Crushed by Debt: Nearly 500,000 Americans to Lose Social Security Income Over Student Loan Defaults

A New Crisis Unfolds as the Government Targets the Nation’s Most Vulnerable for Loan Recovery

USA | May 2025 — In a move that is drawing fierce criticism from economists, advocacy groups, and everyday Americans alike, the U.S. government is preparing to withhold Social Security benefits from nearly half a million individuals starting this June, all because of defaulted student loan debt.

For many seniors and disabled citizens, this marks a devastating escalation in America’s growing debt enforcement crisis—one that threatens to undermine the very foundation of retirement security.

Debt That Follows You into Retirement

Student loan debt in the United States has reached staggering levels, with over $1.7 trillion still outstanding. But what has shocked many is that the burden is no longer just on young professionals or middle-aged borrowers.

Due to decades-old education loans—some dating back to the 1970s and 1980s—an estimated 490,000 retirees and disabled Americans could see part of their Social Security checks garnished or delayed by the U.S. Department of Education.

By law, the federal government can seize up to 15% of a borrower’s monthly Social Security benefit once a loan enters default. For individuals living on fixed incomes, this could mean losing essential funds needed for groceries, rent, medicine, or utilities.

Who Is Being Affected?

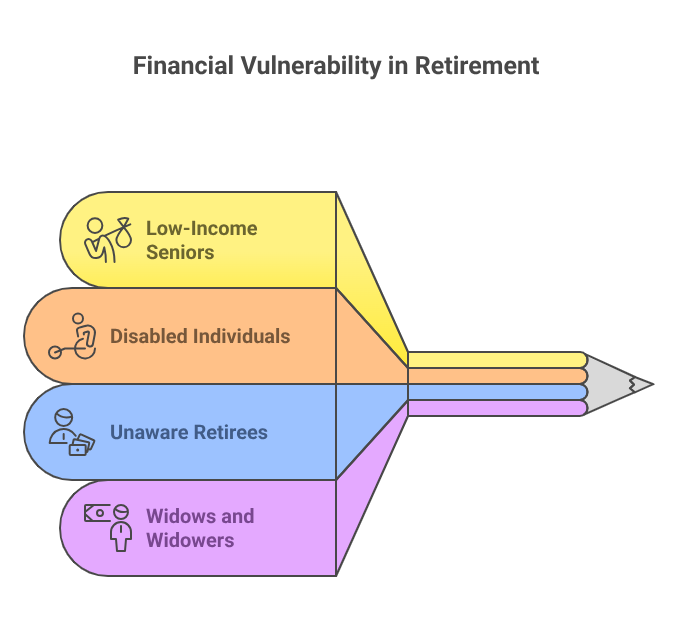

The profile of those impacted reads like a list of society’s most vulnerable:

- Low-income seniors, many of whom are already living below the poverty line

- Disabled individuals who can no longer work

- Retirees are unaware that interest has ballooned on their old student loans

- Widows and widowers who co-signed loans or borrowed for their children’s education

Some beneficiaries are seeing entire monthly checks reduced by hundreds of dollars, while others face the total confiscation of expected payments.

“This is not just about debt—this is about dignity,” said Angela Morris, director of the Elder Finance Protection League. “People who paid into Social Security for 40 or 50 years are now being punished for decades-old loans they often thought were long gone.”

A Legal but Controversial Practice

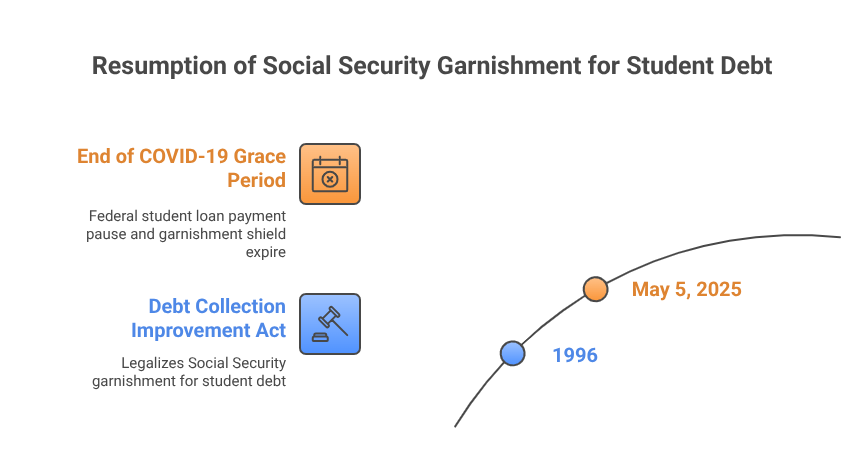

Though perfectly legal under the Debt Collection Improvement Act of 1996, the garnishment of Social Security checks for student debt has rarely been enforced on this scale—until now.

The pause on federal student loan payments during the COVID-19 pandemic shielded many from garnishments temporarily, but that protection ended on May 5, 2025, after a one-year grace period. Now, the full force of debt recovery is returning, and many say the timing couldn’t be worse.

“Food, rent, medicine—everything’s gone up. Now they’re taking what little we have left,” said 68-year-old John Ramirez, a retired warehouse worker from Texas.

Public Outrage and Political Fallout

Across the country, backlash is brewing. Hashtags like #DebtIsNotADeathSentence and #ProtectOurSeniors are trending as more stories emerge of retirees blindsided by garnishment letters and reduced bank deposits.

Lawmakers on both sides of the aisle are demanding answers. Several members of Congress are now drafting emergency legislation to protect Social Security recipients from future collections tied to federal student loan defaults.

“Social Security was never meant to be a tool for debt collectors,” said Senator Carla Jensen (D-OR). “This is a policy failure with real human consequences.”

What Can Affected Individuals Do?

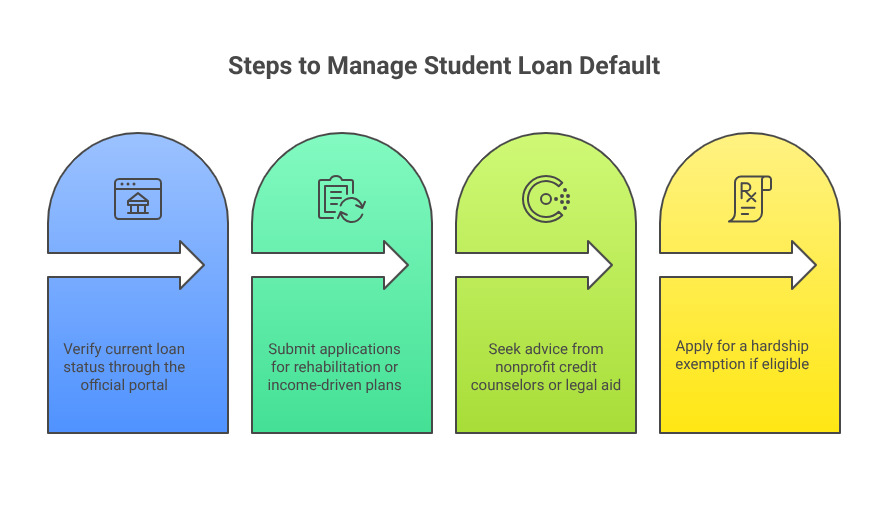

Financial experts recommend that individuals who may be affected take the following steps immediately:

- Check your loan status through the official Federal Student Aid portal

- Apply for loan rehabilitation or income-driven repayment plans to get out of default and stop garnishment

- Consult nonprofit credit counsellors or legal aid organizations for advice on next steps

- Request a hardship exemption if eligible

The Education Department has said it will issue notices before garnishments begin, but many worry those letters will come too late to act.

The Bigger Picture

This development sheds light on a larger, disturbing reality: student debt has become a lifelong burden, and now it’s following Americans into retirement. With more than 3 million borrowers over the age of 60 still carrying student loans, this could be just the beginning.

Unless meaningful reform is passed, the American promise of retirement—a time of rest and financial security—may be eroded by a debt system that punishes the poor and the elderly for past education.

The Fight Ahead

As June approaches, advocacy groups, senior organizations, and voters are uniting to demand urgent action. The message is clear:

“Debt shouldn’t define your future, and it should never steal your retirement.”