Debt Snowball vs. Avalanche: The Ultimate Showdown to Financial Freedom

Debt. The word itself can trigger a cascade of anxiety, a heavy burden that weighs on your shoulders. For millions, it’s a constant source of stress, limiting choices and hindering future plans. But here’s the good news: escaping the clutches of debt isn’t just a pipe dream; it’s an achievable reality. The financial world offers two powerful, battle-tested strategies to accelerate your journey to debt freedom: the Debt Snowball and the Debt Avalanche. Both are championed by financial gurus and everyday success stories alike, promising a clear path out of the red. Yet, for many, the critical question remains: which method truly saves more money in the long run? Which one is the right fit for your unique financial journey? This comprehensive guide will dissect both approaches, weigh their pros and cons, and help you determine the optimal strategy to reclaim your financial future.

Unpacking the Debt Snowball Method: A Psychological Powerhouse

The Debt Snowball Method isn’t just a financial strategy; it’s a masterclass in behavioural psychology. Its core principle is beautifully simple: conquer your debts from the smallest balance to the largest, regardless of their interest rates. This method is designed to build momentum, to provide tangible, quick wins that fuel your motivation and keep you committed.

Here’s a breakdown of how the Debt Snowball method works in practice:

- List Your Debts: Begin by meticulously listing all your outstanding debts, arranging them from the smallest balance to the largest. Ignore interest rates for now; the focus here is purely on the principal amount.

- Minimum Payments are Key: For all debts except the smallest one, commit to making only the minimum required payments each month. This ensures you avoid late fees and maintain a good standing with your creditors.

- Target the Smallest: Now, take any extra funds you can muster – that bonus from work, savings from cutting discretionary spending, or extra income from a side hustle – and aggressively apply it to the debt with the smallest balance. This is your primary target.

- Roll and Repeat: Once that smallest debt is completely paid off, celebrate your victory! Then, take the money you were previously paying on that debt (both the minimum payment and any extra funds) and “roll” it into the payment for the next smallest debt on your list. Continue this snowballing process, building a larger and larger payment as each debt is eliminated, until you are entirely debt-free.

Why the Debt Snowball Method Resonates with So Many:

- Quick Wins & Psychological Boost: There’s an undeniable rush that comes with paying off a debt, no matter how small. These early victories provide a powerful psychological boost, demonstrating that your efforts are yielding tangible results.

- Motivation & Momentum: Each debt you eliminate acts like a snowball rolling downhill, gathering size and speed. This momentum is crucial, especially when the journey to debt freedom feels long and arduous.

- Simplicity & Ease of Use: The Debt Snowball is remarkably straightforward to understand and implement. Its simplicity reduces the potential for confusion or overwhelm, making it an accessible starting point for anyone feeling daunted by their debt.

This method prioritizes consistency and emotional engagement over pure mathematical optimization. It’s about keeping you in the game, building confidence, and transforming the often arduous journey to debt freedom into a series of achievable milestones.

Demystifying the Debt Avalanche Method: The Mathematically Superior Approach

In stark contrast to the Debt Snowball’s psychological focus, the Debt Avalanche Method is a beacon of mathematical efficiency. This strategy is laser-focused on minimizing the total interest paid over the life of your debts, ultimately getting you debt-free in the shortest possible time frame. It prioritizes debts with the highest interest rates, recognizing that these are the ones costing you the most money.

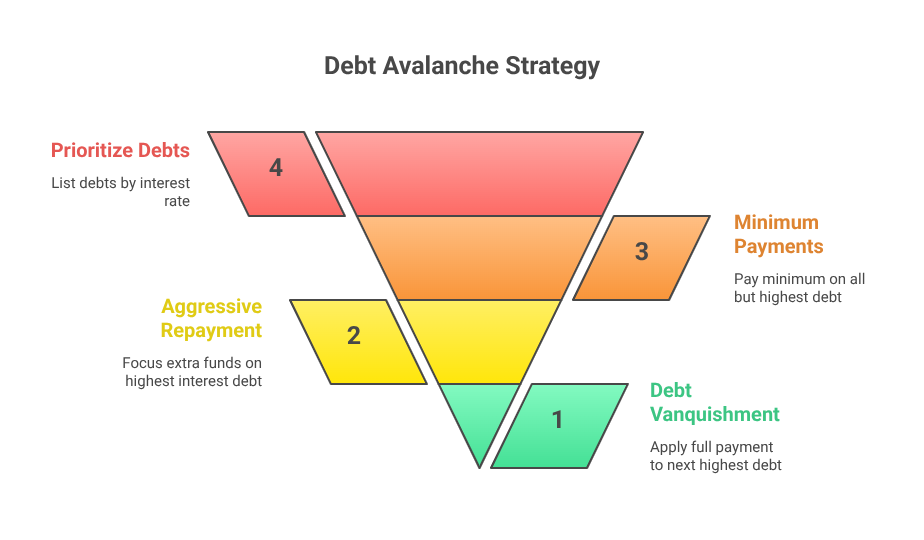

Here’s how to implement the Debt Avalanche method:

- Prioritize by Interest Rate: Your first step is to list all your debts, but this time, arrange them from the highest interest rate to the lowest interest rate. The balance size is secondary here.

- Minimum Payments for All But One: Similar to the Snowball, you’ll make the minimum required payments on all your debts, except for the one with the absolute highest interest rate.

- Attack the Highest Interest Debt: Every extra dollar you have available for debt repayment should be directed squarely at the debt carrying the highest interest rate. This is where you’ll make your aggressive principal payments.

- Move to the Next Highest: Once the highest-interest debt is completely vanquished, take the full payment amount you were dedicating to it (minimum + extra funds) and apply it to the debt with the next highest interest rate. Continue this methodical process until every debt is gone.

Why Financial Experts Champion the Debt Avalanche Method:

- Maximum Interest Savings: This is the undeniable champion for saving the most money. By systematically eliminating the debts that accrue the most interest first, you significantly reduce the overall cost of your debt.

- Fastest Path to Freedom: Because you’re tackling the most expensive debts first, you are mathematically optimized to become debt-free in the quickest possible time, assuming consistent payments.

- Efficiency & Optimization: For those who are highly motivated by financial efficiency and tangible savings, the Avalanche method provides a clear, logical, and highly effective path to debt elimination.

The Debt Avalanche method appeals to individuals who are driven by the numbers, who can see the long-term benefit of greater savings, and who possess the discipline to persevere even if immediate progress feels less dramatic.

Snowball vs. Avalanche: A Head-to-Head Comparison with Real-World Implications

Let’s bring this comparison to life with a practical example. Imagine you have the following debts, and you’re committed to paying an extra $300 per month towards them:

| Debt Type | Balance | Interest Rate | Minimum Payment |

|---|---|---|---|

| Credit Card A | $1,000 | 18% | $50 |

| Credit Card B | $5,000 | 22% | $125 |

| Personal Loan | $7,000 | 10% | $200 |

| Auto Loan | $15,000 | 6% | $275 |

Applying the Debt Snowball Method:

Following the Snowball method, your focus is solely on the smallest balance. You would prioritize them in this order:

- Credit Card A ($1,000)

- Credit Card B ($5,000)

- Personal Loan ($7,000)

- Auto Loan ($15,000)

You’d pay the minimums on Credit Card B, Personal Loan, and Auto Loan, and direct your extra $300 (plus Credit Card A’s minimum $50) towards Credit Card A until it’s gone. Then, that full payment rolls into Credit Card B, and so on.

Applying the Debt Avalanche Method:

With the Avalanche method, interest rate is king. Your payment order would be:

- Credit Card B (22%)

- Credit Card A (18%)

- Personal Loan (10%)

- Auto Loan (6%)

Here, you’d make minimum payments on Credit Card A, Personal Loan, and Auto Loan, while channelling your extra $300 (plus Credit Card B’s minimum $125) to Credit Card B until it’s paid off. Then, that total payment would shift to Credit Card A, and so forth.

The Indisputable Result:

When all the calculations are done, the Debt Avalanche Method will unequivocally save you more money on interest over the lifetime of your debts. It also typically results in becoming debt-free a few months earlier than the Snowball Method, assuming unwavering commitment. This is the mathematical truth.

However, the human element cannot be overlooked. Many individuals, despite the financial benefits, find it challenging to stick with the Avalanche method, particularly at the beginning, because they don’t see debts being eliminated as quickly. The emotional reward of the Debt Snowball’s quick wins often proves to be a more powerful motivator, keeping people engaged in their debt-free journey even if it comes at a slightly higher total cost.

Pros and Cons: A Balanced View of Each Strategy

Understanding the inherent strengths and weaknesses of both methods is crucial for making an informed decision.

Debt Snowball Pros:

- Encourages Consistency: The rapid succession of debt payoffs builds a strong habit of consistent repayment.

- Easier for Beginners: Its simplicity makes it less intimidating for those new to structured debt repayment.

- Builds Good Habits: It fosters discipline and teaches the power of focused financial effort.

- Boosts Emotional Motivation: The “quick wins” are powerful psychological reinforcers, making the process feel less like a grind.

Debt Snowball Cons:

- Higher Overall Interest Paid: This is its main mathematical drawback. You’ll end up paying more in interest over time.

- Not the Fastest Path to Zero Debt: While it feels fast due to early wins, it’s not the most efficient in terms of time to debt freedom.

Debt Avalanche Pros:

- Saves the Most Money: This is its undisputed strength. By targeting high-interest debt, it minimizes your total interest payments.

- Gets You Debt-Free Faster: Mathematically, it’s the most efficient way to eliminate all your debts.

- Mathematically Superior: For anyone focused purely on financial optimization, the Avalanche is the clear winner.

Debt Avalanche Cons:

- Less Emotionally Rewarding at First: If your highest-interest debt is also a large one, it can take a while to pay it off, leading to a feeling of slow progress.

- Requires Discipline and Patience: This method demands a higher degree of self-discipline to stick with it through the initial lack of rapid debt elimination.

- Progress Can Feel Slow Initially: Without the immediate gratification of small debts disappearing, some may lose motivation.

Choosing the Right Strategy for You: A Personalized Approach

The “best” method isn’t universal; it’s deeply personal. The most effective strategy is the one you can commit to consistently and successfully. Ask yourself these critical questions to guide your decision:

- Are you easily motivated by tangible progress and quick victories? If seeing debts disappear quickly keeps you energized, the Debt Snowball might be your ideal starting point.

- Is your primary goal to save every possible dollar and get out of debt as quickly as mathematically possible, even if it means delayed gratification? If so, the Debt Avalanche is the clear choice.

- Have you struggled with financial consistency or adherence to budgets in the past? The psychological wins of the Snowball can be invaluable for building initial momentum and discipline. Consider starting with Snowball and potentially transitioning later.

- Are you inherently disciplined and analytical with your finances? If you’re unfazed by large numbers and driven by efficiency, the Debt Avalanche will yield the greatest financial return.

Can You Blend Both Methods? The Hybrid Approach

Absolutely! There’s no rule that says you must strictly adhere to one method. Many financially savvy individuals successfully combine elements of both the Snowball and Avalanche to create a customized debt repayment plan that perfectly suits their personality and financial goals.

For instance, you might:

- Start with the Snowball: Use the Debt Snowball for your first one or two smallest debts. This builds crucial momentum, confidence, and establishes good payment habits.

- Transition to Avalanche: Once you’ve built that initial psychological push and feel more disciplined, you can then switch gears and apply the Debt Avalanche principle to your remaining, higher-interest debts.

This hybrid approach offers a powerful blend: the immediate motivational boost of quick wins, followed by the long-term financial optimization of interest savings. It’s the best of both worlds, offering flexibility and adaptability to your evolving financial discipline.

What the Experts Say: A Unified Message

While personal finance experts like Dave Ramsey champion the Debt Snowball for its behavioural effectiveness, and economists often lean towards the Debt Avalanche for its mathematical superiority, there’s a powerful consensus among them on one fundamental truth: having a debt repayment plan is paramount. Both the Debt Snowball and the Debt Avalanche are vastly superior to merely making minimum payments or haphazardly choosing which debt to tackle next. The key is intentionality and commitment.

Universal Tips to Maximize Results with Any Method

Regardless of whether you choose the motivational power of the Snowball, the financial efficiency of the Avalanche, or a clever hybrid, these foundational financial habits will dramatically accelerate your journey to debt freedom:

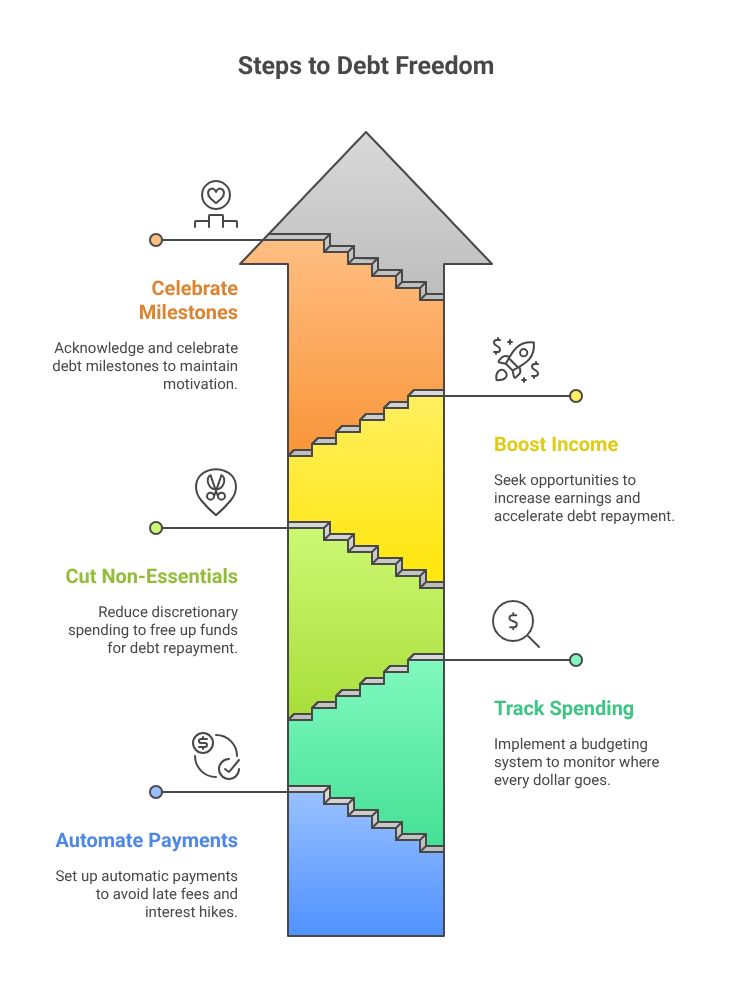

- Automate Your Payments: Set up automatic payments for all your minimums, and if possible, for your extra targeted payments too. This ensures you never miss a due date, avoiding late fees and potential interest rate hikes that can derail your progress.

- Track Every Dollar Religiously: Implement a robust budgeting system. Whether it’s a detailed spreadsheet, a budgeting app, or a simple pen and paper, knowing exactly where every dollar goes provides clarity and empowers you to make smarter financial decisions. Clarity is control.

- Ruthlessly Cut Non-Essential Spending: Every single dollar freed up from discretionary spending can be directly applied to your debt. Review your subscriptions, reduce dining out, pack lunches, and find areas where you can trim expenses without significantly impacting your quality of life. Redirecting these savings to your debt is a game-changer.

- Boost Your Income: Actively seek opportunities to increase your earnings. This could involve taking on a side hustle, freelancing, selling unused items online, or negotiating a raise at your current job. Even an extra $50 or $100 per month can significantly shorten your debt timeline and save you hundreds or even thousands in interest.

- Celebrate Milestones (Responsibly): Acknowledge and celebrate each debt you conquer. These small, non-financial rewards (a nice walk, a special home-cooked meal, an hour to read a book) reinforce positive behaviour and help maintain your emotional engagement with the process. Avoid celebratory splurges that could undermine your progress.

Final Thoughts: Snowball vs. Avalanche – The True Victory

So, which method truly saves more money? From a purely mathematical standpoint, the answer is clear and undeniable: the Debt Avalanche Method will always result in less interest paid and a faster debt payoff, assuming consistent adherence. If your sole objective is financial optimization and maximizing savings, the Avalanche is your champion.

However, the ultimate victory in the battle against debt isn’t just about saving the most money; it’s about achieving and sustaining momentum until you are completely debt-free. If you’ve historically struggled with financial discipline, or if the thought of a long, drawn-out process feels too daunting, the Debt Snowball Method might be the better fit for you. Its psychological benefits and rapid reinforcement can keep you motivated when the mathematical gains of the Avalanche might feel too slow.

The most crucial step is to take action. Choose a method that resonates with your personal motivation and financial personality, commit to it wholeheartedly, and stay disciplined. Whether you roll your way to freedom with a growing snowball or crush your interest payments with a powerful avalanche, the glorious end goal remains the same: a life unburdened by debt, offering true financial freedom and peace of mind. Your debt-free future awaits.