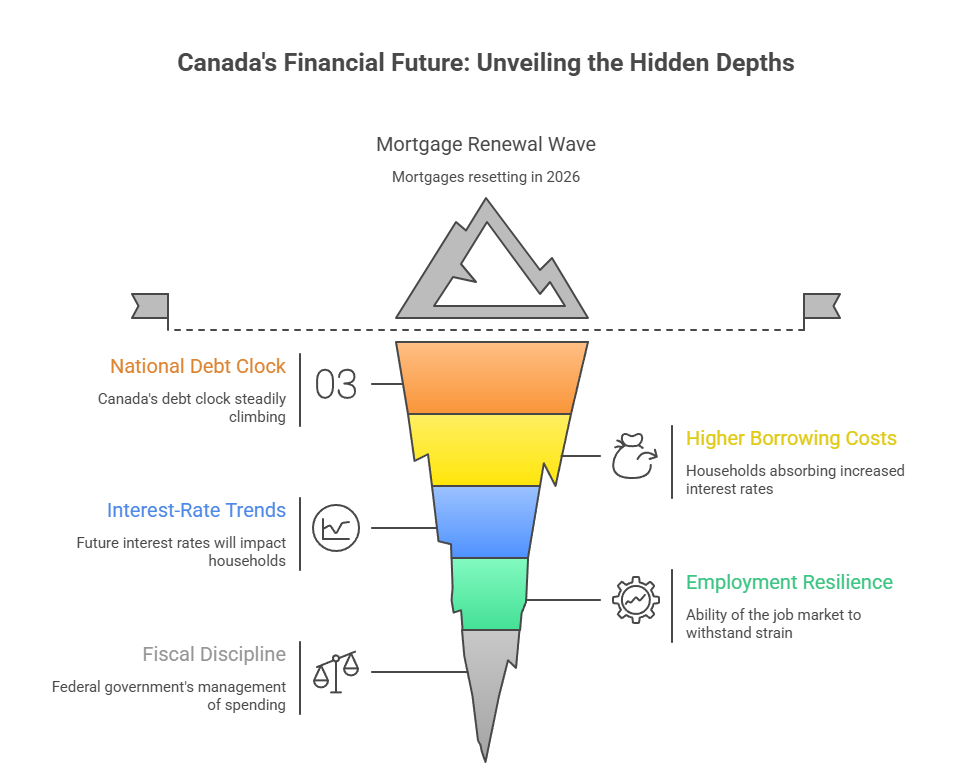

Canada’s National Debt Clock Accelerates as Mortgage Renewals Reset in 2026

Canada’s national debt clock is ticking faster in 2026, and economists warn the country may be approaching a financial pressure point. As millions of homeowners face mortgage renewals at significantly higher interest rates, the combined weight of government borrowing and household debt is drawing renewed scrutiny. The mortgage renewal crisis is no longer a distant risk—it is unfolding in real time, reshaping household budgets, consumer spending, and broader economic stability across Canada.

The latest data shows Canada’s national debt continuing to climb, even as policymakers attempt to balance growth and fiscal discipline. At the same time, the mortgage renewal wave expected throughout 2026 is poised to expose homeowners to payment shocks that many did not fully anticipate when they locked in ultra-low rates during the pandemic years. Together, these forces are creating what analysts describe as a “dual-pressure moment” for the Canadian economy.

Canada Debt Clock Shows Mounting Fiscal Pressure

The Canada debt clock has become an increasingly watched indicator among economists, investors, and policymakers. The federal government’s borrowing expanded sharply during the pandemic, and while deficits have narrowed from their peak, the total national debt remains historically elevated.

What makes the current situation more concerning is the timing. Government debt is rising just as households—already among the most indebted in the developed world—are preparing to refinance mortgages at much higher rates. This overlap amplifies systemic risk.

Financial analysts note three key trends driving the acceleration:

- Persistent federal deficits

- Higher interest costs on government borrowing

- Slower economic growth projections

Interest payments alone are consuming a growing share of federal revenues. As rates remain elevated compared with the ultra-low period of 2020–2021, servicing the national debt is becoming more expensive, limiting fiscal flexibility.

The 2026 Mortgage Renewal Wave Begins

The mortgage renewal crisis is rooted in decisions made during the pandemic housing boom. Millions of Canadian homeowners secured five-year fixed mortgages in 2020 and 2021 when interest rates were near historic lows. Those loans are now beginning to mature.

In 2026, a large cohort of borrowers will renew at rates that are often two to three percentage points higher than their original terms. For many households, this translates into hundreds—or even thousands—of dollars in additional monthly payments.

Mortgage industry estimates suggest:

- Roughly 40% of outstanding mortgages will renew between 2025 and 2027

- Many borrowers could see payment increases of 25% to 40%

- Highly leveraged households face the greatest risk

This reset is occurring gradually, but its cumulative impact is expected to intensify through 2026.

Payment Shock: The Household Reality

For Canadian families, the mortgage renewal crisis is not an abstract macroeconomic concept—it is a monthly budget shock. Homeowners who purchased at peak prices are especially vulnerable because they are carrying large principal balances.

Consider a typical scenario now emerging across the country. A homeowner who locked in a 2% mortgage rate in 2021 may now face renewal rates closer to 5% or higher. On a $500,000 mortgage, that shift can increase monthly payments by more than $700.

Households are responding in several ways:

- Cutting discretionary spending

- Extending amortization periods

- Increasing use of credit cards or lines of credit

- Delaying major purchases

Consumer spending patterns already show early signs of tightening in interest-sensitive sectors such as retail, home improvement, and automotive sales.

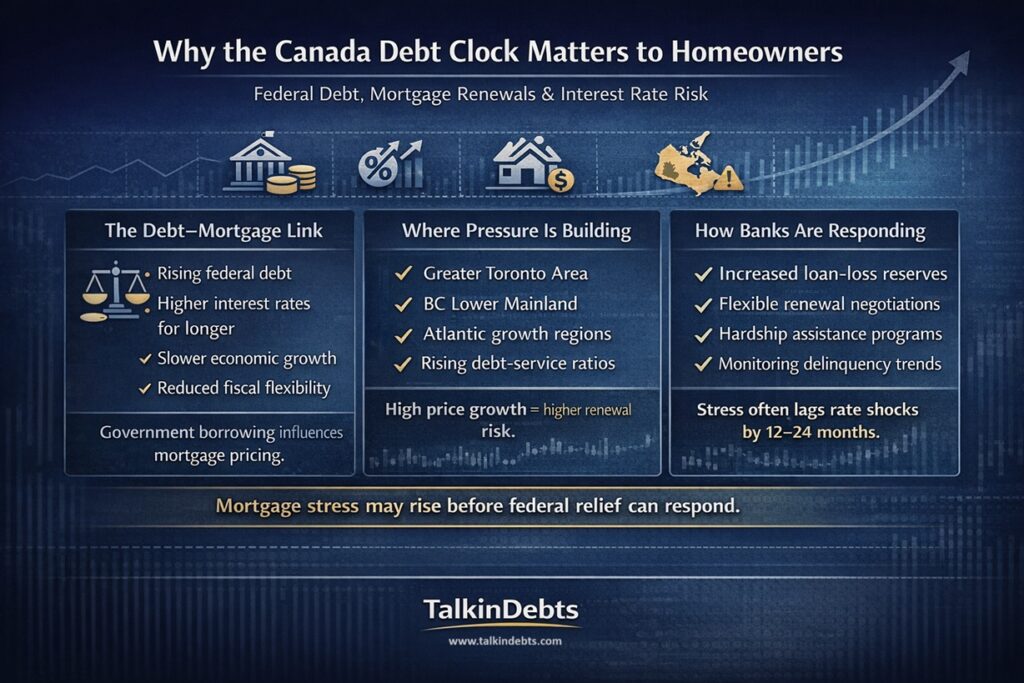

Why the Canada Debt Clock Matters to Homeowners

At first glance, federal debt and household mortgages may appear unrelated. However, economists stress that the Canada debt clock and the mortgage renewal crisis are deeply interconnected.

When government debt rises:

- Interest rates tend to remain higher for longer

- Fiscal room for stimulus shrinks

- Economic growth can slow

Higher interest rates directly affect mortgage pricing. If government borrowing continues to expand, it could complicate efforts to bring borrowing costs down quickly.

Moreover, rising federal interest payments may limit Ottawa’s ability to introduce large-scale relief measures if household stress intensifies.

Regional Hotspots Emerging

The mortgage renewal impact is not uniform across Canada. Housing markets that experienced the sharpest pandemic-era price increases are now seeing the greatest vulnerability.

Early risk indicators point to pressure building in:

- Ontario’s Greater Toronto Area

- British Columbia’s Lower Mainland

- Parts of Atlantic Canada with rapid recent price growth

In these regions, home prices rose significantly faster than incomes during the low-rate period. As mortgages reset, debt-service ratios are climbing more quickly than the national average.

Rural markets and provinces with lower average home prices may experience softer impacts, though no region is entirely insulated.

Lenders Preparing for Stress

Canadian banks and mortgage lenders have been closely monitoring the mortgage renewal cycle. Stress tests introduced in recent years require borrowers to qualify at higher benchmark rates, which provides some buffer.

However, industry observers note that the real test comes when households must actually make the higher payments month after month.

Financial institutions are preparing through:

- Increased loan-loss provisioning

- More flexible renewal negotiations

- Expanded hardship assistance programs

- Closer monitoring of delinquency trends

So far, mortgage arrears remain relatively low by historical standards. But economists caution that delinquencies often lag rate shocks by 12 to 24 months.

Consumer Spending Faces Headwinds

One of the clearest economic ripple effects of the mortgage renewal crisis is expected to appear in consumer spending. Housing costs represent the largest expense for most Canadian households. When mortgage payments rise sharply, discretionary spending typically falls.

Retail analysts are already watching for:

- Slower growth in discretionary retail

- Reduced home renovation activity

- Softer vehicle sales

- Increased household saving rates out of caution

If the Canada debt clock continues climbing while consumer demand weakens, economic growth could face a delicate balancing act through 2026.

Policymakers Walk a Tightrope

Federal and central bank officials are navigating a complex policy environment. On one hand, inflation pressures have moderated compared with their peak. On the other hand, cutting rates too quickly could reignite housing market overheating.

The Bank of Canada must weigh:

- Inflation stability

- Household debt vulnerability

- Housing market risks

- Broader economic growth

Meanwhile, federal fiscal policy is constrained by the rising cost of servicing the national debt. Large stimulus programs similar to pandemic-era support are considered unlikely unless economic conditions deteriorate sharply.

Housing Market Adjustments Underway

Canada’s housing market has already cooled from its pandemic highs, but the mortgage renewal cycle could shape the next phase of price movement.

Analysts expect a mixed pattern:

- Some homeowners may list properties due to payment strain

- Others may hold and cut spending elsewhere

- New buyers remain sensitive to interest-rate expectations

A wave of forced selling is not currently the base-case forecast. However, even modest increases in listings could influence price momentum in highly leveraged markets.

The key variable remains employment. As long as job markets remain relatively stable, most homeowners are expected to manage higher payments—though often with reduced financial flexibility.

The Psychological Impact of the Debt Clock

Beyond the raw numbers, the Canada debt clock carries psychological weight. Highly visible debt metrics can influence consumer and investor sentiment.

When households see both government debt and personal borrowing costs rising simultaneously, confidence can weaken. This behavioral effect can sometimes amplify economic slowdowns even before hard data shows significant deterioration.

Business investment decisions, hiring plans, and consumer purchases are all sensitive to confidence levels. Economists are watching sentiment indicators closely as the mortgage renewal cycle accelerates.

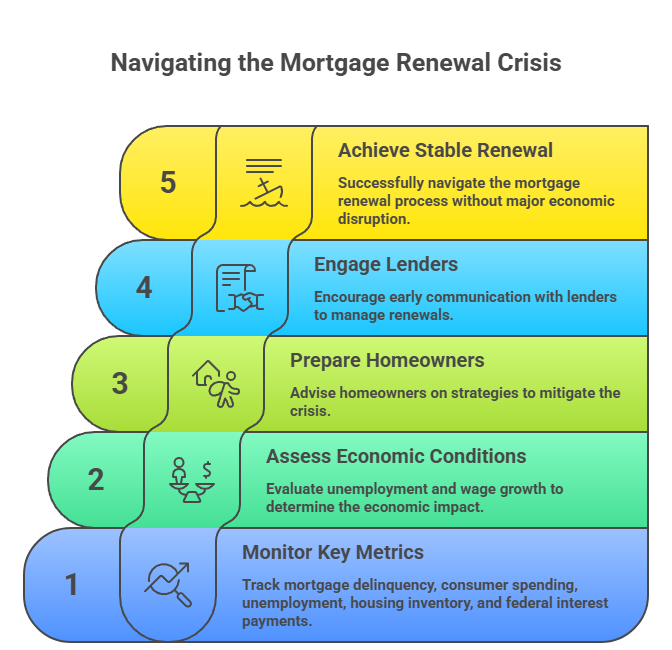

What Experts Are Watching in 2026

As the year unfolds, financial analysts say several indicators will determine whether the mortgage renewal crisis becomes a manageable adjustment or a more serious economic drag.

Key metrics include:

- Mortgage delinquency rates

- Consumer spending trends

- Unemployment levels

- Housing inventory growth

- Federal interest-payment share of revenues

If unemployment remains low and wage growth holds steady, Canada may navigate the transition without major disruption. However, any negative shock—such as job losses or global economic slowdown—could magnify household stress.

Strategic Moves for Homeowners

Financial planners say preparation is critical for borrowers approaching renewal in 2026. Many households still have time to soften the impact.

Common strategies being recommended include:

- Making pre-payments where possible

- Reducing other high-interest debt

- Building emergency savings

- Shopping with multiple lenders before renewal

- Considering longer amortization options

Early engagement with lenders is increasingly encouraged, especially for highly leveraged borrowers.

A Defining Financial Moment

Canada’s national debt clock and the 2026 mortgage renewal wave are converging at a pivotal moment for the country’s financial outlook. While the situation does not currently point to a systemic crisis, the margin for error is narrower than in previous years.

The coming quarters will reveal whether households can absorb higher borrowing costs without triggering broader economic strain. Much will depend on interest-rate trends, employment resilience, and fiscal discipline at the federal level.

What is clear is that the era of ultra-cheap borrowing has ended. As mortgages reset and the Canada debt clock continues its steady climb, 2026 is shaping up to be a defining year for Canada’s debt landscape—one that policymakers, lenders, and households alike will be watching with increasing urgency.