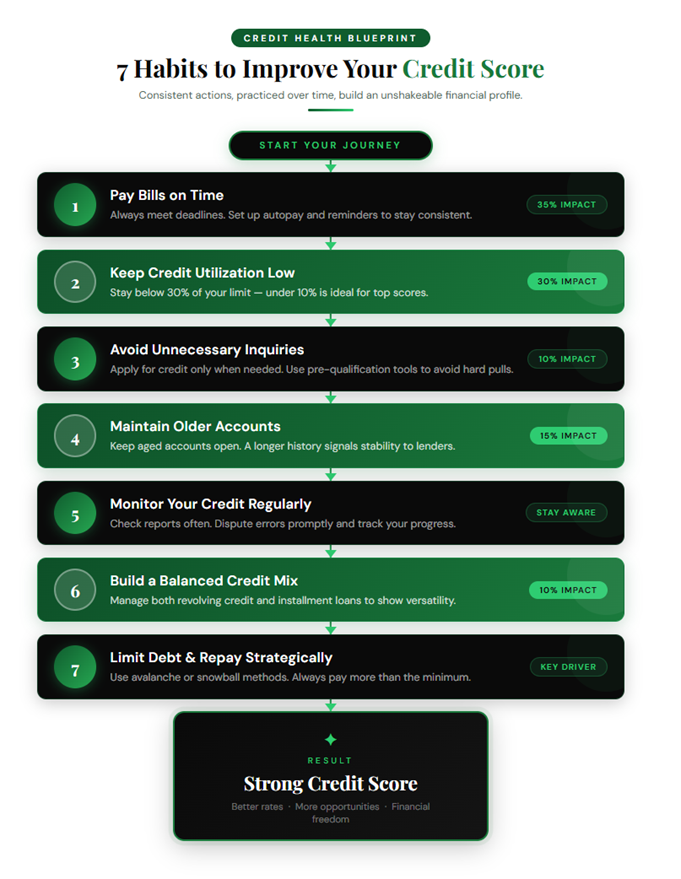

7 Habits That Improve Your Credit Score Over Time

Your credit score plays a critical role in shaping your financial future. Whether you’re applying for a personal loan, a mortgage, or a credit card, your creditworthiness determines not only your approval chances but also the interest rates and terms you receive. Yet, many people misunderstand how credit scores actually improve.

There is no instant solution or shortcut to achieving a high credit score. Instead, it’s the result of consistent financial behavior practiced over time. The good news is that by adopting the right habits, you can steadily build, repair, and maintain a strong credit profile.

If you’re looking to improve your credit score in a sustainable way, these seven habits form the foundation of long-term success.

7 Habits to Build a Strong Credit Score

1. Paying Bills on Time – The Cornerstone of Credit Health

Your payment history is the most influential factor in your credit score. It reflects whether you meet your financial obligations consistently, and lenders rely heavily on this behavior to assess your reliability.

Every payment you make—credit cards, loans, utilities, and other obligations—contributes to this record. Missing even a single payment can negatively impact your score and remain on your credit report for years.

Building a strong payment habit involves more than just avoiding late fees. It demonstrates financial discipline and reliability over time.

To stay consistent:

- Always pay at least the minimum amount due before the deadline

- Set up automatic payments for recurring bills

- Use reminders or budgeting apps to track due dates

- Align payment dates with your income cycle

If you’ve missed payments in the past, don’t get discouraged. Credit scoring models give more weight to recent activity. By consistently making on-time payments moving forward, you can gradually rebuild your score and offset previous mistakes.

2. Keeping Credit Utilization Low – Manage What You Use

Credit utilization refers to how much of your available credit you’re using at any given time. It’s one of the most important factors in determining your credit score after payment history.

A high utilization ratio signals that you may be over-reliant on credit, which increases perceived risk for lenders—even if you’re making payments on time.

For example, if you have a total credit limit of $10,000 and you’re using $7,000, your utilization is 70%, which is considered high.

Healthy utilization habits include:

- Keeping your usage below 30% of your total credit limit

- Aiming for under 10% for optimal scoring benefits

- Paying off balances multiple times a month if needed

- Avoiding maxing out credit cards

Another useful strategy is to request a credit limit increase (without increasing spending). This lowers your utilization ratio while keeping your spending stable.

Managing utilization effectively shows lenders that you are in control of your credit and not financially stretched.

3. Avoiding Unnecessary Credit Inquiries – Be Strategic

Each time you apply for credit, a hard inquiry is recorded on your credit report. While a single inquiry typically causes only a small, temporary dip in your score, multiple inquiries within a short period can have a cumulative negative effect.

Frequent applications may suggest financial instability or a higher likelihood of default, making lenders more cautious.

To minimize the impact:

- Apply for credit only when necessary

- Avoid submitting multiple applications at once

- Research eligibility criteria before applying

- Use pre-qualification tools that involve soft inquiries when available

It’s important to note that certain types of inquiries—such as those for rate shopping on mortgages or auto loans—are often grouped together if done within a short timeframe. Still, being selective and intentional about applications protects your credit profile.

4. Maintaining Older Accounts – The Value of Time

The length of your credit history is another key factor in your credit score. It includes the age of your oldest account, the age of your newest account, and the average age of all accounts.

A longer credit history provides more data for lenders to evaluate your financial behavior, which generally works in your favor.

Closing old accounts can:

- Shorten your average credit history

- Increase your credit utilization ratio

- Potentially lower your score

Instead, consider these practices:

- Keep older accounts open, even if you don’t use them frequently

- Use them occasionally for small purchases to keep them active

- Avoid closing accounts unless there is a strong reason (such as high fees)

Maintaining long-standing accounts demonstrates stability and consistency—two qualities that lenders highly value.

5. Monitoring Your Credit Regularly – Stay Informed and Alert

Regularly checking your credit report is an essential habit for maintaining and improving your score. It helps you understand where you stand and identify potential issues before they become serious problems.

Errors on credit reports are more common than many people realize. Incorrect account information, outdated balances, or even fraudulent activity can negatively impact your score.

By monitoring your credit:

- You can detect inaccuracies and dispute them promptly

- You stay aware of changes in your score

- You track the effectiveness of your financial habits

Make it a routine to review your credit report from major credit bureaus. Many platforms offer free access to your credit score and report, making it easier than ever to stay informed.

Being proactive with monitoring ensures that your credit profile accurately reflects your financial behavior.

6. Building a Balanced Credit Mix – Show Versatility

Credit scoring models consider the variety of credit accounts you manage. A healthy mix typically includes both revolving credit (such as credit cards) and installment loans (such as personal loans, auto loans, or mortgages).

Having a diverse credit portfolio shows that you can handle different types of financial obligations responsibly.

However, this doesn’t mean you should open new accounts unnecessarily. The goal is to demonstrate responsible management of the credit you already have.

Best practices:

- Maintain a mix of credit types over time

- Avoid opening accounts solely to improve your score

- Focus on managing existing accounts effectively

A balanced credit mix enhances your profile and provides lenders with a more complete picture of your financial capabilities.

7. Limiting Debt and Following a Clear Repayment Strategy

Excessive debt is one of the biggest barriers to a strong credit score. High balances increase your credit utilization and make it harder to keep up with payments.

Developing a structured repayment strategy is essential for reducing debt and improving your credit health.

Effective approaches include:

- Prioritizing high-interest debts first (avalanche method)

- Paying off smaller balances to build momentum (snowball method)

- Making more than the minimum payment whenever possible

- Avoiding new debt while repaying existing obligations

Consistency is key. Even small additional payments can significantly reduce your overall debt over time and improve your credit score.

Reducing debt not only boosts your credit profile but also improves your overall financial well-being and peace of mind.

The Power of Consistency in Credit Building

Improving your credit score is not about dramatic changes—it’s about consistent, responsible behavior over time. Each positive action you take contributes to a stronger financial profile.

These habits work together to:

- Build trust with lenders

- Reduce financial risk

- Increase access to better credit opportunities

It’s important to be patient. Credit improvement is gradual, but the results are long-lasting.

Build a Stronger Financial Future Starting Today

Your credit score reflects your financial habits. By focusing on these seven key behaviors—paying on time, managing utilization, limiting inquiries, maintaining accounts, monitoring your report, diversifying credit, and reducing debt—you can steadily improve your score and create a solid financial foundation.

Start with small, manageable changes and stay consistent. Over time, these habits will not only improve your credit score but also give you greater control over your financial future.

A better credit score isn’t just about borrowing—it’s about building stability, confidence, and long-term financial freedom.

Learn more about our Credit Counselling Guidance