10 Common Credit Report Errors and How to Fix Them

Your credit report plays a critical role in your financial life. Whether you’re applying for a loan, credit card, mortgage, or even a job, lenders and institutions rely on your credit report to assess your credibility. However, credit reports are not always accurate. Errors can and do happen—and even a small mistake can significantly impact your credit score, leading to higher interest rates or denied applications.

Understanding the most common credit report errors and knowing how to fix them is essential for maintaining your financial health.

Why Credit Report Errors Happen

Credit report errors occur more often than many people realize. These mistakes can arise from multiple sources, including lenders, data entry systems, or even identity theft.

One of the main reasons is human error. Financial institutions report data to credit bureaus regularly, and incorrect entries—such as wrong account balances or payment statuses—can slip through. Additionally, outdated information may remain on your report longer than it should.

Another common cause is mixed files. This happens when your credit file is confused with someone else’s, often due to similar names or identification details. Identity theft is another major contributor, where fraudulent accounts or transactions appear on your report without your knowledge.

System glitches and delays in updates can also lead to inconsistencies. For example, a paid-off loan might still appear as active or overdue.

Types of Common Reporting Mistakes

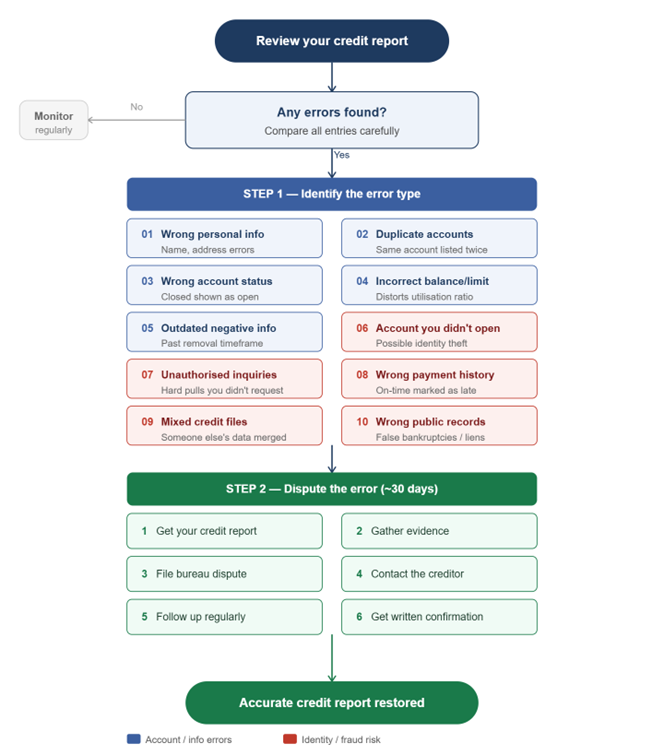

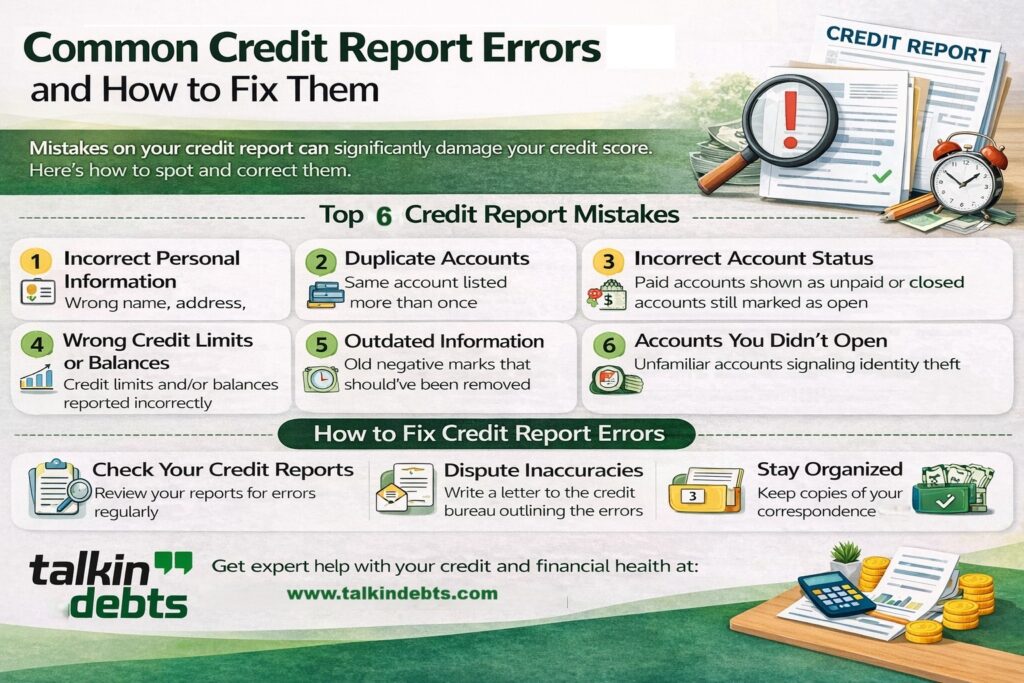

Credit report errors can take many forms, but most fall into a few key categories. Recognizing these can help you quickly identify issues in your report.

1. Incorrect Personal Information

This includes wrong name spellings, incorrect addresses, or mismatched contact details. While these may seem minor, they can sometimes indicate a deeper issue like a mixed credit file.

2. Duplicate Accounts

Sometimes the same account may appear multiple times, making it seem like you have more debt than you actually do.

3. Incorrect Account Status

An account that is closed might still be listed as open, or a paid loan could be marked as unpaid or delinquent.

4. Wrong Credit Limits or Balances

Your credit utilization ratio plays a major role in your score. If your balance or credit limit is reported incorrectly, it can distort your financial profile.

5. Outdated Information

Negative information, such as late payments or defaults, should be removed after a specific period. If they remain beyond that timeframe, it’s an error.

Identity-Related Errors

Identity-related issues are among the most serious types of credit report errors because they can indicate fraud.

6. Accounts You Didn’t Open

If you notice unfamiliar accounts on your report, it could be a sign of identity theft. Fraudsters may use your personal details to open credit lines.

7. Unauthorized Credit Inquiries

Hard inquiries occur when lenders check your credit. If you see inquiries from companies you never applied to, it may signal misuse of your identity.

8. Incorrect Payment History

Payments marked as late or missed—even when you paid on time—can damage your score significantly.

9. Mixed Credit Files

This occurs when your report includes someone else’s information. It’s more common than expected, especially with similar names or shared addresses.

10. Incorrect Public Records

Bankruptcies, liens, or court judgments may be incorrectly listed under your name or not removed after resolution.

Steps to Dispute Inaccurate Information

Fixing credit report errors requires a systematic approach. Acting quickly can minimize the damage and restore your credit standing.

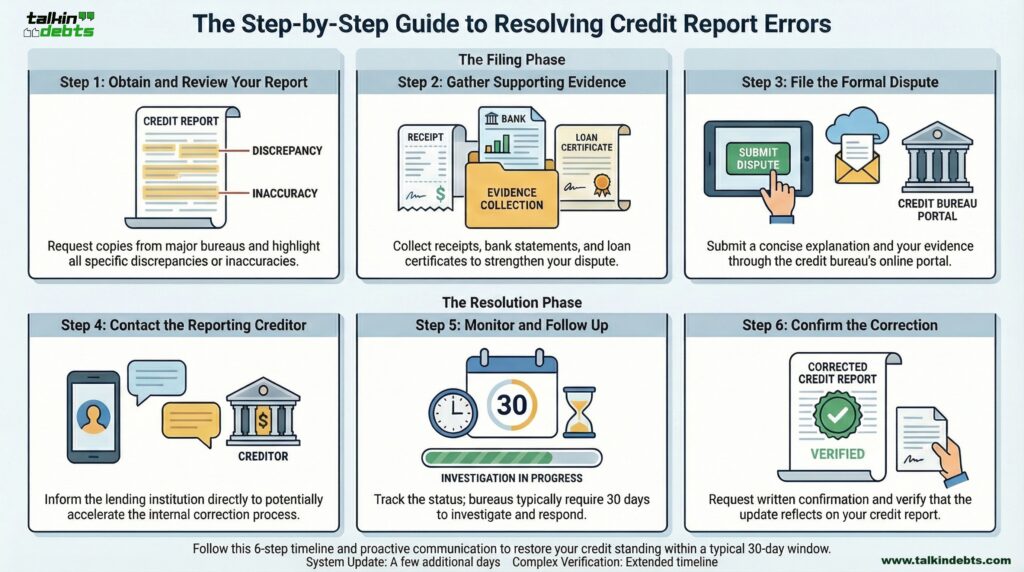

Step 1: Obtain Your Credit Report

Start by getting a copy of your credit report from the major credit bureaus. Review it carefully and highlight any discrepancies.

Step 2: Gather Supporting Documents

Collect evidence such as payment receipts, bank statements, loan closure certificates, or identity proof. Documentation strengthens your dispute.

Step 3: File a Dispute with the Credit Bureau

Most credit bureaus allow disputes online. Clearly explain the error and attach your supporting documents. Be specific and concise.

Step 4: Contact the Creditor

In addition to notifying the credit bureau, inform the lender or institution that reported the incorrect information. They may correct the issue faster internally.

Step 5: Follow Up Regularly

Track the status of your dispute. If the issue isn’t resolved within the expected timeframe, follow up with both the bureau and the creditor.

Step 6: Request Written Confirmation

Once the correction is made, ask for a written confirmation and ensure the update reflects in your credit report.

How Long Do Corrections Take

The time required to fix credit report errors can vary depending on the complexity of the issue.

In most cases, credit bureaus take 30 days to investigate and respond to a dispute. During this period, they verify the information with the reporting creditor.

If the creditor confirms the error, the correction is made, and your credit report is updated accordingly. In some cases, it may take an additional few days for the updated report to reflect across all systems.

However, if the dispute involves multiple accounts or requires extensive verification, the process may take longer. Delays can also occur if documentation is incomplete or unclear.

It’s important to stay proactive throughout the process. Regular follow-ups can help ensure your case doesn’t get overlooked.

Protecting Your Credit Moving Forward

Fixing errors is only part of the process—preventing them is equally important.

Regularly monitoring your credit report is the best way to catch issues early. Make it a habit to review your report at least once every few months. Many financial platforms offer free credit monitoring services that alert you to changes.

You should also safeguard your personal information. Avoid sharing sensitive details unless necessary and ensure that your financial accounts are secured with strong passwords and multi-factor authentication.

Another effective strategy is to maintain proper financial records. Keep copies of loan agreements, payment confirmations, and account statements. These documents can be invaluable if you ever need to dispute an error.

The Real Impact of Credit Report Errors

Credit report errors are not just minor inconveniences—they can have real financial consequences.

A lower credit score can lead to higher interest rates on loans and credit cards. In some cases, it may result in outright rejection of applications. For businesses and professionals, it can even affect partnerships or approvals for contracts.

Errors can also cause unnecessary stress and confusion, especially if they involve identity theft or large financial discrepancies.

That’s why it’s essential to treat your credit report as a living financial document that requires regular attention and maintenance.

Ensuring Long-Term Credit Accuracy

Credit report errors are more common than most people think, but they are also fixable. By understanding the types of errors, staying vigilant, and taking prompt action, you can protect your financial reputation and ensure your credit profile accurately reflects your true standing.

A clean and accurate credit report not only improves your financial opportunities but also strengthens your financial decision-making. Consistent monitoring, timely dispute resolution, and proper record-keeping will help you maintain long-term credit accuracy and avoid unnecessary financial setbacks.

Learn more about our Credit Counselling Guidance