Middle East Conflict Drives Global Borrowing Costs to Multi-Year Highs, Squeezing Households Worldwide

March 2026 — Escalating conflict in the Middle East is sending shockwaves through global financial systems, pushing borrowing costs higher and tightening credit conditions for millions of consumers. From rising credit card interest rates to more expensive personal loans, households across both developed and emerging economies are beginning to feel the financial strain of a crisis unfolding thousands of miles away.

How the Middle East conflict affects global borrowing costs:

Oil Shock Rekindles Inflation Fears

The latest surge in geopolitical tensions has triggered a sharp rise in global oil prices, reigniting inflation concerns at a time when many central banks were preparing to ease monetary policy.

Brent crude prices have climbed significantly in recent weeks, driven by fears of supply disruptions in one of the world’s most critical energy-producing regions. Energy markets remain highly sensitive to developments in the Middle East, and even the risk of prolonged instability is enough to push prices upward.

Higher oil prices are already feeding into broader inflation, increasing transportation, manufacturing, and household energy costs. This has complicated the path forward for central banks, forcing them to reconsider planned interest rate cuts.

Central Banks Hold Firm as Rate Cuts Fade

Before the escalation, markets widely expected central banks to begin lowering interest rates in 2026. That outlook is now rapidly shifting.

Major institutions, including the U.S. Federal Reserve, the European Central Bank, and the Bank of England, are signaling a more cautious approach. Policymakers are increasingly concerned that easing rates too soon could allow inflation to rebound, particularly if energy prices remain elevated.

As a result, interest rates are expected to stay higher for longer — a move that directly impacts global borrowing costs.

“Geopolitical risks are now a key factor in monetary policy decisions,” said a senior market analyst at a leading investment firm. “Central banks cannot afford to loosen policy while inflation risks are rising again.”

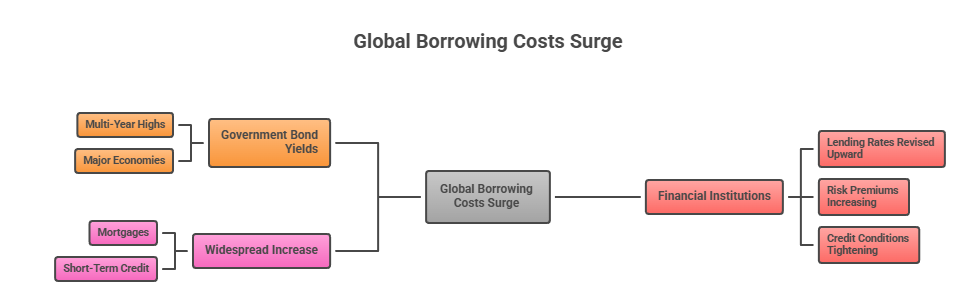

Global Borrowing Costs Surge

The impact of sustained high interest rates is being felt across global credit markets.

Government bond yields — a key benchmark for lending rates — have climbed to multi-year highs in several major economies. This increase is translating directly into higher borrowing costs for banks, businesses, and ultimately consumers.

Financial institutions are adjusting quickly:

- Lending rates are being revised upward

- Risk premiums are increasing

- Credit conditions are tightening

The result is a widespread increase in the cost of borrowing, affecting everything from mortgages to short-term credit.

Personal Loans Become Costlier and Harder to Access

For individuals seeking personal loans, the shift is already evident.

Banks and non-banking financial institutions are raising interest rates on unsecured loans, reflecting both higher funding costs and increased economic uncertainty. At the same time, lenders are becoming more selective.

Key Developments:

- Personal loan interest rates are rising across markets

- Approval criteria are becoming stricter

- Loan processing times are increasing

Borrowers with lower credit scores are facing the greatest challenges, with many applications being rejected or approved at significantly higher rates.

Credit Card Interest Rates Climb Sharply

Credit card users are among the most exposed to rising borrowing costs.

Unlike fixed-rate loans, credit card interest rates are directly linked to benchmark rates, meaning they adjust quickly when central banks maintain or increase rates.

In several markets, average credit card Annual Percentage Rates (APRs) have reached record levels. For consumers carrying balances, this translates into:

- Higher monthly interest charges

- Increased minimum payments

- Longer repayment periods

For many households, the cost of revolving credit is becoming increasingly difficult to manage.

Household Debt Pressures Intensify

The timing of rising borrowing costs is particularly challenging. Many households entered 2026 already carrying elevated levels of debt following years of inflation and economic uncertainty.

Now, with interest rates climbing again:

- Debt servicing costs are increasing

- Disposable incomes are shrinking

- Savings buffers are eroding

Economists warn that prolonged high borrowing costs could lead to a rise in delinquencies, particularly in unsecured credit segments such as personal loans and credit cards.

Emerging Markets Face Double Impact

While developed economies grapple with higher consumer borrowing costs, emerging markets are facing a more complex crisis.

Capital outflows, currency depreciation, and rising external debt costs are compounding the impact of global rate increases. Countries that rely heavily on imported energy are particularly vulnerable, as rising oil prices widen trade deficits and increase inflation.

This creates a feedback loop:

- Higher inflation leads to higher domestic interest rates

- Higher rates slow economic growth

- Slower growth increases financial stress

For consumers in these economies, access to affordable credit is becoming increasingly limited.

Banks Tighten Credit Amid Rising Risk

Financial institutions are responding defensively to the evolving situation.

With uncertainty increasing, banks are tightening lending standards to protect their balance sheets. This includes:

- Enhanced credit risk assessments

- Reduced loan exposure in high-risk segments

- Lower credit limits for existing customers

While these measures reduce systemic risk, they also restrict access to credit for many individuals and small businesses.

Markets Volatile as Investors Reprice Risk

Global financial markets have become increasingly volatile as investors reassess risk in light of geopolitical developments.

Equity markets have shown fluctuations, while bond yields continue to climb. Safe-haven assets such as gold are attracting renewed interest, reflecting heightened uncertainty.

This volatility is feeding back into credit markets, where lenders are pricing in higher risk premiums — further increasing borrowing costs.

A Shift in Consumer Financial Behavior

As borrowing becomes more expensive, households are beginning to adjust their financial behavior.

Early signs of change include:

- Reduced reliance on credit cards

- Increased focus on debt repayment

- Lower discretionary spending

Retail sectors and consumer-driven industries may feel the impact as spending slows, potentially affecting broader economic growth.

Outlook: Uncertainty Likely to Persist

The future trajectory of borrowing costs will depend heavily on how the Middle East conflict evolves.

If tensions escalate further:

- Oil prices could rise even higher

- Inflation may remain elevated

- Interest rates could stay restrictive for longer

If the situation stabilizes:

- Energy markets may calm

- Inflation pressures could ease

- Central banks may revisit rate cuts

However, analysts caution that even in a best-case scenario, borrowing costs are unlikely to return quickly to the ultra-low levels seen in previous years.

Global Events, Personal Consequences

The current crisis underscores the deep connection between global geopolitical events and everyday financial realities.

A conflict in the Middle East is now influencing:

- The interest rate on a personal loan

- The cost of carrying a credit card balance

- The financial stability of households worldwide

For consumers, the message is clear: the era of cheap credit is fading, and managing debt is becoming more critical than ever.