Types of Consumer Debt Explained: Credit Cards, Loans & More

Consumer debt has become a major part of everyday financial life. From credit cards and personal loans to auto financing and student borrowing, millions of people rely on different forms of debt to manage expenses, achieve goals, or handle emergencies. While debt can provide financial flexibility and opportunities, it can also create long-term financial pressure when not managed properly.

Understanding the different types of consumer debt is essential for making smarter financial decisions. Each form of debt comes with unique features, interest rates, repayment terms, and risks. Knowing how they work can help consumers avoid financial stress, reduce interest costs, and improve their overall financial health.

This guide explains the major types of consumer debt, including credit card debt, personal loans, auto loans, student loans, and the difference between secured and unsecured debt.

What Is Consumer Debt?

Consumer debt refers to money borrowed by individuals for personal, family, or household purposes. Unlike business debt, consumer debt is used to purchase goods, services, education, vehicles, or other personal needs.

Consumer debt is usually borrowed through banks, credit unions, financial institutions, online lenders, or credit card companies. Borrowers agree to repay the money over time, often with added interest and fees.

Common examples of consumer debt include:

- Credit card balances

- Personal loans

- Student loans

- Auto loans

- Mortgage loans

- Buy now, pay later services

- Medical debt

Consumer debt can either help build financial stability or create financial hardship depending on how responsibly it is managed.

Why Consumer Debt Is So Common

Modern lifestyles often require access to borrowed money. Rising living costs, inflation, education expenses, healthcare bills, and emergency situations push many consumers toward credit solutions.

Some common reasons people take on consumer debt include:

- Managing temporary cash shortages

- Purchasing a vehicle

- Paying for higher education

- Covering medical emergencies

- Financing home improvements

- Consolidating existing debts

- Building a credit history

When used carefully, debt can support financial growth. However, excessive borrowing can lead to missed payments, damaged credit scores, and long-term financial instability.

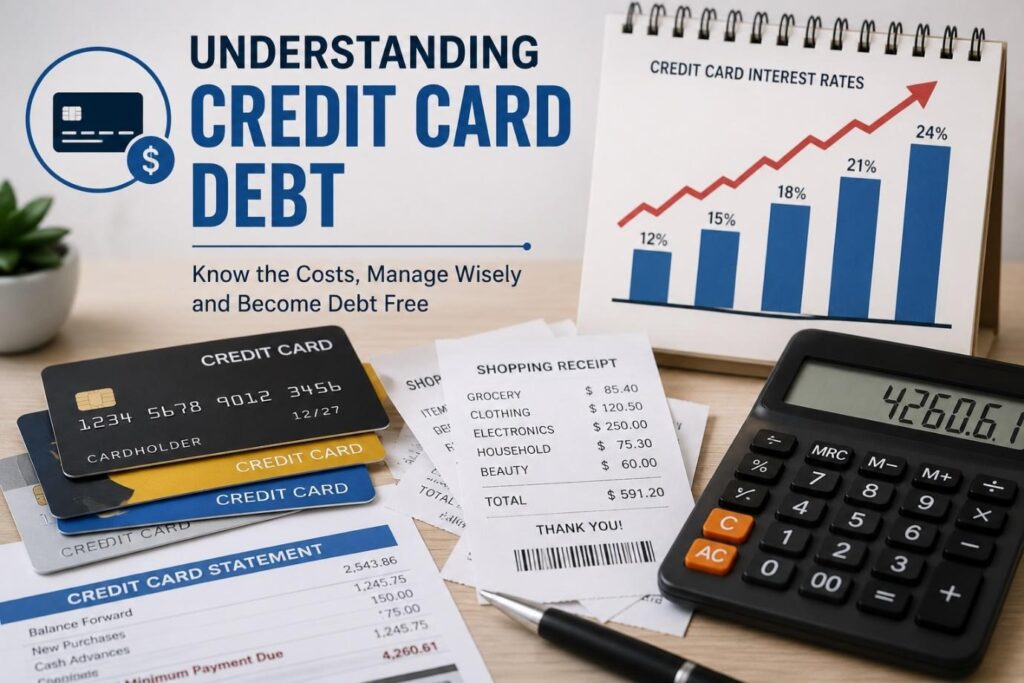

Credit Card Debt

Credit card debt is one of the most common forms of consumer debt worldwide. Credit cards allow consumers to borrow money up to a certain credit limit for purchases, online shopping, travel, dining, and everyday expenses.

How Credit Card Debt Works

When a person uses a credit card, the issuer pays the merchant on behalf of the cardholder. The borrower must then repay the amount either in full or through monthly payments.

If the full balance is not paid before the due date, interest charges are added to the remaining balance. Over time, unpaid balances can grow rapidly because of high interest rates.

Features of Credit Card Debt

- Revolving credit system

- Minimum monthly payments

- High interest rates

- Flexible spending

- Reward programs and cashback offers

Credit card debt is considered convenient because consumers can repeatedly borrow and repay within their approved credit limit.

Risks of Credit Card Debt

Although credit cards offer convenience, they can become financially dangerous when misused. High interest rates make it easy for balances to grow quickly.

Common problems include:

- Overspending

- Late payment penalties

- Increasing interest charges

- Declining credit scores

- Long-term debt accumulation

Consumers who only make minimum payments may remain in debt for years.

Tips for Managing Credit Card Debt

- Pay balances in full whenever possible

- Avoid unnecessary spending

- Make payments before the due date

- Keep credit utilization low

- Avoid using multiple cards excessively

Responsible credit card usage can help build a strong credit history and improve financial flexibility.

Personal Loans

Personal loans are another popular type of consumer debt. These loans provide borrowers with a lump sum amount that must be repaid over a fixed period through monthly installments.

Personal loans can be used for many purposes, including:

- Debt consolidation

- Emergency expenses

- Medical bills

- Weddings

- Home renovations

- Travel expenses

How Personal Loans Work

A lender approves a specific loan amount based on the borrower’s income, credit score, and repayment ability. The borrower then repays the loan with interest over a fixed term, usually ranging from one to seven years.

Unlike credit cards, personal loans typically have fixed repayment schedules and fixed interest rates.

Advantages of Personal Loans

- Predictable monthly payments

- Lower interest rates than many credit cards

- Fast access to funds

- Useful for debt consolidation

- Fixed repayment period

Debt consolidation loans can simplify finances by combining multiple debts into one monthly payment.

Risks of Personal Loans

While personal loans may seem attractive, borrowers should still exercise caution.

Potential risks include:

- High interest rates for poor credit borrowers

- Loan origination fees

- Penalties for missed payments

- Increased debt burden

Taking out unnecessary personal loans can worsen financial problems instead of solving them.

Auto Loans

Auto loans help consumers purchase vehicles without paying the full cost upfront. Most people rely on financing when buying a car, truck, or motorcycle.

How Auto Loans Work

In an auto loan agreement, the lender provides funds to purchase the vehicle. The borrower then repays the loan through monthly payments over several years.

The vehicle itself serves as collateral for the loan. If payments are missed, the lender may repossess the vehicle.

Features of Auto Loans

- Fixed monthly payments

- Loan terms typically between three and seven years

- Vehicle used as collateral

- Interest rates based on creditworthiness

Auto loans are considered secured debt because the lender has legal rights to the vehicle until the loan is fully repaid.

Benefits of Auto Loans

- Makes vehicle ownership more accessible

- Allows consumers to spread costs over time

- Can help build credit history

Risks of Auto Loans

Auto loans can become problematic when consumers borrow more than they can comfortably repay.

Common issues include:

- Negative equity

- High interest costs

- Vehicle depreciation

- Repossession risk

Long loan terms may reduce monthly payments but increase total interest paid over time.

Student Loans

Student loans are designed to help individuals pay for education-related expenses such as tuition, accommodation, books, and living costs.

Education costs continue to rise globally, making student borrowing increasingly common.

How Student Loans Work

Students borrow money from government programs or private lenders and repay the loans after graduation or after leaving school.

Repayment terms vary depending on the lender and loan type.

Types of Student Loans

There are generally two major categories:

Federal Student Loans

Government-backed student loans often provide:

- Lower interest rates

- Flexible repayment plans

- Deferred payments during studies

- Income-driven repayment options

Private Student Loans

Private lenders offer student loans based on creditworthiness and financial history.

These loans may have:

- Higher interest rates

- Fewer repayment protections

- Variable interest options

Advantages of Student Loans

- Increases access to higher education

- Helps students invest in future careers

- Flexible repayment structures in some cases

Risks of Student Loans

Student debt can create long-term financial challenges, especially for graduates with low incomes or unstable employment.

Common problems include:

- Large debt balances

- Long repayment periods

- Interest accumulation

- Delayed financial milestones

Many borrowers struggle with student debt for decades after graduation.

Mortgage Debt

Mortgage loans are among the largest forms of consumer debt. These loans help consumers purchase homes or real estate properties.

How Mortgage Loans Work

A mortgage lender provides financing for a home purchase, and the borrower repays the loan over a long-term period, often 15 to 30 years.

The property serves as collateral.

Features of Mortgage Debt

- Lower interest rates compared to unsecured debt

- Long repayment periods

- Fixed or variable interest options

- Secured by property

Mortgage debt can help consumers build wealth through homeownership, but missed payments can lead to foreclosure.

Medical Debt

Medical debt occurs when consumers cannot fully pay healthcare expenses.

Unexpected medical emergencies, surgeries, hospital stays, or treatments often result in significant debt burdens.

Why Medical Debt Is Increasing

Healthcare costs continue to rise in many countries, causing more people to rely on financing or payment plans.

Medical debt may involve:

- Hospital bills

- Prescription costs

- Emergency treatment

- Insurance gaps

Medical debt can damage credit scores and create severe financial stress for families.

Buy Now, Pay Later Debt

Buy now, pay later services have become increasingly popular in online shopping.

These services allow consumers to split purchases into smaller installment payments.

Risks of Buy Now, Pay Later Services

Although these programs appear convenient, they may encourage overspending.

Potential risks include:

- Multiple repayment obligations

- Late fees

- Credit score impacts

- Accumulating hidden debt

Consumers should carefully monitor installment spending to avoid financial problems.

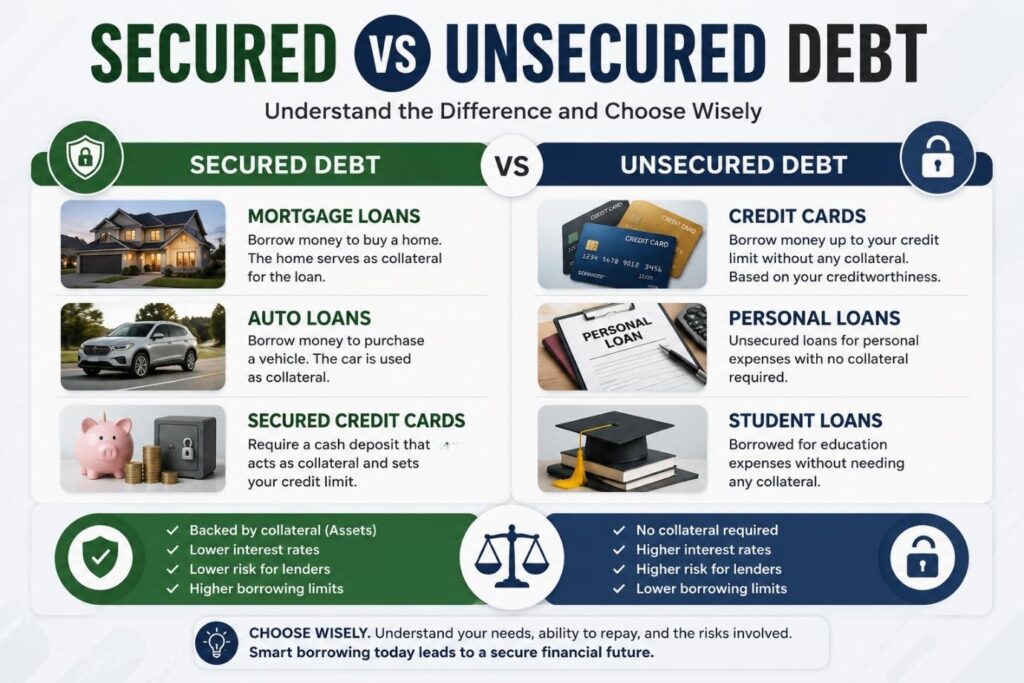

Secured vs Unsecured Debt

One of the most important concepts in consumer finance is understanding the difference between secured and unsecured debt.

What Is Secured Debt?

Secured debt is backed by collateral. The borrower pledges an asset that the lender can seize if payments are not made.

Examples of secured debt include:

- Auto loans

- Mortgage loans

- Secured credit cards

Advantages of Secured Debt

- Lower interest rates

- Easier approval

- Higher borrowing limits

Risks of Secured Debt

If borrowers fail to repay secured debt, they risk losing their assets.

For example:

- Missed mortgage payments may lead to foreclosure

- Missed auto loan payments may result in repossession

What Is Unsecured Debt?

Unsecured debt does not require collateral. Approval depends mainly on the borrower’s creditworthiness and income.

Examples include:

- Credit card debt

- Personal loans

- Student loans

- Medical debt

Advantages of Unsecured Debt

- No collateral required

- Faster approval process

- Greater flexibility

Risks of Unsecured Debt

Because lenders face more risk, unsecured debt often carries higher interest rates.

Failure to repay unsecured debt can lead to:

- Collection actions

- Lawsuits

- Credit score damage

- Wage garnishment in some cases

How Consumer Debt Affects Credit Scores

Consumer debt plays a major role in determining credit scores.

Lenders evaluate factors such as:

- Payment history

- Credit utilization

- Debt balances

- Loan mix

- Length of credit history

Responsible borrowing and timely payments can improve credit scores, while excessive debt and missed payments can severely damage financial credibility.

Signs of Unhealthy Debt

Consumers should watch for warning signs that debt is becoming unmanageable.

Common signs include:

- Struggling to make minimum payments

- Using credit cards for essential expenses

- Frequently borrowing to repay existing debt

- Receiving collection calls

- Maxed-out credit cards

- Missing loan payments

Recognizing these warning signs early can help prevent serious financial consequences.

Strategies for Managing Consumer Debt

Managing debt effectively requires discipline and financial planning.

Helpful strategies include:

Create a Monthly Budget

Tracking income and expenses helps consumers understand where money is being spent.

Prioritize High-Interest Debt

Paying off high-interest debt first can reduce long-term borrowing costs.

Build an Emergency Fund

Savings can help avoid reliance on credit during emergencies.

Avoid Unnecessary Borrowing

Consumers should carefully evaluate whether new debt is truly necessary.

Seek Professional Financial Advice

Debt consultants and financial counselors can help create repayment strategies and negotiate with creditors.

Building a Healthier Financial Future

Consumer debt is not always negative. In many cases, borrowing helps individuals achieve important life goals such as education, transportation, and homeownership. However, understanding the different types of consumer debt is critical for making informed financial decisions.

Credit card debt, personal loans, auto loans, student loans, and other borrowing options each come with unique advantages and risks. Learning how secured and unsecured debt works can help consumers borrow responsibly and protect their financial future.

By managing debt carefully, making timely payments, and avoiding excessive borrowing, consumers can reduce financial stress, improve credit health, and build long-term financial stability.

Learn more about our Credit Counselling Guidance