CuraDebts Review 2026: Is CuraDebts Legitimate or Just Another Debt Trap?

Affiliate Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. Disclosure Policy

Debt can feel overwhelming—especially when collection calls don’t stop, interest keeps piling up, and every solution online sounds too good to be true. If you’re here, chances are you’ve come across CuraDebts and are wondering: Is this actually legitimate, or just another company promising relief without results?

That’s a valid concern. In 2026, with so many debt relief services operating globally, it’s important to separate genuine help from risky shortcuts. This review is designed to give you a clear, honest, and practical understanding of CuraDebts—how it works, who it’s for, and whether it’s worth considering for your situation.

What Is CuraDebts and How Does It Work?

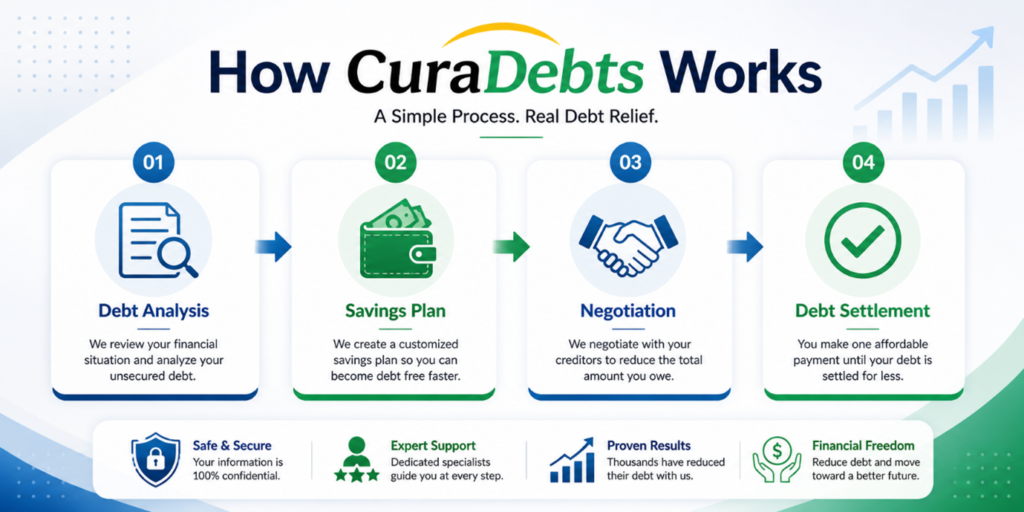

CuraDebts is a debt relief service that helps individuals manage and reduce unsecured debts, including credit card debt, personal loans, and medical bills. Instead of offering loans, CuraDebts typically works through negotiation strategies aimed at reducing the total amount you owe.

The core idea is simple:

- You stop making direct payments to creditors

- Funds are redirected into a structured repayment plan

- CuraDebts negotiates settlements with creditors on your behalf

This approach is commonly known as debt settlement, and it’s designed for people who are already struggling to keep up with minimum payments.

Within the first step of the process, you’ll usually go through a financial evaluation to determine eligibility. This includes reviewing your income, total debt, and financial hardship.

If you’re unsure whether this approach fits your situation, you can see if CuraDebts is right for you before committing to anything.

Is CuraDebts Legitimate in 2026?

Yes—CuraDebts operates as a legitimate debt relief provider. However, legitimacy doesn’t automatically mean it’s the right choice for everyone.

Here’s what makes it credible:

- It follows standard debt settlement practices used across the industry

- It does not promise instant debt elimination (a major red flag if any company does)

- It typically charges fees only after settlements are reached

- It offers consultation before enrollment

That said, debt settlement companies—including CuraDebts—operate in a complex space. Results depend heavily on your financial condition, creditor cooperation, and your commitment to the program.

So while CuraDebts is legitimate, it’s not a magic fix.

Who Should Consider CuraDebts?

CuraDebts may be suitable if:

- You are struggling with high unsecured debt

- You are already missing or close to missing payments

- Minimum payments are no longer manageable

- You want to avoid bankruptcy but need structured relief

However, it may not be ideal if:

- You can still comfortably make payments

- Your debt is primarily secured (like mortgages or auto loans)

- You are looking for a quick fix without financial discipline

Debt settlement requires patience. Programs often take 24–48 months to complete. Check out Now!

How CuraDebts Helps Reduce Debt

The strategy behind CuraDebts is negotiation leverage. When accounts become delinquent, creditors may be willing to accept a reduced lump sum rather than risk getting nothing.

CuraDebts facilitates this by:

- Building a negotiation timeline

- Communicating directly with creditors

- Structuring settlement offers

- Guiding you through repayment planning

This doesn’t erase debt overnight—but it can significantly reduce the total amount owed if executed properly.

Pros and Cons of CuraDebts

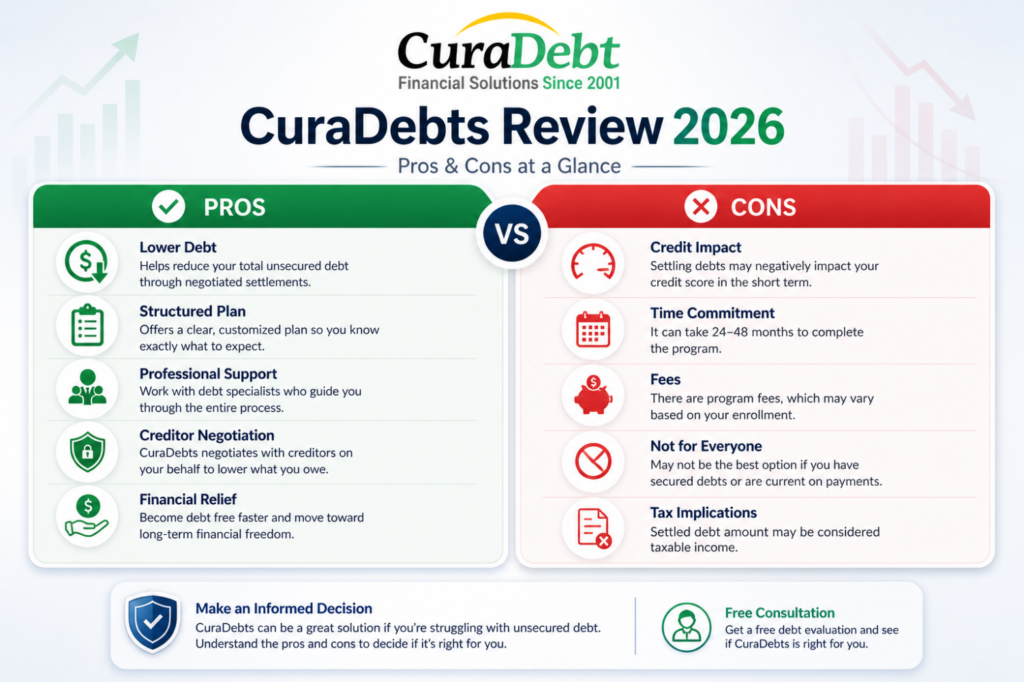

Advantages

1. Potential Debt Reduction

You may end up paying less than your original balance if settlements are successful.

2. Structured Plan

Instead of juggling multiple creditors, you follow a single, organized program.

3. Avoid Bankruptcy (In Some Cases)

For many, this is a middle ground between struggling payments and legal insolvency.

4. Professional Negotiation

Handling creditors directly can be stressful—this service takes over that responsibility.

Limitations

1. Credit Score Impact

Missed payments and settlements can negatively affect your credit profile.

2. No Guaranteed Results

Creditors are not obligated to settle, and outcomes vary.

3. Time Commitment

Programs can take several years to complete.

4. Fees Apply

While typically performance-based, fees can still be significant.

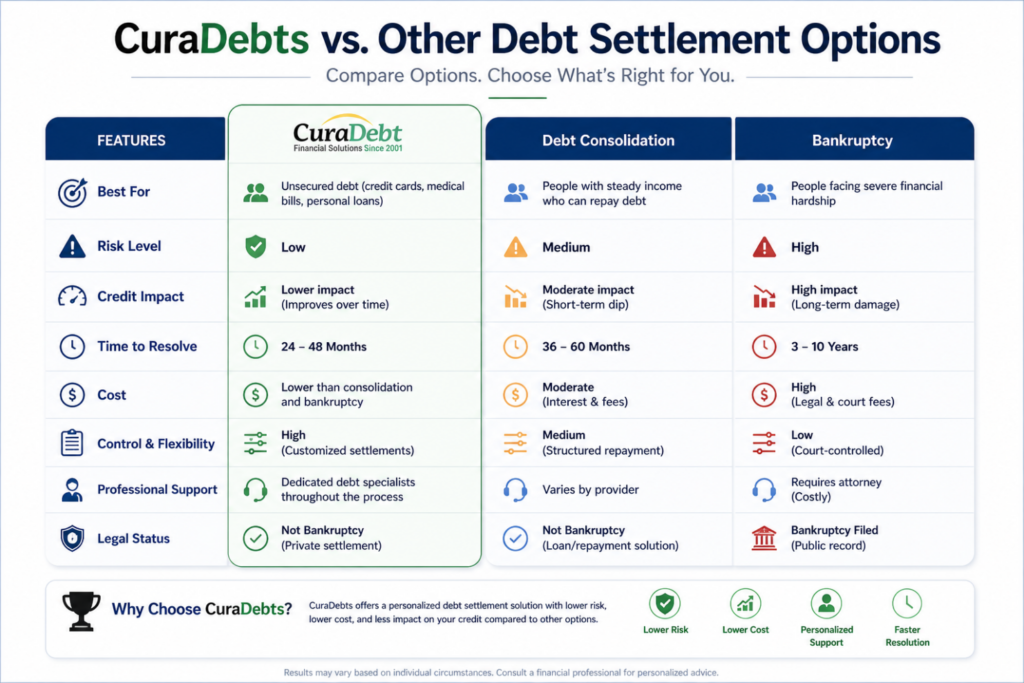

CuraDebts vs Alternatives: What’s Better?

To truly evaluate CuraDebts, you need to compare it with other available options.

CuraDebts vs Debt Consolidation

- Debt Consolidation combines multiple debts into one loan with a lower interest rate

- CuraDebts (Settlement) reduces the total amount owed

Choose consolidation if your credit is still good

Choose settlement if you’re already in financial distress

CuraDebts vs Credit Counseling

- Credit Counseling focuses on budgeting and structured repayment

- CuraDebts aims to reduce principal balances

Counseling is ideal for early-stage debt

CuraDebts fits more difficult situations

CuraDebts vs Bankruptcy

- Bankruptcy is a legal reset, but comes with long-term consequences

- CuraDebts offers a non-legal alternative

- Bankruptcy is faster but more damaging

- CuraDebts is slower but less severe (in many cases)

What Realistically Happens After You Enroll?

Understanding expectations is critical.

Here’s a simplified timeline:

Month 1–3:

- Financial evaluation and program setup

- You begin saving toward settlements

Month 4–12:

- Accounts may become delinquent

- Negotiations begin

Year 1–3:

- Settlements are reached

- Payments are made gradually

During this period, communication and consistency are key. Missing program payments can delay results.

Common Misconceptions About CuraDebts

“It wipes out all debt instantly.”

False. Debt reduction happens over time through negotiation.

“It damages your credit permanently.”

Not necessarily. While there is a short-term impact, recovery is possible.

“It works for everyone.”

No solution fits all financial situations.

Is CuraDebts Safe to Use?

Safety depends on expectations and transparency.

CuraDebts is generally considered safe if:

- You understand the process

- You are committed to completing the program

- You avoid unrealistic expectations

Always read agreements carefully and ensure you’re clear about fees and timelines.

Key Things to Check Before Choosing CuraDebts

Before moving forward, ask yourself:

- Can I commit to a long-term repayment plan?

- Am I already struggling to keep up with debt payments?

- Do I understand the impact on my credit?

- Have I explored other options?

Taking a step back and evaluating your situation objectively is crucial.

Final Verdict: Is CuraDebts Worth It in 2026?

CuraDebts is a legitimate option in the debt relief space, but it’s not a one-size-fits-all solution. It works best for individuals facing serious financial strain who need structured negotiation support to reduce their debt burden.

If you’re looking for a quick fix, this isn’t it. But if you’re willing to commit to a process that prioritizes long-term financial recovery, CuraDebts can be a practical path forward.

The key is clarity—knowing exactly what you’re signing up for and aligning it with your financial reality.

Take the Next Step Toward Debt Relief

Debt doesn’t resolve itself—and waiting often makes it worse. If you’re seriously considering a solution, the best move is to evaluate your options early.

Start your free session today — no obligation.

Understanding your choices now can save you years of financial stress later.