Free Government Debt Relief Programs: What’s Real vs What’s a Scam in 2026

Every year, millions of financially stressed households search for the same phrase: free government debt relief programs.

The wording reveals more than curiosity — it reveals urgency.

People are not browsing casually. They are looking for a way out. Credit card balances have doubled, interest rates remain stubbornly high, medical bills pile up unexpectedly, and personal loans stretch budgets to their limits. For many families, minimum payments barely touch the principal. Debt becomes a treadmill that never slows down.

In that situation, the promise of “government debt forgiveness” sounds like salvation.

But here’s the uncomfortable reality most advertisements won’t say clearly: while real government debt relief does exist, broad, universal debt cancellation programs for everyone simply do not. The gap between expectation and reality has created fertile ground for scams that impersonate official help while charging desperate borrowers thousands of dollars in upfront fees.

In 2026, understanding the difference between legitimate assistance and deceptive marketing is no longer optional. It is a financial protection skill.

The goal isn’t just to find relief. It’s to avoid making your debt problem worse.

Why Searches for Government Debt Help Are Surging

Economic pressure has reshaped household finances over the past few years. Inflation has increased everyday expenses. Interest rates have pushed borrowing costs higher. At the same time, wage growth has not kept pace with living costs in many sectors.

This mismatch leaves people leaning heavily on credit.

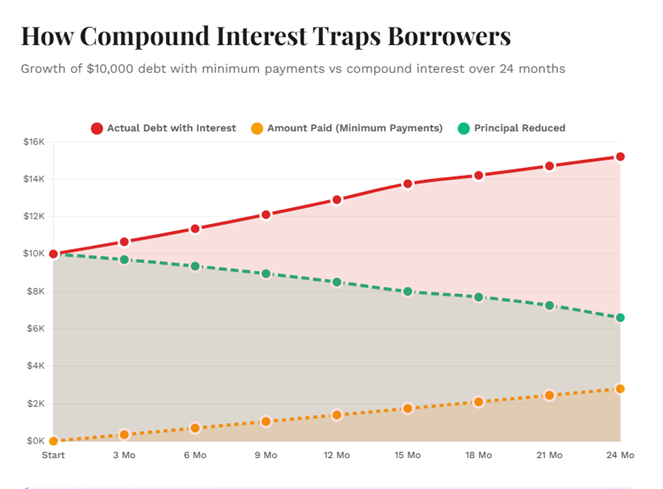

Once balances grow, compound interest accelerates the damage. A $10,000 credit card balance at high interest can quietly become $14,000 or $15,000 even with regular payments. That math alone drives people toward Google at midnight searching for “free government debt relief programs.”

The problem is psychological as much as financial. When someone feels trapped, they look for a fast solution. Scammers understand this behavior better than anyone. They design offers that sound official, urgent, and exclusive.

That’s where confusion begins.

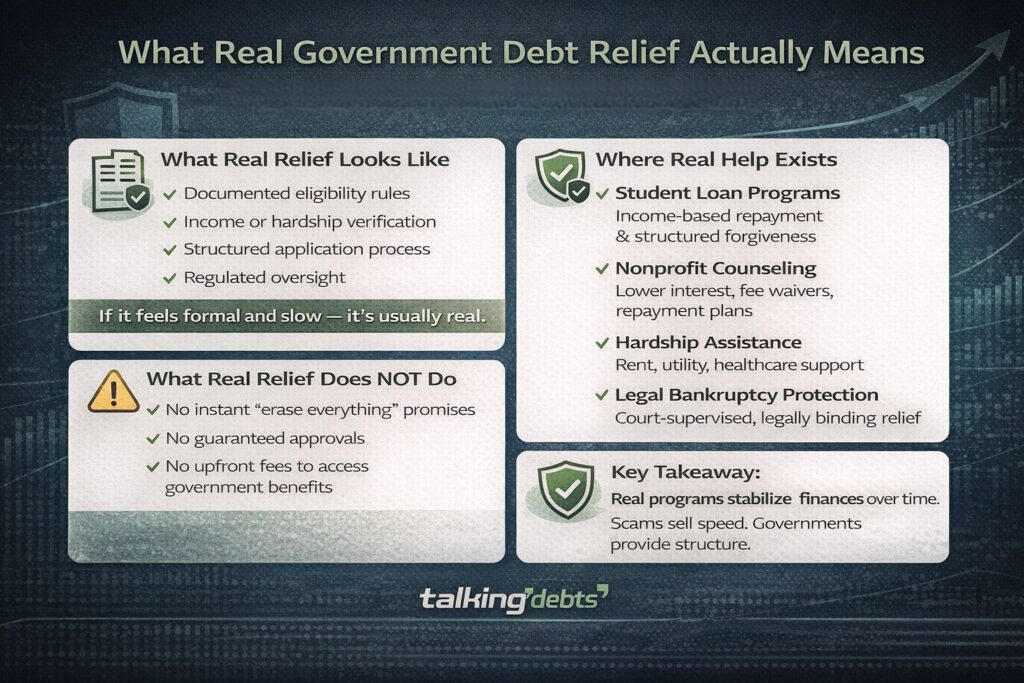

What Real Government Debt Relief Actually Means

Authentic government assistance rarely looks dramatic or instant. It doesn’t promise to “erase everything today.” It doesn’t advertise guaranteed approval. And it never asks for large upfront payments to access benefits.

Instead, legitimate relief follows formal procedures:

- documented eligibility rules

- verification of income or hardship

- structured application processes

- regulated oversight

If it feels slow and bureaucratic, that’s often a sign it’s genuine.

Government programs are built around accountability, not marketing hype. They aim to stabilize finances over time rather than provide magical fixes.

Understanding this difference is critical because it immediately filters out 80% of the fake offers you’ll see online.

Where Real Government Debt Relief Exists

Although there is no universal “wipe-out-your-debt” scheme, several forms of genuine help are available when you know where to look.

Student loan forgiveness and income-based repayment

Federal education loans are one of the few areas where the government directly offers structured forgiveness. Borrowers can qualify for income-driven repayment plans that lower monthly installments based on earnings. In certain professions or after long-term consistent payments, remaining balances may be forgiven.

These programs are real, enforceable, and written into federal policy.

However, enrollment is always free. Any company charging fees to “unlock” these benefits is simply selling paperwork you could complete yourself.

Certified nonprofit debt counseling

Many governments regulate or accredit nonprofit credit counseling agencies. These organizations don’t eliminate debt but help negotiate more manageable repayment structures with creditors.

They may:

- reduce interest rates

- waive penalties or late fees

- consolidate multiple debts into one payment

- create structured repayment schedules

While this approach lacks the appeal of “forgiveness,” it often delivers more sustainable long-term results without harming credit.

Hardship and living-cost assistance

Another overlooked form of relief is indirect support. Rental assistance, utility subsidies, healthcare programs, or temporary income benefits reduce essential expenses. That freed-up cash can then be redirected toward paying down debt faster.

This method may not feel like “debt relief,” but in practice it often works better than risky settlement schemes.

Legal bankruptcy protection

Bankruptcy remains one of the most powerful and misunderstood tools available. It is not a scam or loophole; it is a legal, court-supervised process designed specifically to help individuals who genuinely cannot repay their debts.

Although it carries consequences, it provides something scams never can: legally binding protection from creditors and a clear path forward.

How Debt Relief Scams Trick Borrowers

Fraudulent companies rely on emotional triggers. They know that stressed borrowers are more likely to act quickly without verification.

Most scams follow the same playbook. They use official-sounding language, display fake seals or flags, and claim to be affiliated with government departments. Then they push for immediate action.

Watch for these warning signs:

- promises of guaranteed or instant forgiveness

- requests for upfront enrollment or “processing” fees

- pressure to act today or lose eligibility

- instructions to stop communicating with your creditors

- vague explanations of how the program actually works

Real government debt relief never behaves this way. It doesn’t rush you or threaten you.

If someone sounds more like a salesperson than a public service representative, that’s your cue to step back.

The Hidden Cost of Falling for Fake Programs

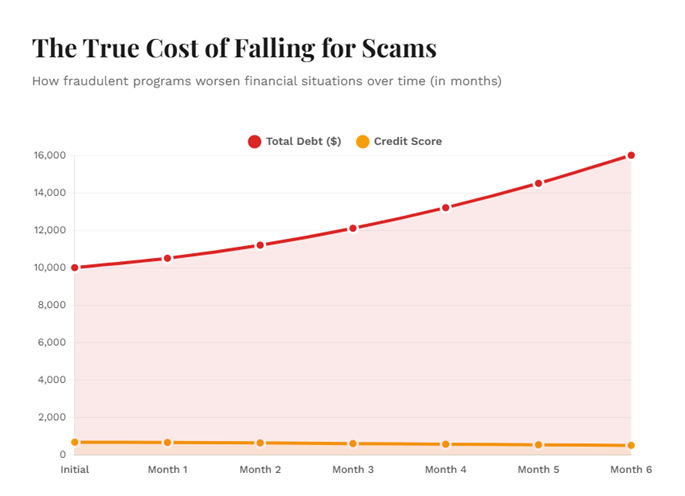

The damage from scams goes far beyond losing a fee.

Many fraudulent firms advise clients to stop paying creditors while they “negotiate.” During this period, late fees accumulate, interest compounds, and accounts may go to collections. Credit scores drop sharply. Lawsuits become possible.

By the time victims realize nothing is being negotiated, their financial position is worse than before.

Ironically, the search for relief creates deeper debt.

That’s why caution matters so much.

How to Verify a Program Before Trusting It

A few simple checks can prevent expensive mistakes.

Start by confirming whether the program is listed on official government websites or recognized consumer protection portals. Genuine initiatives are transparent and publicly documented.

You should also expect written disclosures, clear timelines, and realistic outcomes. No legitimate agency will guarantee results before reviewing your situation.

When in doubt, slow down. Scams depend on urgency. Real help allows time for review.

Building a Smarter Debt Strategy in 2026

The safest path forward usually combines multiple steps rather than chasing one dramatic solution. Budget adjustments, regulated counseling, structured repayment plans, and targeted government assistance together create gradual but reliable progress.

It may not feel exciting, but stability rarely is.

Debt reduction is more like rehabilitation than rescue. It requires planning, consistency, and verified support systems. Once borrowers accept this reality, they become far less vulnerable to unrealistic promises.

And that shift in mindset alone can prevent costly mistakes.

The Reality Borrowers Need to Remember

Searching for free government debt relief programs isn’t wrong. Real support does exist. But the form it takes is very different from what advertisements suggest.

True relief is structured, regulated, and specific. It focuses on affordability and sustainability rather than dramatic cancellation.

Scams sell dreams. Governments offer processes.

One is fast, flashy, and risky. The other is slower, controlled, and safe.

When your financial future is on the line, slow and safe always wins.

Understanding that difference is what separates people who rebuild their finances from those who lose even more chasing false hope.

FAQ (Frequently Asked Questions)

-

Are there real free government debt relief programs in 2026?

Yes, legitimate programs include income-driven repayment plans for federal student loans, nonprofit credit counseling agencies, and bankruptcy protection. There are no programs that eliminate private credit card debt for free — any service claiming this is likely a scam.

-

How do I know if a debt relief program is a scam?

Red flags include upfront fees before any service is provided, guarantees to settle all debt for pennies on the dollar, instructions to stop communicating with creditors, and no CFPB or BBB registration.

-

What is the difference between debt relief and debt consolidation?

Debt consolidation combines multiple debts into one lower-interest loan — you still repay the full amount. Debt relief (or settlement) negotiates to reduce the total amount owed, usually at a cost to your credit score.

-

Who qualifies for government-approved debt relief in 2026?

Eligibility depends on debt type. Federal student loan borrowers may qualify under the IDR or PSLF programs. Consumers overwhelmed by medical or credit card debt may qualify for Chapter 7 or Chapter 13 bankruptcy protection based on income.

-

Is the 2026 emergency debt relief program real?

There is no single “2026 emergency debt relief program.” This phrase is often used in scam advertisements. Legitimate assistance exists through the CFPB, HUD-approved housing counselors, and federally approved credit counseling agencies.