Debt Counseling: What to Expect in Your First Session

Affiliate Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. Disclosure Policy

Debt can feel overwhelming. Whether you’re struggling with credit card balances, medical bills, personal loans, or collection calls, you’re probably searching for answers and a realistic way forward. If you’ve been looking for debt counseling near me, you’re already taking an important first step toward improving your financial situation.

Many people hesitate because they don’t know what to expect during the first appointment. The good news is that your first session is designed to help—not judge—you. A certified counselor will review your finances, explain your options, and help you understand the best path based on your unique circumstances.

In this guide, you’ll learn exactly what happens during a first debt counseling session, what documents to bring, the benefits of professional guidance, and how to prepare for a productive meeting.

See if CuraDebt is right for your situation by booking a free consultation.

What Is Debt Counseling?

Debt counseling is a professional service that helps individuals understand their financial situation and develop a strategy to manage or reduce debt. Instead of guessing which solution might work, you receive personalized guidance from experienced financial professionals.

People seek debt counseling services for many reasons, including mounting bills, missed payments, and difficulty keeping up with monthly expenses. A counselor reviews your finances, identifies problem areas, and recommends practical solutions that fit your circumstances.

Depending on your financial situation, they may discuss:

- Budgeting strategies

- Credit counseling

- Debt management plans

- Debt settlement

- Tax debt assistance

- Other debt relief options

The biggest benefit is having an experienced professional explain your choices clearly, allowing you to make informed decisions instead of reacting under financial pressure.

Why People Search for Debt Counseling Near Me

Financial problems rarely happen overnight. In many cases, debt builds slowly until monthly payments become difficult to manage.

People commonly search for debt counseling near me because they’re dealing with:

- High-interest credit card debt

- Medical expenses

- Personal loans

- Collection calls

- IRS or tax debt

- Reduced income

- Divorce or family changes

- Unexpected emergencies

- Poor budgeting habits

Many people simply want someone to explain their options before the situation gets worse.

Professional financial counseling provides clarity and confidence, helping you move from uncertainty to a realistic action plan.

Debt Counseling: What to Expect During Your First Session

Knowing what to expect from debt counseling can make the experience much less stressful. Your first meeting focuses on understanding your finances—not selling you a program.

Initial Financial Assessment

The counselor begins by learning about your financial background.

Expect questions about:

- Your employment

- Household income

- Family size

- Monthly expenses

- Financial goals

- Current financial challenges

This conversation helps the counselor understand your complete financial picture before recommending any solutions.

Reviewing Your Income and Expenses

Next, you’ll review where your money comes from and where it goes each month.

Your counselor may ask about:

- Salary

- Side income

- Rent or mortgage

- Utilities

- Groceries

- Insurance

- Transportation

- Childcare

- Entertainment expenses

Many people discover spending habits they hadn’t noticed before. This step often provides immediate insight into improving cash flow.

Evaluating Your Debts

This is one of the most important parts of the first debt counseling session.

Your counselor reviews each debt, including:

- Credit cards

- Medical bills

- Personal loans

- Student loans

- Collection accounts

- Tax obligations

They’ll examine:

- Total balances

- Interest rates

- Minimum payments

- Delinquency status

- Collection activity

This evaluation helps determine which debts need immediate attention.

Discussing Debt Relief Options

After reviewing your finances, your counselor explains possible solutions.

Depending on your situation, these may include:

- Budget restructuring

- Debt management plans

- Debt settlement

- Credit counseling

- Tax debt assistance

- Negotiation with creditors

- Other debt relief consultation recommendations

A good counselor explains the advantages and disadvantages of every option so you can make an informed decision.

Creating a Personalized Financial Plan

No two financial situations are exactly alike.

Instead of offering a one-size-fits-all solution, your counselor creates a customized action plan that may include:

- Monthly budgeting

- Debt repayment priorities

- Spending adjustments

- Savings goals

- Payment strategies

- Long-term financial planning

This roadmap helps you understand exactly what to do after leaving the session.

Answering Your Questions

Many people arrive feeling anxious or confused.

Your counselor will answer questions such as:

- Which debts should I pay first?

- Should I settle or repay?

- Will creditors continue calling?

- Can I improve my credit?

- How long will debt relief take?

- What happens if I can’t make payments?

This conversation is your opportunity to gain clarity without pressure.

Next Steps After the Session

Before the appointment ends, you’ll understand what comes next.

Possible next steps include:

- Reviewing your financial plan

- Gathering additional documents

- Speaking with creditors

- Enrolling in a debt relief program (if appropriate)

- Scheduling a follow-up meeting

Remember, attending a consultation doesn’t automatically commit you to any program.

Documents to Bring to Your First Appointment

Being prepared helps your counselor provide the most accurate recommendations.

Bring as many of the following documents as possible.

Pay Stubs

These verify your current income and help calculate your monthly cash flow.

Bank Statements

Recent statements show your spending habits, recurring expenses, and available funds.

Credit Card Statements

These provide balances, minimum payments, interest rates, and account status.

Loan Documents

Bring information about personal loans, auto loans, student loans, or other outstanding debt.

Tax Records

Tax documents are especially important if you’re dealing with IRS debt or tax-related financial issues.

Monthly Expense List

Include recurring expenses such as:

- Rent

- Mortgage

- Utilities

- Insurance

- Transportation

- Childcare

- Food

- Phone

- Internet

This allows your counselor to build a realistic budget.

Collection Notices

Bring letters from collection agencies or creditors so your counselor understands any urgent issues.

Get Your Free CuraDebt Consultation Today

You don’t have to figure everything out alone. Speaking with an experienced debt specialist can help you understand your options and reduce the uncertainty surrounding your finances.

Get your free CuraDebt consultation today to explore personalized debt relief solutions with no obligation. A simple conversation could help you take the first step toward regaining financial control.

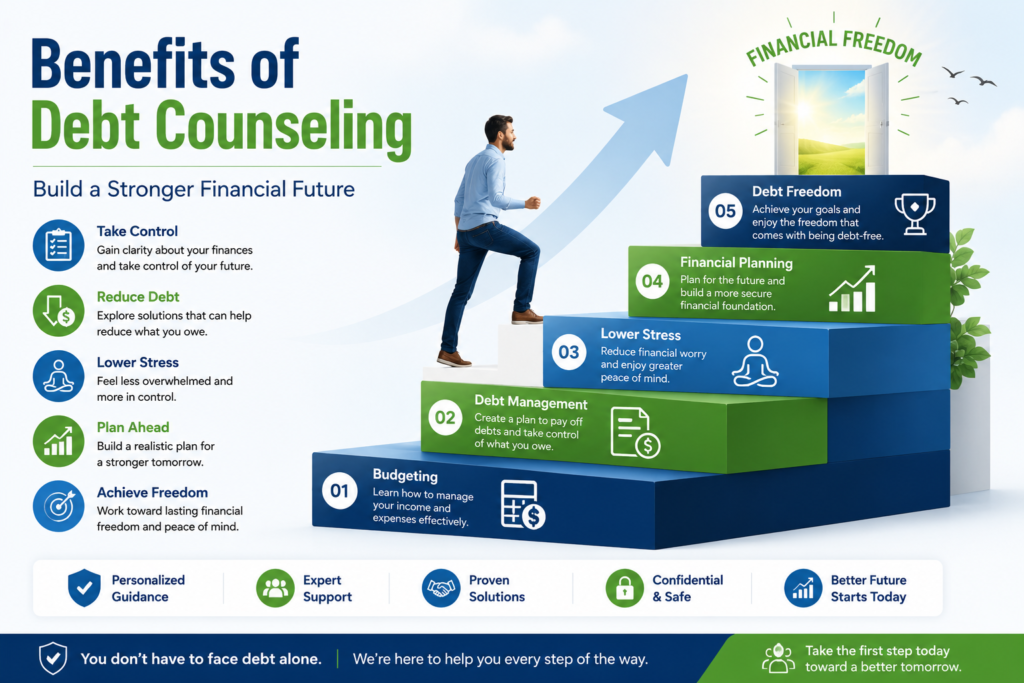

Benefits of Debt Counseling

Professional debt counseling services offer much more than budgeting advice.

Lower Financial Stress

Having a clear plan often reduces anxiety and helps you regain confidence.

Better Budgeting

You’ll learn practical ways to manage income and expenses more effectively.

Understanding Repayment Options

Many people don’t realize how many debt relief options may be available.

Professional Guidance

Experienced counselors understand creditor negotiations, repayment strategies, and financial planning.

Long-Term Financial Planning

The goal isn’t simply reducing debt—it’s helping you build healthier financial habits.

Greater Confidence

After learning debt counseling what to expect, many people feel empowered to make informed financial decisions.

Common Mistakes to Avoid Before Debt Counseling

Avoid these common mistakes to get the most from your consultation.

Ignoring Creditors

Ignoring phone calls or letters rarely makes debt disappear. Communicating early often creates more options.

Taking Out More Loans

Borrowing additional money usually increases financial pressure instead of solving it.

Hiding Financial Information

Be completely honest with your counselor. Accurate information leads to better recommendations.

Waiting Too Long

The earlier you seek debt help, the more solutions may be available.

Believing Debt Relief Scams

Be cautious of companies that promise guaranteed debt elimination or demand large upfront fees before providing assistance.

Choose reputable professionals with transparent processes and realistic expectations.

Take the First Step Toward Financial Freedom

Understanding what to expect from debt counseling can remove much of the uncertainty that keeps people from seeking help. Your first appointment is an opportunity to review your finances, understand your debt, explore available solutions, and receive personalized guidance from experienced professionals.

Whether you’re dealing with credit card balances, medical bills, personal loans, or tax debt, professional debt counseling services can help you create a practical path toward financial stability. The sooner you seek debt help, the more opportunities you may have to improve your financial future.

Start your free CuraDebt session today—there’s no obligation, and taking the first step now could put you on the path toward financial freedom.

Frequently Asked Questions

Is debt counseling free?

Many organizations offer a free initial debt relief consultation. Always ask about fees before enrolling in any program.

Does debt counseling affect my credit score?

Simply attending a counseling session does not directly affect your credit score. However, certain debt relief programs may have different credit implications, which your counselor should explain.

How long is the first session?

Most first debt counseling session appointments last between 45 and 90 minutes, depending on your financial situation.

Do I have to enroll in a program?

No. A consultation is designed to educate you about your options. You’re free to decide whether any recommended program is right for you.

Can debt counseling help with tax debt?

Yes. Some providers specialize in tax debt and may discuss settlement or payment options if you owe back taxes.

How should I prepare?

Gather your financial documents, create a list of monthly expenses, and be ready to discuss your financial goals honestly. The more information you provide, the more personalized the advice will be.