New Debt Collection Laws in the US and UK Take Effect in 2026

CFPB Debt Rules and Tougher Regulations Transform Consumer Protection

Sweeping new debt collection laws across the United States and the United Kingdom are now in effect in 2026, bringing stricter oversight, tighter compliance requirements, and stronger consumer protections that are reshaping how debt collectors operate.

Regulators say the updated framework is designed to eliminate harassment, improve transparency, and hold collection agencies accountable for unethical practices that have triggered rising complaints in recent years. The changes, led by the Consumer Financial Protection Bureau’s CFPB debt rules in the US and reinforced by enhanced enforcement standards in the UK, represent the most significant overhaul of debt collection regulations in more than a decade.

For millions of borrowers, the reforms promise fewer intrusive calls and clearer repayment communication. For collection agencies, lenders, and creditors, the new rules introduce higher operational costs, deeper scrutiny, and stricter penalties for non-compliance.

Industry experts describe 2026 as a defining year that could permanently change the way debt recovery is conducted on both sides of the Atlantic.

Rising Consumer Debt Sparks Regulatory Action

The introduction of new debt collection laws comes at a time when household debt has climbed sharply. Higher interest rates, inflationary pressure, and post-pandemic financial strain have left many families struggling to meet loan, credit card, and utility payments.

As delinquencies increased, complaints about aggressive collection tactics also grew.

Regulators reported thousands of grievances involving repeated phone calls, unclear balances, threats of legal action, and attempts to collect outdated or inaccurate debts. Consumers frequently described feeling pressured into payments they could not realistically afford.

Authorities concluded that existing frameworks no longer reflected modern communication methods such as texting, emails, and automated dialers. The traditional rules were written for landline calls and paper letters, leaving gaps that some agencies exploited.

The 2026 reforms aim to close those gaps and modernize enforcement.

CFPB Debt Rules & UK Reforms:

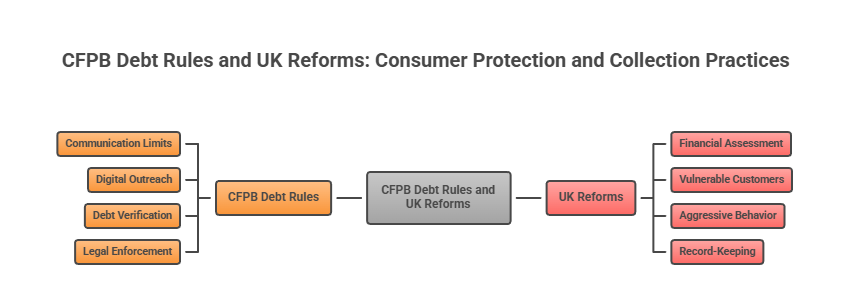

CFPB Debt Rules Redefine Collection Practices in the US

In the United States, the CFPB debt rules introduce tighter restrictions on how collectors contact consumers and pursue unpaid accounts.

One of the most impactful changes involves communication limits. Excessive calling is now subject to strict caps, and repeated or continuous attempts to reach a consumer may be treated as harassment. Collectors must carefully track how often they make contact to avoid violations.

Digital outreach is also regulated more heavily. Text messages, emails, and social media communication fall under the same legal standards as phone calls. Every digital message must provide a clear and simple opt-out option, allowing consumers to stop contact immediately if they choose.

Debt verification requirements have also expanded. Shortly after the first interaction, agencies must provide detailed information, including the original creditor’s name, total balance owed, itemized fees or interest, and instructions for disputing inaccuracies. This ensures borrowers fully understand what they are being asked to pay.

Legal enforcement has strengthened as well. Attempting to collect on time-barred debts or using misleading language about lawsuits can now trigger significant penalties. Regulators have emphasized that deceptive practices will face swift action.

For agencies, this means that documentation, call monitoring, and compliance systems are no longer optional — they are essential.

UK Tightens Oversight and Consumer Safeguards

The United Kingdom has introduced parallel reforms focused heavily on fairness and affordability.

Debt collectors are now expected to assess a borrower’s financial situation before proposing repayment plans. Pressuring consumers into unrealistic instalments is considered irresponsible and may violate conduct standards.

Agencies must also identify vulnerable customers, including those facing unemployment, illness, or financial hardship. In such cases, collectors are required to provide flexibility, offer breathing space, or temporarily pause recovery efforts.

Aggressive behavior is explicitly prohibited. Repeated automated dialers, threatening statements, or misleading claims about legal consequences can lead to enforcement action.

Record-keeping requirements have also become stricter. Firms must maintain detailed logs of every interaction, ensuring regulators can review how each case was handled. These audit trails are designed to increase transparency and accountability.

Regulators say the focus is clear: recovery should be fair, not intimidating.

Compliance Pressure Mounts for Collection Agencies

While the new debt collection laws aim to protect consumers, they also create operational challenges for the industry.

Collection agencies must now invest heavily in compliance technology. Systems are required to monitor call frequency, track opt-out requests, log communications, and store documentation securely.

Manual processes that once worked are no longer sufficient. Automated compliance tools, training programs, and internal audits are becoming standard requirements.

Smaller agencies may struggle with the cost of these upgrades, leading to concerns about consolidation within the sector. Some analysts predict that firms unable to meet regulatory expectations could exit the market or merge with larger competitors.

However, established players argue that stricter standards will ultimately benefit ethical companies by eliminating unfair competition from non-compliant operators.

Creditors Face Greater Responsibility

The impact of the new CFPB debt rules and UK regulations extends beyond collection agencies themselves. Banks, telecom providers, healthcare institutions, and utility companies that outsource debt recovery are also under scrutiny.

Creditors are increasingly responsible for ensuring their third-party partners follow all regulatory requirements. If a contracted agency violates the law, the creditor’s reputation and legal standing could be affected.

As a result, many businesses are strengthening vendor oversight, revising contracts, and demanding higher compliance standards before assigning accounts.

Some organizations are also shifting strategy by focusing more on early intervention. Offering hardship programs or flexible payment arrangements before accounts reach collections may reduce risks and improve customer relationships.

Preventive measures are becoming just as important as recovery tactics.

Consumers Gain Stronger Rights and Protections

For borrowers, the reforms provide meaningful safeguards.

Consumers now have greater control over how and when they are contacted. They can request limits on communication or stop certain channels entirely. They also receive clearer explanations of their debts, reducing confusion and disputes.

Stronger validation requirements make it easier to identify errors, outdated balances, or fraudulent claims. Meanwhile, restrictions on harassment and aggressive behavior help reduce stress during already difficult financial situations.

Advocates say these protections will improve trust between consumers and financial institutions.

Instead of fear-based collection, the industry is moving toward structured, respectful engagement.

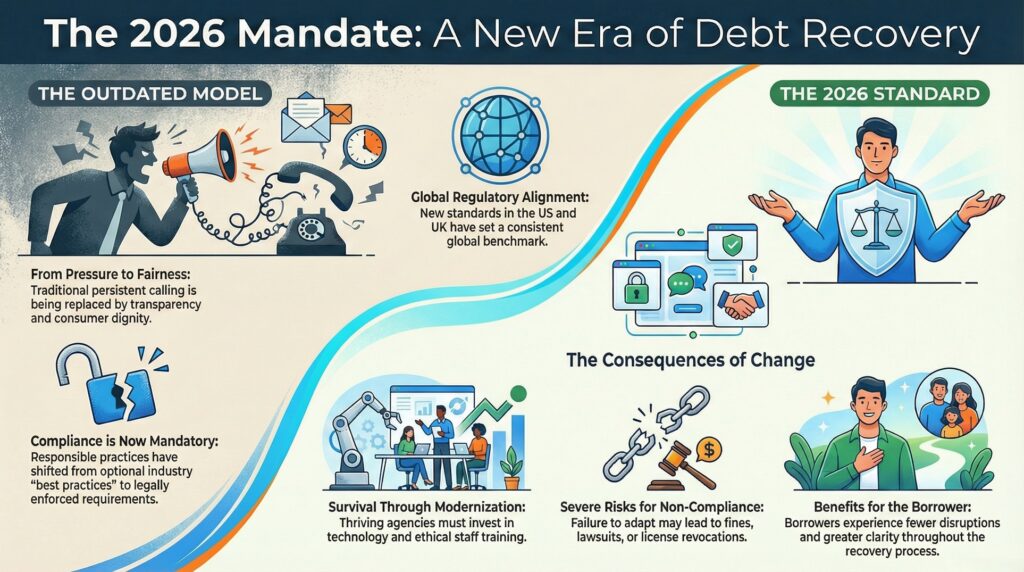

A Fundamental Shift for the Industry

The introduction of new debt collection laws in 2026 signals more than a routine policy update. It represents a fundamental transformation in how debt recovery is expected to function.

The traditional model of persistent calling and pressure tactics is giving way to a compliance-driven approach built on transparency and fairness. Regulators have made it clear that consumer dignity must come first.

Agencies that adapt by investing in technology, training staff, and prioritizing ethical practices are likely to thrive. Those who cling to outdated methods may face fines, lawsuits, or license revocations.

As enforcement activity increases throughout the year, the message from regulators remains consistent: responsible collection practices are no longer optional — they are mandatory.

The CFPB debt rules in the United States and the strengthened regulations in the United Kingdom have set a new global benchmark. Debt recovery is entering a more accountable era, one where consumer protection stands at the center of every interaction.

For borrowers, that means fewer disruptions and greater clarity. For the industry, it means higher standards and lasting change.

And for 2026, it marks the beginning of a new chapter in the future of debt collection.