Why Debt Collectors Call From Different Numbers — And How to Make It Stop

If you’ve been receiving repeated calls from unknown numbers about a debt, you’re not alone. Many consumers search for answers when they notice debt collectors calling from different numbers instead of a single consistent contact. The experience can feel confusing, stressful, and sometimes even intimidating.

Understanding why this happens — and what you can legally do about it — is the first step toward regaining control of your phone and your peace of mind. This guide explains the real reasons behind multiple-number collection calls and provides practical, legally sound steps to make the calls stop.

Why Debt Collectors Call From Different Numbers

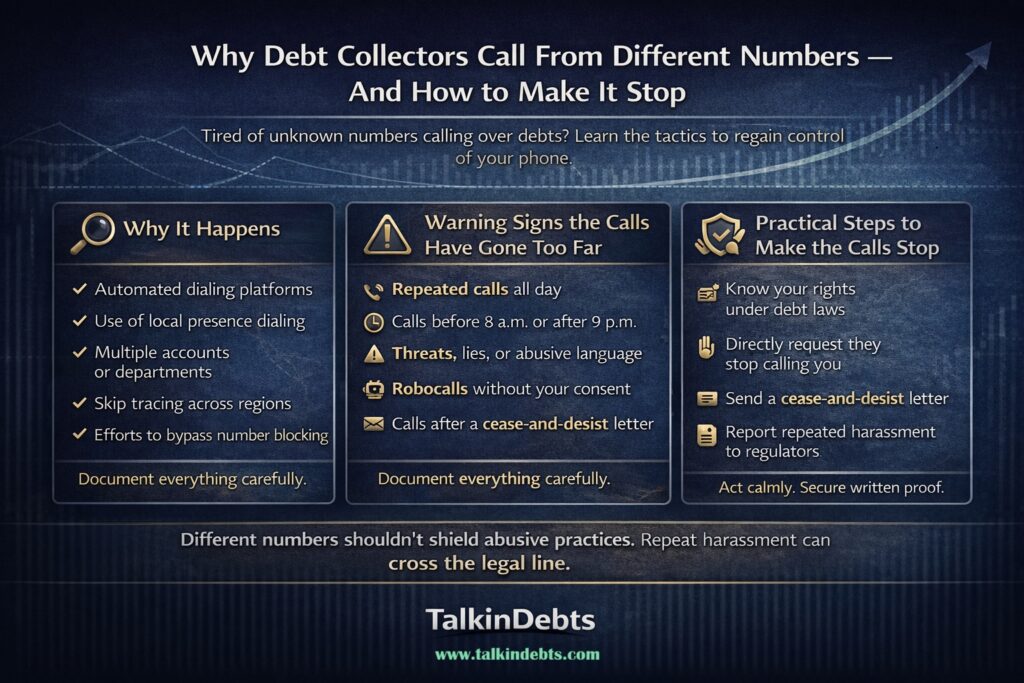

When consumers notice debt collectors calling from different numbers, it usually isn’t random. There are several common operational and technical reasons behind this practice.

1. Use of Automated Dialing Systems

Most modern collection agencies use automated dialing platforms. These systems:

- Rotate outgoing phone numbers

- Route calls through different lines

- Display local area codes to increase answer rates

From the agency’s perspective, this improves contact efficiency. From the consumer’s side, it can feel like harassment — especially when the calls are frequent.

2. Local Presence Dialing

A very common reason for debt collectors calling from different numbers is something called local presence dialing. This technology:

- Matches the caller ID to your area code

- Makes the call appear local

- Increases the likelihood you’ll answer

While widely used in the industry, it can create the impression that multiple collectors are calling you when it may actually be the same company.

3. Multiple Accounts or Departments

Sometimes the reason is administrative rather than technical. You may see different numbers because:

- Your account was transferred internally

- Multiple debts are being pursued

- Different departments attempted contact

- The debt was sold to a new agency

In these cases, the calls may legitimately originate from different numbers — but they must still follow the law.

4. Third-Party Skip Tracing Efforts

Collection agencies often use skip tracing teams to locate updated contact details. These teams may:

- Test multiple lines

- Call from different outbound systems

- Use various regional numbers

This can increase call frequency and number variation, particularly in early-stage recovery efforts.

5. Attempting to Improve Contact Rates

Let’s be direct: sometimes agencies rotate numbers because consumers tend to block known collection numbers. When one number gets blocked, the system may simply try another.

However — and this is critical — there are legal limits to how far collectors can go.

Is It Legal for Debt Collectors to Call From Different Numbers?

The short answer: using different numbers is not automatically illegal. But the way collectors use them can cross legal boundaries.

Collectors must still comply with consumer protection laws, such as:

- The Fair Debt Collection Practices Act (FDCPA) in the U.S.

- The Telephone Consumer Protection Act (TCPA)

- Local consumer protection regulations in other countries

If the pattern of calls becomes excessive, deceptive, or abusive, it may violate the law — regardless of how many numbers are used.

Warning Signs the Calls May Be Crossing the Line

Not every situation involving debt collectors calling from different numbers is improper. However, certain patterns should raise red flags.

Watch for these warning signs:

- 📞 Repeated calls throughout the day

- 📞 Calls before 8 a.m. or after 9 p.m. (in many jurisdictions)

- 📞 Robocalls without consent

- 📞 Calls that continue after you request written communication

- 📞 Threatening or abusive language

- 📞 Failure to identify the company clearly

- 📞 Calls after you’ve sent a cease-and-desist letter

If you notice several of these behaviors together, you may have grounds to take action.

Why Blocking the Numbers Often Doesn’t Work

Many people’s first instinct is to block each incoming number. Unfortunately, when debt collectors are calling from different numbers, simple blocking usually fails.

Here’s why:

- Dialing systems generate new outbound numbers

- Agencies may have dozens of lines

- Local presence tools can create many variations

- New agencies may acquire the debt later

Blocking can reduce noise temporarily, but it rarely solves the root problem.

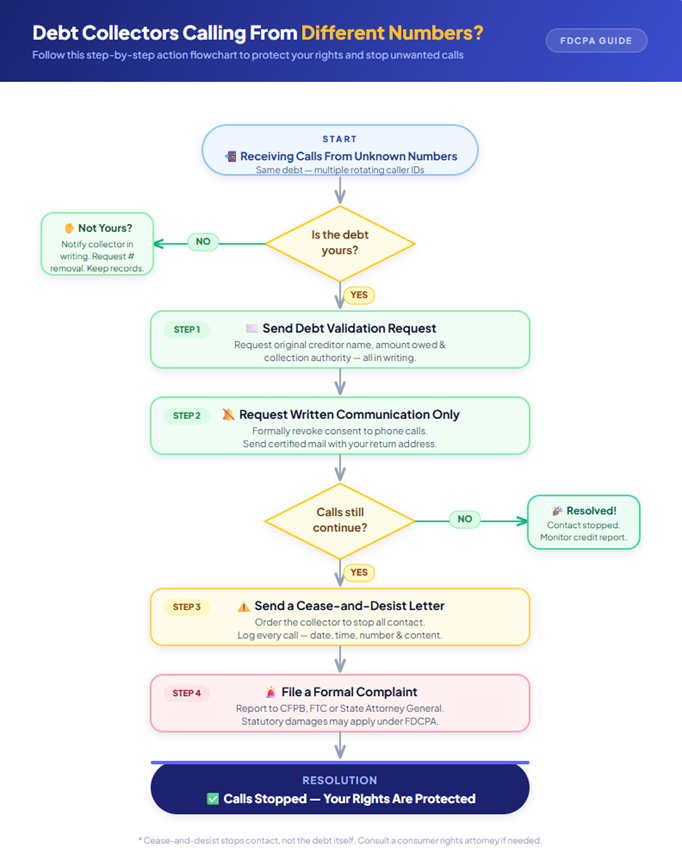

How to Make Debt Collector Calls Stop (Step-by-Step)

The good news: you do have options. If you’re dealing with persistent calls from rotating numbers, follow this structured approach.

Step 1: Request Debt Validation

Before anything else, confirm the debt is legitimate.

Send a written debt validation request asking for:

- The original creditor

- The amount owed

- Prove the agency has the authority to collect

- Account documentation

Many consumers discover errors at this stage. If the collector cannot validate the debt properly, they must stop collection efforts.

Step 2: Send a Written Communication Preference Notice

If phone calls are overwhelming, you can formally request limited communication.

Your letter should state:

- You prefer communication in writing

- You revoke consent for automated calls (if applicable)

- Your correct mailing address

Once received, reputable agencies typically reduce phone activity significantly.

Step 3: Issue a Cease-and-Desist Letter (When Appropriate)

If the calls remain excessive, you can escalate.

A cease-and-desist letter instructs the collector to stop contacting you. After receiving it, they may only contact you to:

- Confirm no further contact will occur

- Notify you of specific legal action

Important: This does not erase the debt — it only stops communication.

Step 4: Document Every Call

When dealing with debt collectors calling from different numbers, documentation is powerful.

Keep a log including:

- Date and time

- Phone number used

- Company name given

- Summary of conversation

- Whether it was a robocall

This record becomes critical if you later file a complaint.

Step 5: Register on Do Not Call Lists (Where Applicable)

While debt collectors have certain exemptions, registering your number can still help in some cases — especially with borderline or third-party telemarketing-style calls.

It also strengthens your position if unwanted robocalls continue.

Step 6: File a Formal Complaint if Harassment Continues

If the behavior appears excessive or deceptive, you can escalate to regulators.

Common complaint channels include:

- Consumer protection authorities

- Telecommunications regulators

- Financial ombudsman services

- Attorney General’s offices (in some countries)

Provide your call log and any written correspondence.

Special Case: When the Debt Isn’t Yours

A surprisingly common situation involves debt collectors calling from different numbers about a debt that doesn’t belong to you.

If this happens:

- Clearly state that you are not the debtor

- Request the removal of your number

- Follow up in writing

- Keep records of continued calls

Collectors are required to update their records when properly notified.

How Collection Agencies View Multiple Number Dialing

From the industry side — and this is important context — rotating numbers is often seen as an efficiency tool rather than harassment.

Agencies typically aim to:

- Improve right-party contact rates

- Reduce abandoned calls

- Manage large account volumes

- Comply with dialing regulations

However, consumer experience matters. When call frequency becomes excessive or misleading, regulators may intervene.

Preventive Steps to Reduce Future Collection Calls

Beyond stopping current calls, you can take steps to reduce future issues.

Keep Your Contact Information Updated

Outdated records often trigger aggressive skip tracing. Updating addresses with creditors can reduce unnecessary outreach.

Respond Early to Legitimate Debts

Accounts that go silent longer often move to more intensive dialing campaigns. Early engagement can sometimes prevent escalation.

Monitor Your Credit Reports

Regular monitoring helps you spot:

- Newly placed collections

- Incorrect accounts

- Identity mix-ups

Early detection gives you more control.

When to Seek Professional Help

Consider speaking with a consumer rights professional if:

- Calls exceed a reasonable frequency

- You suspect robocall violations

- The collector uses threats or deception

- Your cease-and-desist is ignored

- You are being contacted about someone else’s debt repeatedly

In some jurisdictions, consumers may be entitled to statutory damages for unlawful collection practices.

Take Back Control of Your Phone

Dealing with debt collectors calling from different numbers can feel overwhelming, but you are not powerless. In many cases, the behavior stems from automated systems and contact strategies — not necessarily wrongdoing.

That said, collectors must follow strict legal boundaries. When calls become excessive, misleading, or continue after formal requests, you have clear rights and escalation paths.

Start by validating the debt, setting firm communication preferences, documenting everything, and escalating when necessary. With the right steps, most consumers can significantly reduce — or completely stop — unwanted collection calls.

If the situation persists despite your efforts, it may be time to seek professional guidance and formally assert your consumer rights.