What Your Credit Score Really Means: How to Interpret Scores and Key Factors

Your credit score is one of the most influential numbers in your financial life. It quietly shapes major decisions—whether you can borrow money, how much you can borrow, and how much that borrowing will cost you over time. Yet, despite its importance, many people only have a surface-level understanding of what their credit score really means.

In reality, your credit score is not just a number—it is a reflection of your financial behavior, discipline, and reliability. It acts as a trust signal to lenders, service providers, and sometimes even employers. Understanding how it works can help you take control of your financial future, reduce borrowing costs, and unlock better opportunities.

What a Credit Score Measures

A credit score is a numerical representation of your creditworthiness. It is designed to predict how likely you are to repay borrowed money based on your past financial behavior.

Credit scores are calculated using data from your credit report, which includes your borrowing and repayment history. The score is typically generated using models such as FICO or VantageScore.

These scoring models analyze multiple aspects of your financial activity to create a comprehensive picture of how you manage credit.

Key Factors That Influence Your Credit Score

Payment History

This is the most important component of your credit score. It reflects whether you pay your financial obligations on time. Consistent, on-time payments build trust with lenders, while missed or late payments can significantly reduce your score. Even one delayed payment can remain on your report for years.

Credit Utilization Ratio

This measures how much of your available credit you are currently using. For example, if you have access to a total credit limit and you are using a large portion of it, lenders may see this as a sign of financial pressure. Keeping your utilization low demonstrates responsible credit management.

Length of Credit History

The duration of your credit activity matters. A longer credit history provides more data and helps lenders better understand your financial behavior. Older accounts contribute positively, especially if they show a consistent record of responsible usage.

Credit Mix

Having a mix of different types of credit—such as revolving credit (credit cards) and installment loans (personal loans or mortgages)—can improve your score. It shows that you can manage multiple types of financial obligations effectively.

New Credit Activity

Opening several new credit accounts in a short period can lower your score. Each application results in a hard inquiry, which may signal that you are actively seeking credit and could be at higher risk.

It is important to understand that your credit score does not measure your income or wealth. Instead, it focuses on how consistently and responsibly you manage the credit available to you.

Credit Score Ranges Explained

Credit scores generally range from 300 to 850, depending on the scoring model used. These ranges help lenders categorize borrowers based on risk levels.

Credit Score Categories and What They Mean

800 – 850: Excellent

This range reflects exceptional credit management. Individuals in this category are considered very low risk and are likely to receive the best interest rates, highest credit limits, and most favorable terms.

740 – 799: Very Good

A very strong score that indicates reliability and consistency. Borrowers in this range typically qualify for competitive loan offers and flexible terms.

670 – 739: Good

This is a solid and acceptable range for most lenders. While not the highest tier, it still allows access to a wide range of credit products.

580 – 669: Fair

This range suggests moderate risk. Lenders may still approve applications, but often with higher interest rates and stricter conditions.

300 – 579: Poor

A low score indicates significant credit challenges, such as missed payments or defaults. Access to credit is limited, and borrowing becomes more expensive.

Understanding your credit score range gives you a clear picture of where you stand and what improvements may be needed. It also helps set realistic expectations when applying for credit.

Why Lenders Check Credit Scores

Lenders rely on credit scores to make quick, consistent, and informed decisions about whether to extend credit. Instead of reviewing every detail manually, they use your score as a summary of your financial reliability.

What Lenders Assess Using Your Credit Score

- Your likelihood of repaying a loan

- The level of risk involved in lending to you

- The appropriate interest rate for your profile

- The amount of credit you should receive

The Role of Risk-Based Pricing

Most lenders use a system called risk-based pricing, where your credit score directly influences the terms of your loan:

- Higher credit score = Lower risk = Lower interest rates

- Lower credit score = Higher risk = Higher interest rates

This approach allows lenders to balance risk while offering competitive terms to reliable borrowers.

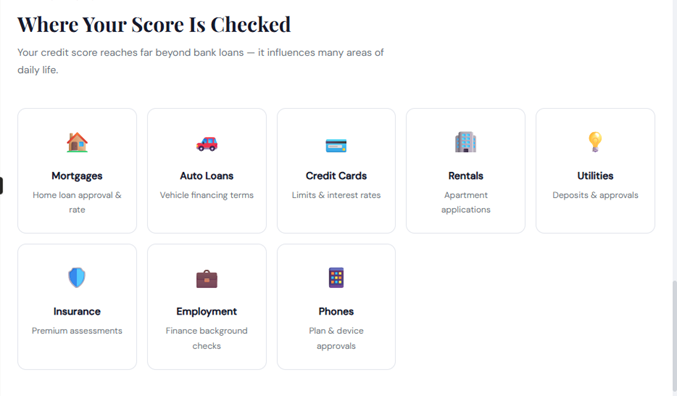

Where Credit Scores Are Used

Your credit score plays a role in many areas beyond traditional loans, including:

- Rental housing applications

- Utility and service approvals

- Insurance risk assessments

- Employment background checks in certain industries

In modern financial systems, your credit score functions as a universal indicator of trust. It helps organizations evaluate how dependable you are in meeting financial commitments.

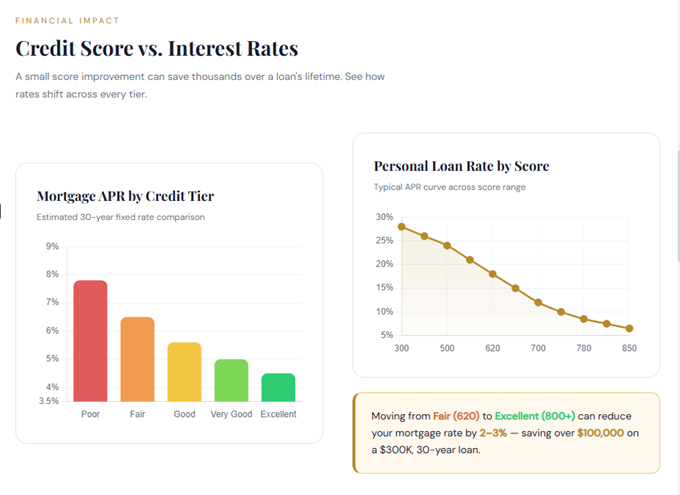

How Scores Impact Loans and Interest Rates

Your credit score has a direct and long-term impact on your financial costs. It determines not only whether you are approved for credit but also how much you will pay over time.

Interest Rates and Credit Scores

Lenders use your credit score to decide the interest rate on your loan. A higher score indicates lower risk, which leads to lower interest rates. A lower score increases perceived risk, resulting in higher rates.

Even a small difference in your credit score can significantly affect the total amount you repay over the life of a loan.

Key Ways Your Credit Score Affects Borrowing

Loan Approval

Applicants with strong credit scores are more likely to be approved quickly and with fewer conditions.

Total Cost of Borrowing

Lower interest rates reduce the overall cost of a loan, saving money over time.

Credit Limits

Higher scores often lead to higher credit limits, giving you greater financial flexibility.

Loan Terms and Flexibility

A strong score can help you secure better repayment terms, including longer tenures or lower monthly payments.

Speed of Approval

High-score applicants often benefit from faster processing due to lower perceived risk.

Long-Term Financial Impact

A low credit score can have lasting consequences. Higher interest rates, limited options, and stricter requirements can make borrowing more expensive and less accessible. Over time, this can create a cycle where financial progress becomes more difficult.

On the other hand, maintaining a high credit score allows you to borrow efficiently, reduce costs, and take advantage of better financial opportunities.

Tips to Maintain a Healthy Credit Score

Building and maintaining a strong credit score requires consistent effort, but the process is straightforward when you follow the right habits.

Make Payments on Time

Timely payment of all financial obligations is essential. Payment history has the greatest impact on your credit score, making this the most important habit to maintain.

Keep Credit Utilization Low

Try to use only a small portion of your available credit. Staying below 30% utilization is widely recommended for maintaining a healthy score.

Limit New Credit Applications

Avoid applying for multiple credit accounts within a short period. Each application can slightly lower your score and signal increased risk.

Maintain Long-Term Credit Accounts

Keeping older accounts open helps extend your credit history and strengthens your profile.

Monitor Your Credit Report Regularly

Reviewing your credit report allows you to detect errors, fraud, or inaccuracies that could negatively impact your score.

Maintain a Balanced Credit Mix

Using different types of credit responsibly demonstrates your ability to handle various financial obligations.

Avoid Maxing Out Credit Cards

Using your full credit limit frequently can signal financial stress and lower your score.

Address Outstanding Debts Quickly

Clearing overdue balances and resolving collection accounts can help improve your score over time.

Final Insights

Your credit score is more than just a number—it is a reflection of your financial habits, discipline, and reliability. It influences your ability to access credit, the cost of borrowing, and your overall financial flexibility.

By understanding what your credit score really means and taking consistent steps to manage it, you can build a strong financial foundation that supports your long-term goals.

A strong credit score opens the door to better opportunities, lower costs, and greater financial confidence. Over time, it becomes one of the most valuable assets you can build—one that supports not just borrowing, but your entire financial journey.

Learn more about our Credit Counselling Guidance