How Credit Utilization Affects Your Credit Score?

Your credit score plays a critical role in your financial life in the United States. Whether you’re applying for a credit card, auto loan, mortgage, or even renting an apartment, your score can determine approval and interest rates. One of the most influential yet often misunderstood factors in your credit score is credit utilization.

Understanding how credit utilization works—and how to control it—can quickly improve your credit profile and unlock better financial opportunities.

What Does Credit Utilization Mean?

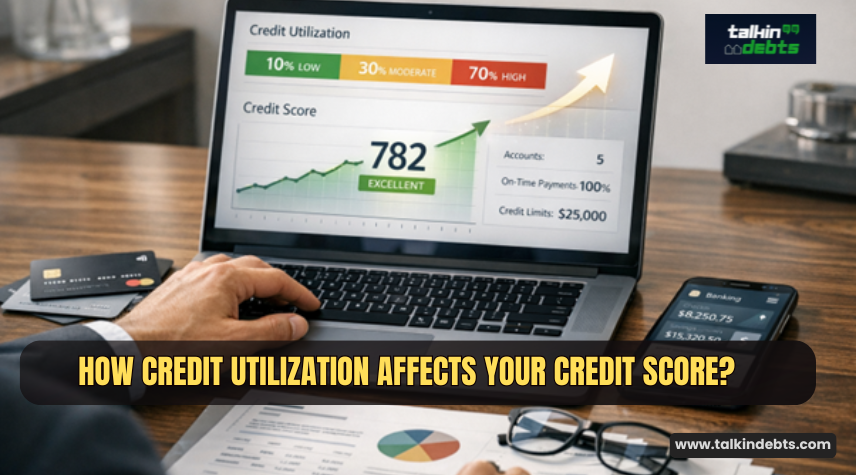

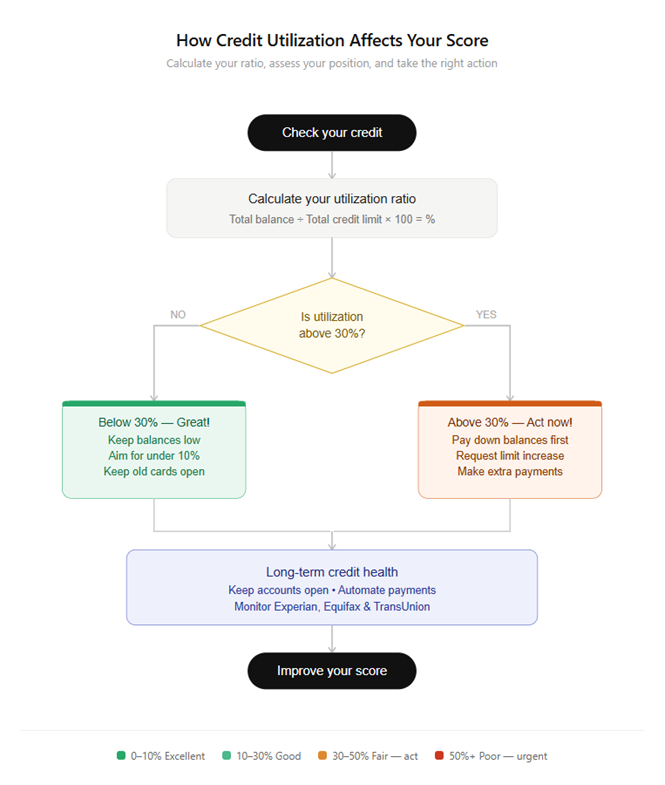

Credit utilization refers to the percentage of your available credit that you are currently using. It is calculated by dividing your total credit card balances by your total credit limits.

For example, if your total credit limit across all cards is $10,000 and your current balance is $3,000, your credit utilization ratio is:

$3,000 ÷ $10,000 = 30%

This percentage is one of the most important components of your credit score. In the U.S., credit scoring models like FICO and Vantage Score consider credit utilization as a major factor because it reflects how responsibly you manage credit.

There are two types of utilization:

- Overall utilization – Total balances across all cards divided by total credit limit

- Per-card utilization – Balance on each individual card divided by its limit

Both matter. Even if your overall utilization is low, having one card maxed out can negatively affect your score.

Ideal Credit Utilization Ratio

In general, the lower your credit utilization ratio, the better it is for your credit score.

Here’s how different utilization levels are typically viewed:

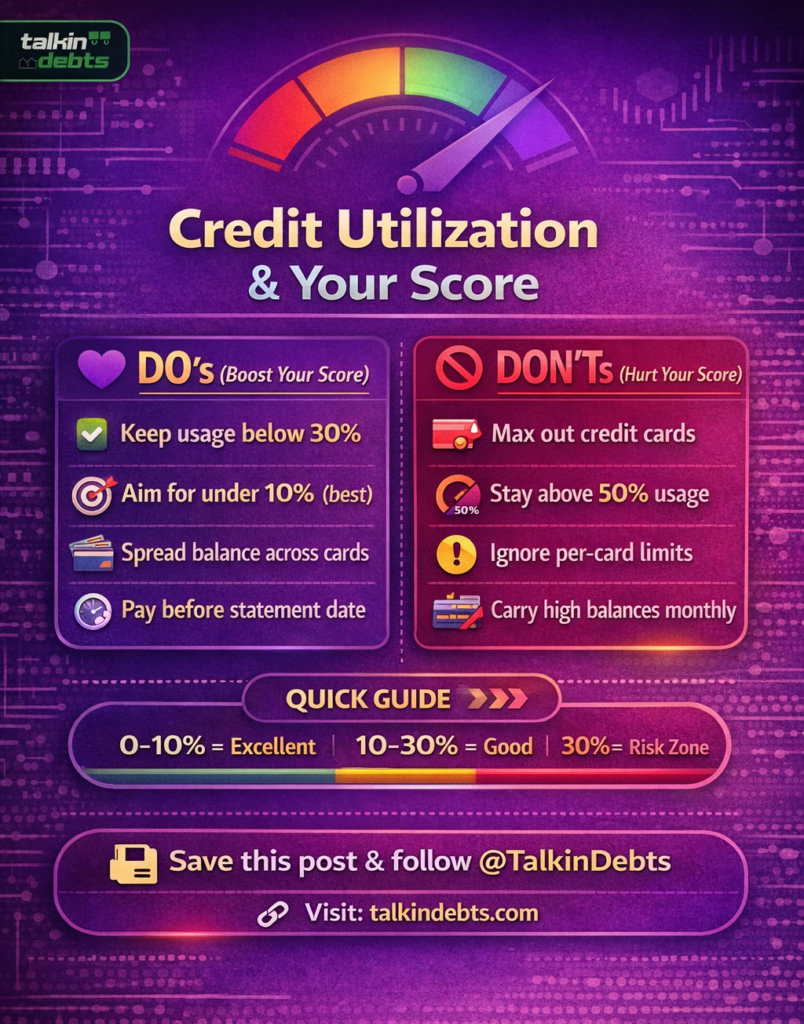

- 0%–10%: Excellent (optimal for top-tier scores)

- 10%–30%: Good (safe range)

- 30%–50%: Fair (may start hurting your score)

- 50%+: Poor (significant negative impact)

Most financial experts recommend keeping your credit utilization below 30%, but for the best results, aiming under 10% is ideal.

For example:

- If your credit limit is $5,000, try to keep your balance below $500 for optimal scoring.

In the U.S. credit system, lenders see high utilization as a sign of financial stress or overdependence on credit, even if you pay your bills on time.

How High Balances Impact Your Credit Score

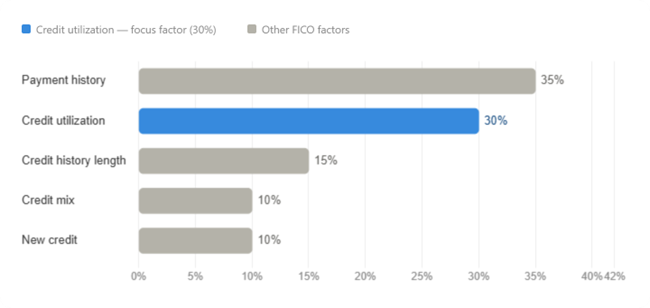

High credit card balances can significantly lower your credit score, even if you never miss a payment. This is because credit utilization makes up about 30% of your FICO score, making it the second most important factor after payment history.

Here’s how high utilization affects your score:

1. Signals Higher Risk to Lenders

When you use a large portion of your available credit, lenders may view you as a higher-risk borrower. It suggests you might be relying heavily on credit to manage expenses.

2. Reduces Available Credit Cushion

A high balance reduces your available credit, leaving little room for emergencies. This lack of flexibility can negatively influence your credit profile.

3. Immediate Score Drops

Unlike some credit factors that take time to impact your score, utilization changes can affect your score almost immediately once reported to credit bureaus.

4. Multiple High Balances Compound the Problem

If several credit cards have high balances, the negative impact is even stronger. Both overall and per-card utilization matter.

5. Temporary but Powerful Effect

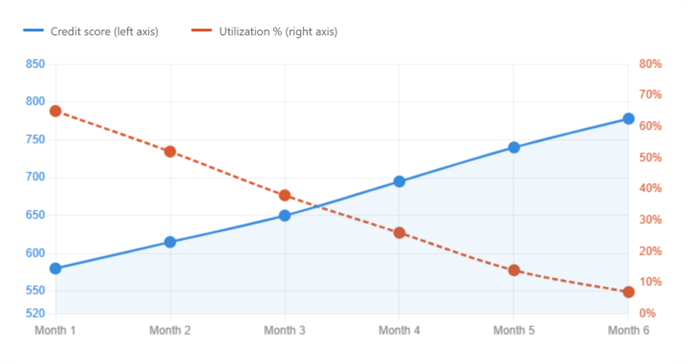

The good news is that utilization has no memory. Once you lower your balances, your score can improve quickly—sometimes within a month.

Ways to Lower Credit Utilization Quickly

If your credit utilization is high, there are several effective ways to bring it down fast and boost your score.

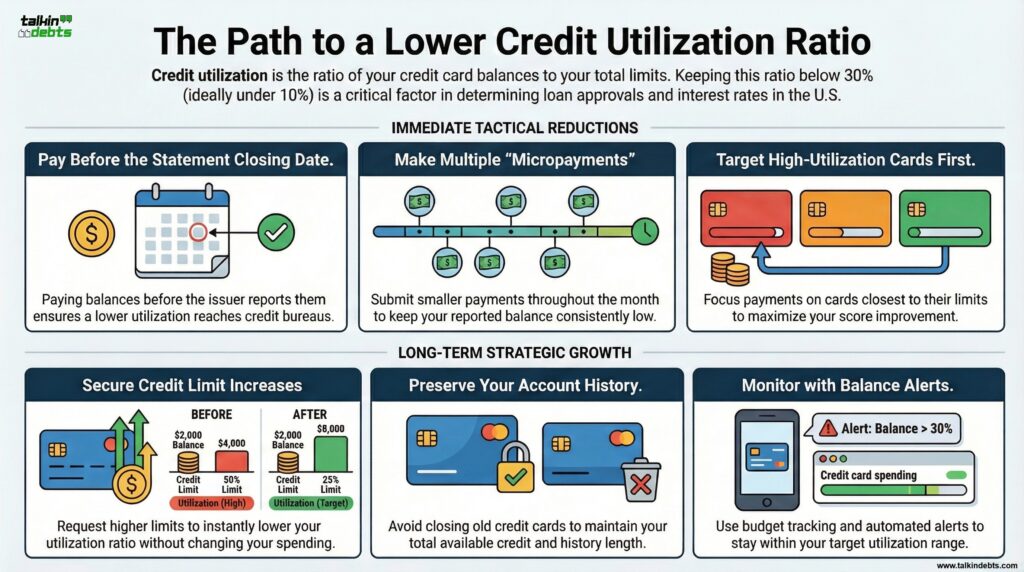

1. Pay Down Balances Before the Statement Date

Credit card issuers typically report balances to credit bureaus at the end of your billing cycle. Paying down your balance before this date ensures a lower utilization gets reported.

2. Make Multiple Payments Each Month

Instead of waiting for your due date, make smaller payments throughout the month. This keeps your reported balance consistently low.

3. Request a Credit Limit Increase

Increasing your credit limit reduces your utilization ratio instantly—without changing your spending.

Example:

- Balance: $2,000

- Limit: $4,000 → 50% utilization

- New Limit: $8,000 → 25% utilization

However, only request increases if you can avoid increasing your spending.

4. Use Multiple Credit Cards Strategically

Spread your expenses across multiple cards to keep individual card utilization low.

5. Pay Off High-Utilization Cards First

Focus on cards that are closest to their limit. Reducing these balances can have a bigger impact on your score.

6. Avoid Closing Old Credit Cards

Closing a card reduces your total available credit, which can increase your utilization ratio overnight.

7. Use Balance Alerts and Budget Tracking

Set alerts to monitor your spending and ensure you stay within your target utilization range.

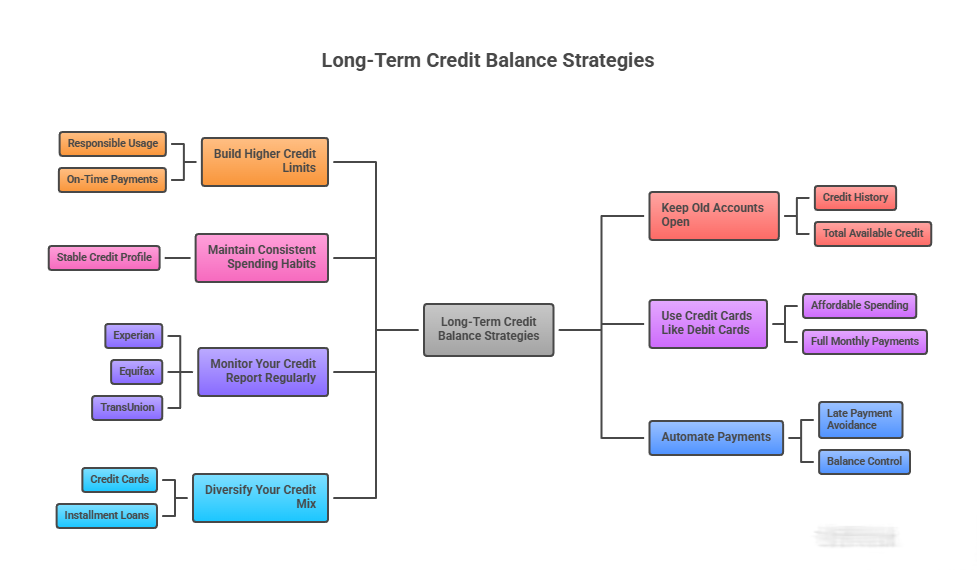

Long-Term Credit Balance Strategies

While quick fixes can improve your credit utilization temporarily, long-term strategies are essential for maintaining a strong credit score in the U.S.

Build Higher Credit Limits Over Time

Responsible usage and on-time payments can lead to automatic credit limit increases. Higher limits make it easier to maintain low utilization.

Keep Old Accounts Open

The length of your credit history also matters. Keeping older accounts open helps maintain both your credit history and total available credit.

Maintain Consistent Spending Habits

Avoid sudden spikes in credit usage. Consistency is key to maintaining a stable credit profile.

Use Credit Cards Like Debit Cards

Only spend what you can afford to pay off in full each month. This prevents balances from accumulating.

Monitor Your Credit Report Regularly

Check your credit reports from the three major U.S. credit bureaus—Experian, Equifax, and TransUnion—to ensure accurate reporting.

Automate Payments

Set up automatic payments to avoid late payments while keeping your balances under control.

Diversify Your Credit Mix

While utilization is important, having a mix of credit types (credit cards, installment loans, etc.) can further strengthen your credit profile.

Why Credit Utilization Matters More Than You Think

Many people focus only on making on-time payments, but credit utilization can quietly damage your score even if you never miss a due date.

In the U.S., lenders use your credit score to determine:

- Loan approvals

- Interest rates

- Credit limits

- Insurance premiums (in some states)

- Rental eligibility

A high utilization ratio can cost you thousands of dollars in higher interest rates over time.

On the other hand, maintaining low utilization signals strong financial discipline and can help you qualify for better financial products.

Key Takeaways for Improving Your Credit Score

- Keep your credit utilization below 30%, ideally under 10%

- Pay down balances before your statement closing date

- Increase credit limits without increasing spending

- Avoid closing old accounts

- Monitor both overall and per-card utilization

Small changes in how you manage your credit balances can lead to significant improvements in your credit score.

Take Control of Your Credit Today

Improving your credit utilization is one of the fastest ways to boost your credit score in the United States. Unlike other factors that take time, utilization can change quickly—and so can your score.

By understanding how it works and applying the right strategies, you can take control of your credit profile, reduce financial stress, and open the door to better financial opportunities.

If you’re serious about improving your credit score, start by reviewing your current balances and taking immediate action to lower your utilization. The results can be faster—and more impactful—than you might expect.

Learn more about our Credit Counselling Guidance