Global Debt Outlook 2025: IMF Warns of Rising Consumer Strain

New IMF signals show tightening financial conditions, rising household liabilities, and a shifting global debt landscape

Global debt is entering a new phase in 2025, and the International Monetary Fund (IMF) has raised a clear warning: consumer strain is intensifying across advanced, emerging, and developing economies alike. After years of volatile interest rates, inflation cycles, and uneven recovery from the pandemic-era shocks, the world is now witnessing debt levels that could redefine economic priorities for the next decade.

The IMF’s latest global debt assessment shows that both public and private debt ratios remain elevated, despite modest improvements in fiscal balances in some regions. However, the most concerning trend is the growing burden of household debt, which is beginning to affect consumption, savings, creditworthiness, and financial stability at the individual level.

This news report breaks down the IMF’s findings, explains the structural challenges, and highlights how individuals can prepare for the next financial cycle as the world economy transitions into tighter credit conditions.

A World Nearing Record Debt Levels Once Again

The IMF estimates that global debt now stands near USD 315 trillion, driven by government spending on social programs, interest costs, and persistent inflationary pressures. Although this is slightly lower than the pandemic-era peak, the composition of debt has changed in a way that directly impacts consumers.

Three major shifts stand out:

1. Government debt remains stubbornly high

Countries across North America, Europe, and Asia continue to carry large fiscal deficits. Higher rates have increased interest payments, which are now consuming 10–20% of government budgets in some advanced economies. This limits the capacity for social support programs, subsidies, and welfare initiatives that consumers rely on.

2. Private-sector debt is rising faster than GDP

Corporations are borrowing to refinance older debt, adjust to higher operational costs, and invest in digital transformation. Although this can stimulate innovation, it also increases the risk of layoffs if cash flows tighten.

3. Household debt is climbing at the fastest pace since 2008

Mortgages, personal loans, credit cards, and buy-now-pay-later (BNPL) schemes are expanding rapidly. Consumers in emerging markets, especially those with variable interest-rate loans, are showing early signs of repayment stress.

Interest Rates Are the Central Pressure Point

Global central banks have entered a cautious phase. While inflation is cooling, it is still above target in several countries. As a result, interest rates remain higher for longer, which amplifies debt servicing costs across all sectors.

For consumers, this means:

- Mortgage payments are significantly higher due to rate resets

- Auto and personal loan EMIs have increased

- Credit card APRs remain near historic highs

- Access to new credit is tighter

The IMF warns that households with income volatility are the most vulnerable, especially in markets where wage growth has not kept pace with inflation. Even small increases in interest costs can cascade into defaults, lower credit scores, and reduced household spending.

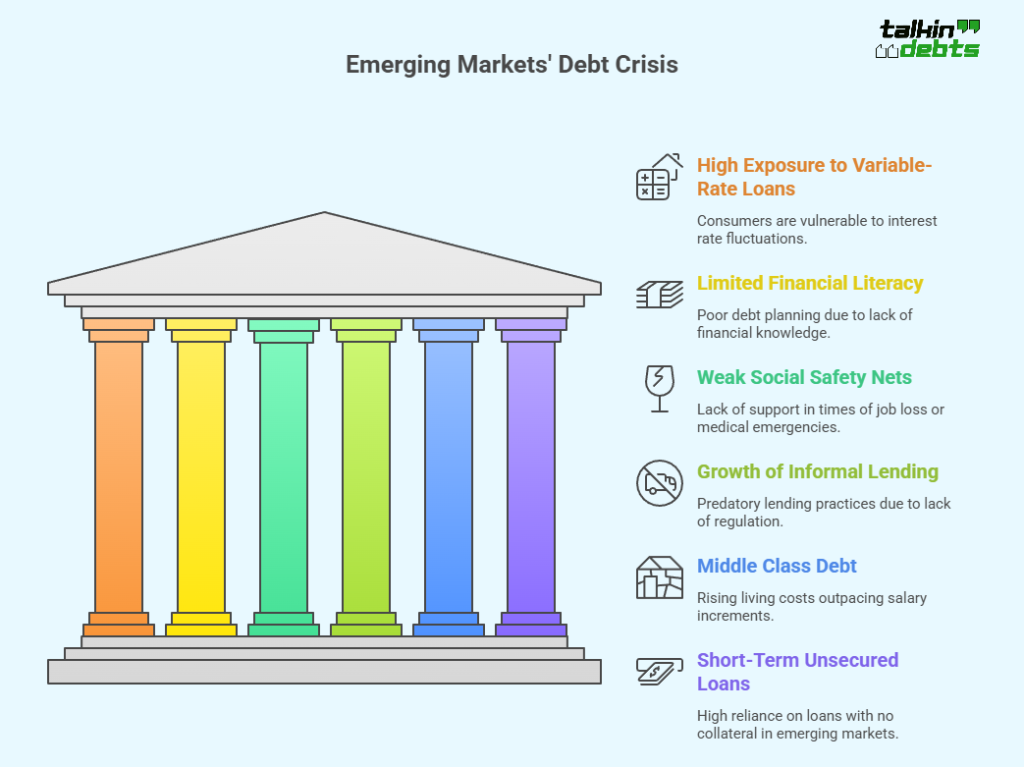

Emerging Markets: The Silent Epicenter of Debt Stress

While advanced economies face their own challenges, emerging markets are experiencing a sharper strain. Rapid urbanization, rising consumer aspirations, and easy access to digital credit platforms have fueled debt growth among younger populations.

Key concerns include:

- High exposure to variable-rate loans makes consumers sensitive to interest hikes

- Limited financial literacy, leading to poor debt planning

- Weak social safety nets, meaning any job loss or medical emergency could trigger financial collapse

- Growth of informal lending, which lacks regulation and often carries predatory rates

Countries in South Asia, Africa, and parts of Latin America are witnessing double-digit increases in household borrowing. Without adequate regulation, this can lead to long-term financial instability.

The Middle Class Is Feeling the Squeeze

Across the globe, middle-income households have become the most heavily indebted demographic. Rising living costs—housing, healthcare, food, and utilities—have outpaced salary increments.

The IMF notes that middle-class debt has increased due to:

- Higher reliance on consumer credit

- Growing cost of homeownership

- Reduced savings during the pandemic

- Lack of emergency funds

- Expansion of BNPL platforms that encourage impulse spending

In high-income economies, mortgage rates are the leading source of stress, while in emerging markets, short-term unsecured loans are the main contributor.

Weak Productivity Growth May Extend the Pain

Another challenge highlighted by the IMF is sluggish productivity growth, which limits wage improvements and economic expansion. When GDP grows slowly, debt ratios rise, placing more pressure on governments and households.

Low productivity also creates a loop:

- Slower wage growth →

- Higher dependency on credit →

- Increased debt levels →

- Lower ability to repay →

- Reduced consumer spending →

- Slower economic growth

This cycle, if unchecked, may keep consumers in a prolonged period of financial pressure.

Global Markets Brace for Potential Debt Shocks

Financial institutions and rating agencies have already begun tightening borrower assessments. Default rates in credit cards, auto loans, and small business loans have increased in several countries, signaling early stress.

Possible 2025 risk events include:

- Corporate debt defaults due to high refinancing costs

- Housing market corrections, particularly in overheated cities

- Sovereign downgrades for countries with large deficits

- Volatility in bond markets, especially emerging market debt

The IMF stresses that although the global system is more resilient than in 2008, the interconnectedness of economies means localized debt crises can spread quickly.

How Individuals Can Prepare for the Next Financial Cycle

The IMF emphasizes that preparedness at the household level is critical. Consumers who take proactive steps today will be better positioned to withstand future shocks.

Here are the IMF-recommended strategies, adapted for practical use:

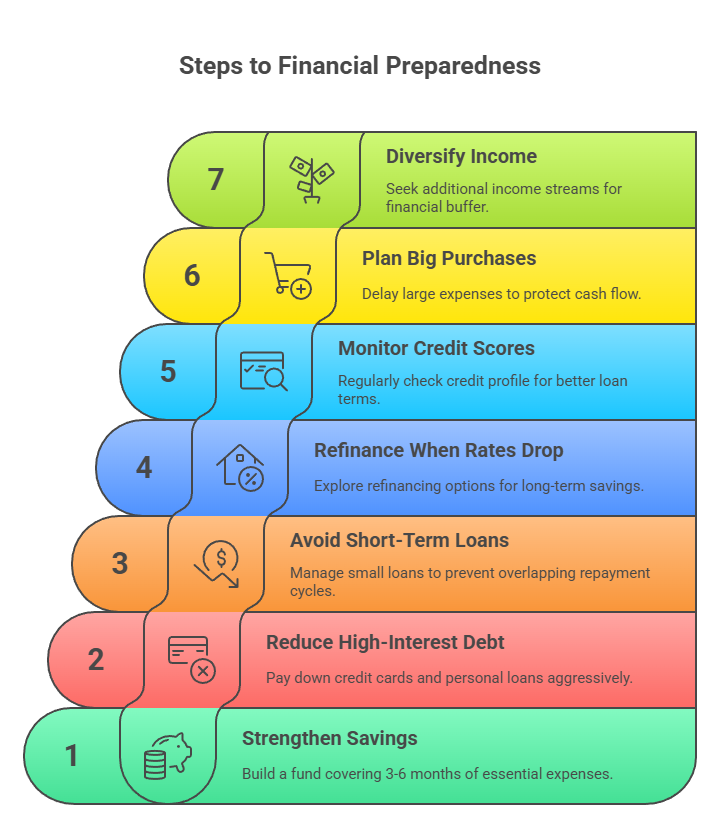

1. Strengthen Emergency Savings

Consumers should aim to build a fund covering 3–6 months of essential expenses. Even small, consistent contributions can accumulate over time and help prevent reliance on expensive short-term credit.

2. Reduce High-Interest Debt First

Credit cards and personal loans often carry interest rates that compound quickly. Paying these down aggressively can significantly ease monthly financial pressure.

3. Avoid Multiple Short-Term Loans

BNPL, microloans, and digital credit schemes appear convenient but can create overlapping repayment cycles. Managing too many small loans increases the risk of default.

4. Refinance When Rates Drop

When central banks begin reducing interest rates, consumers should explore refinancing options for mortgages, auto loans, and personal loans. A modest rate reduction can translate into substantial long-term savings.

5. Monitor Credit Scores Regularly

A strong credit profile ensures better loan terms and protects consumers from predatory lenders. Regular monitoring helps detect incorrect entries, fraud, or identity theft.

6. Plan Big Purchases Carefully

In periods of economic uncertainty, delaying large expenses such as home renovation, luxury items, or unnecessary electronics can protect cash flow.

7. Diversify Income Streams

Gig work, freelance opportunities, and small online businesses can provide supplemental income, offering a buffer during job loss or salary reductions.

Governments Also Need to Rethink Debt Strategy

While individual responsibility is crucial, the IMF stresses that governments must also take decisive actions to stabilize long-term debt trends.

Policy recommendations include:

- Strengthening debt sustainability frameworks

- Enhancing financial literacy programs

- Regulating digital lenders and BNPL platforms

- Improving consumer protection laws

- Redirecting spending to productivity-enhancing sectors

- Encouraging innovation and job creation

By reducing fiscal vulnerabilities and boosting economic competitiveness, countries can create a more stable environment for consumers and businesses.

A Turning Point for Global Finance

As 2025 unfolds, the global economy finds itself at a crossroads. Debt is no longer just a macroeconomic concept confined to governments and banks—it is a household-level concern shaping everyday financial decisions. From rising EMIs to shrinking disposable income, consumers worldwide are navigating a more complex financial landscape.

The IMF’s warning is clear: unless governments and households adapt swiftly, the pressure of rising debt could limit economic opportunity, increase inequality, and challenge financial resilience in the years ahead.

Yet, the outlook is not entirely negative. Technological innovation, stronger financial regulation, and gradual monetary easing could ease the burden in the medium term. Consumer discipline, combined with informed financial planning, will play a critical role in shaping outcomes.

The next financial cycle is beginning—and the choices made today will determine whether households emerge stronger or more vulnerable in the years to come.