How to Understand Your Credit Report: A Beginner’s Guide

Your credit report plays a crucial role in your financial life. Whether you are applying for a loan, credit card, mortgage, or even renting a home, lenders and financial institutions often review your credit report before making decisions. Yet many people do not fully understand what a credit report contains or how it affects their financial opportunities.

Understanding your credit report is one of the most important steps toward building strong financial health. It helps you identify potential errors, detect fraud early, and improve your creditworthiness. For beginners, a credit report may appear complicated at first, filled with numbers, account histories, and financial terms. However, once you understand the structure and purpose of each section, it becomes much easier to interpret.

Learning how to read and monitor your credit report allows you to take control of your financial future. With the right knowledge, you can make better borrowing decisions, maintain a positive credit profile, and avoid unnecessary financial setbacks.

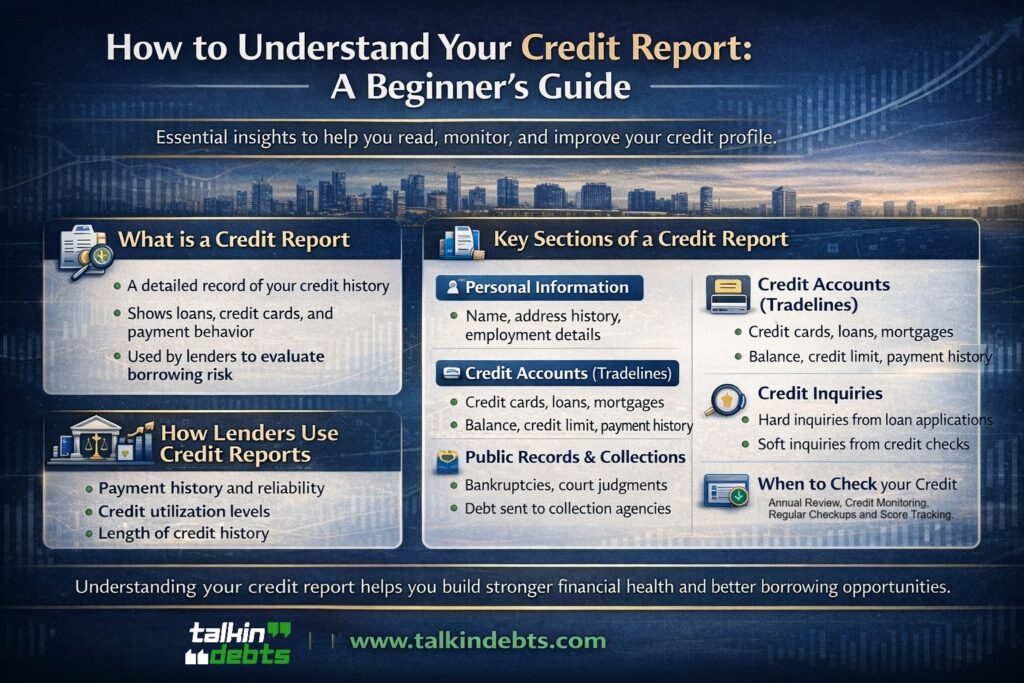

What a Credit Report Is

A credit report is a detailed record of your credit history. It is compiled by credit bureaus that collect financial information from banks, lenders, credit card companies, and other financial institutions. The report provides a snapshot of how you manage borrowed money.

Whenever you take out a loan, open a credit card, or make payments toward debt, these activities may be recorded in your credit report. Over time, this information builds a profile that reflects your financial behavior.

Your credit report does not just show how much you owe. It also tracks how consistently you repay your debts, how long you have maintained credit accounts, and how often you apply for new credit. This information helps lenders assess your reliability as a borrower.

Credit reports typically include personal information such as your name, address history, and employment details. They also list credit accounts, payment histories, outstanding balances, and records of any late or missed payments.

While many people confuse credit reports with credit scores, the two are different. A credit report contains the raw financial data, while a credit score is a numerical summary calculated from that data. Lenders use both to evaluate risk before approving credit applications.

Understanding what your credit report represents is the first step in managing your financial reputation.

Key Sections of a Credit Report

Although the format may vary slightly between credit bureaus, most credit reports contain several standard sections. Each section provides specific insights into your financial behavior.

Personal Information

The personal information section identifies the individual whose credit report it is. It typically includes your full name, date of birth, current and previous addresses, phone numbers, and sometimes employment details.

This section does not affect your credit score, but it ensures that the credit data is associated with the correct individual. If incorrect information appears here, it could indicate a clerical error or potential identity theft.

Credit Accounts

The credit accounts section, often called the “tradelines” section, lists all credit accounts associated with your name. This includes credit cards, personal loans, auto loans, mortgages, and other lines of credit.

For each account, the report may show:

- The name of the lender

- The type of credit account

- The date the account was opened

- The credit limit or loan amount

- The current balance

- The payment history

Payment history is particularly important because it reveals whether payments were made on time. Late or missed payments may negatively affect your creditworthiness.

Credit Inquiries

Credit inquiries occur when a lender checks your credit report after you apply for credit. These inquiries are usually categorized as either hard inquiries or soft inquiries.

Hard inquiries happen when you apply for credit cards, loans, or mortgages. Too many hard inquiries within a short period may signal financial risk to lenders.

Soft inquiries occur when you check your own credit report or when companies conduct background checks for pre-approved offers. Soft inquiries do not affect your credit score.

Public Records

In some cases, credit reports may include public financial records. These may involve bankruptcies, tax liens, or court judgments related to unpaid debts.

Such records can significantly influence how lenders perceive your financial stability. Although not everyone has public records listed, reviewing this section ensures that the information is accurate and up to date.

Collections Accounts

If a debt remains unpaid for a long time, it may be transferred to a collection agency. Collection accounts appear in this section of your credit report.

These entries indicate that a lender was unable to recover the debt through normal payment arrangements. Collections accounts may negatively impact your credit profile and remain visible for several years, depending on the regulations in your country.

Understanding each section of your credit report helps you quickly identify the factors affecting your financial standing.

How Lenders Use Credit Reports

Lenders rely heavily on credit reports when evaluating whether to approve a credit application. The report helps them assess the risk of lending money to a borrower.

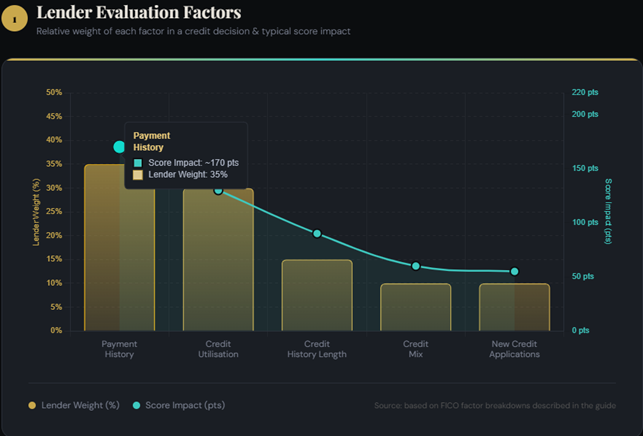

One of the main factors lenders examine is payment history. Consistently paying bills on time demonstrates financial responsibility and increases trust between borrowers and lenders.

Credit utilization is another important factor. This refers to how much of your available credit you are currently using. High utilization levels may signal financial strain, while moderate usage often indicates responsible credit management.

The length of your credit history also matters. Longer credit histories provide lenders with more data about your financial habits. A well-managed account history over many years can strengthen your credit profile.

Lenders also review the types of credit accounts you maintain. A balanced mix of credit cards, installment loans, and other accounts may suggest that you can manage different forms of credit effectively.

Another key factor is recent credit activity. Multiple new credit applications in a short period may raise concerns about financial stress. Lenders may view this as a sign that a borrower is relying heavily on credit.

By analyzing these elements, lenders determine whether to approve credit, set interest rates, or establish borrowing limits. In many cases, a stronger credit report can lead to better loan terms and lower interest rates.

Understanding how lenders interpret your credit report can help you maintain habits that support a healthy financial profile.

Where to Check Your Credit Report

Checking your credit report regularly is essential for maintaining financial awareness. Many people only look at their credit reports when applying for loans, but reviewing them periodically can help identify problems early.

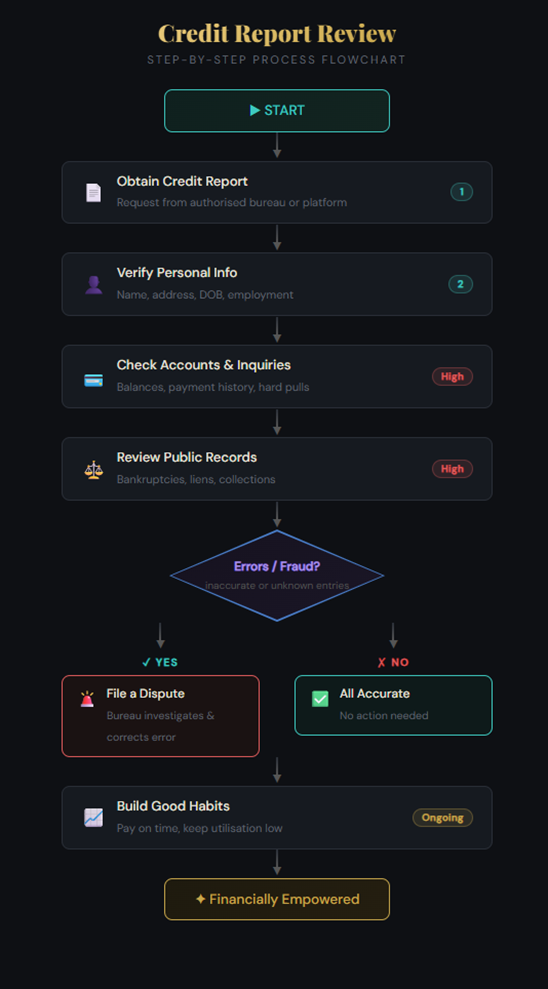

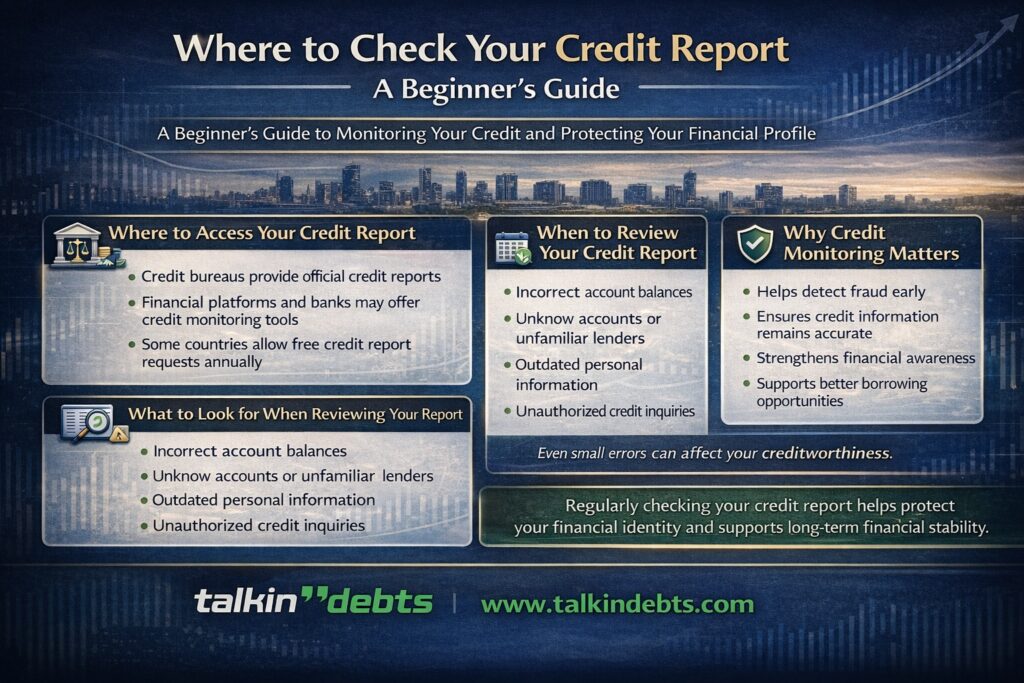

Credit reports are typically available through credit bureaus and authorized financial platforms. Depending on your country, you may be able to request free copies of your credit report at certain intervals.

Many financial institutions and digital financial services now provide credit monitoring tools that allow individuals to track changes in their credit profiles. These services may notify users about new accounts, credit inquiries, or unusual activity.

When reviewing your credit report, it is important to look for inaccuracies such as incorrect account balances, unfamiliar accounts, or outdated personal information. Even small errors may affect how lenders interpret your creditworthiness.

If you notice incorrect information, you can usually dispute the error with the credit bureau that issued the report. The bureau will then investigate the claim and update the report if necessary.

Regularly checking your credit report helps ensure that your financial records remain accurate and secure.

When to Review Your Credit Report

Monitoring your credit report should become part of your regular financial routine. There are several situations when reviewing your credit report is particularly important.

One key moment is before applying for a major loan or credit card. Checking your credit report beforehand allows you to identify potential issues that could affect your application.

Another important time to review your credit report is after paying off significant debts. Confirming that closed accounts are correctly recorded ensures that your credit history reflects your progress.

You should also check your credit report if you suspect identity theft or fraudulent activity. Unexpected accounts or unfamiliar inquiries may indicate that someone has used your personal information without authorization.

Major life events can also make credit report monitoring more important. Buying a home, starting a business, or planning large financial commitments often requires a strong credit profile.

Even without specific financial events, reviewing your credit report at least once or twice a year can help maintain financial awareness. Regular monitoring allows you to track improvements, spot errors quickly, and make informed financial decisions.

Building Confidence Through Credit Awareness

Understanding your credit report is an essential skill for anyone managing personal finances. While the document may appear complex at first, learning how to interpret its sections can provide valuable insights into your financial behavior.

Your credit report tells a story about how you manage money and repay debts. By reviewing it regularly, you gain a clearer understanding of your financial strengths and areas that may require improvement.

Responsible credit habits, such as making payments on time and maintaining balanced credit usage, can gradually strengthen your credit profile. Over time, these habits may improve your borrowing opportunities and financial flexibility.

Credit awareness is not just about avoiding financial problems. It is about building long-term financial stability and ensuring that your credit history accurately represents your financial responsibility.

By understanding your credit report and monitoring it consistently, you can take meaningful steps toward a healthier financial future.

Learn more about our Credit Counselling Guidance and Free Initial Assessment Available