US Debt Clock Hits $35 Trillion: What It Means for Your Wallet in 2025

In 2025, the US Debt Clock officially crossed the $35 trillion mark, a staggering milestone that has sparked concern among economists, policymakers, and everyday Americans. While national debt figures often seem abstract, the truth is this: the debt crisis has very real consequences for your wallet, your savings, and the future of the US economy.

The US National Debt Clock is more than just a running tally—it’s a reflection of how government borrowing, spending, and interest obligations shape inflation, taxes, and even household debt. If you’re wondering what $35 trillion in debt means for you in 2025, here’s the breakdown.

Understanding the US Debt Clock

The US Debt Clock is a constantly updated digital display in New York City and online, showing the national debt in real time. As of 2025, it has surged past $35 trillion, fuelled by decades of deficit spending, stimulus programs, entitlement obligations, and rising interest costs.

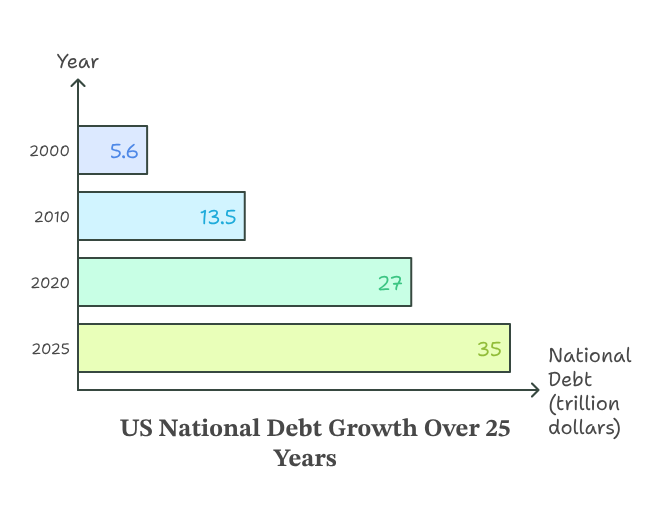

For context:

- In 2000, the national debt was $5.6 trillion.

- By 2010, it reached $13.5 trillion after the financial crisis.

- In 2020, debt ballooned to $27 trillion following COVID-19 relief packages.

- Today, in 2025, the US national debt has grown by more than 500% in 25 years.

This relentless rise raises critical questions: How will it be paid back? And what does it mean for average Americans?

Why $35 Trillion Matters

A figure as enormous as $35 trillion can feel distant, but the effects of this record-breaking debt level ripple through the economy and into household budgets. Here’s why it matters in 2025:

- Higher Inflation Pressure

Government borrowing at this scale often fuels inflation. While inflation cooled slightly from the 2022–2023 highs, persistent deficit spending risks keeping prices elevated. From groceries to housing, Americans continue to feel the pinch. - Rising Interest Rates

The Federal Reserve has kept interest rates higher to control inflation, and servicing a $35 trillion debt now consumes more than $1 trillion per year in interest payments alone. These higher rates spill over into mortgages, auto loans, and credit cards, making debt more expensive for households. - Future Taxes or Spending Cuts

With debt at record levels, future governments may be forced to raise taxes or cut back on social programs, healthcare, or retirement benefits. That means the cost of today’s borrowing could land squarely on taxpayers in the coming decades.

The Impact on Your Wallet

Now, let’s translate the US national debt crisis into real-life consequences for 2025 households.

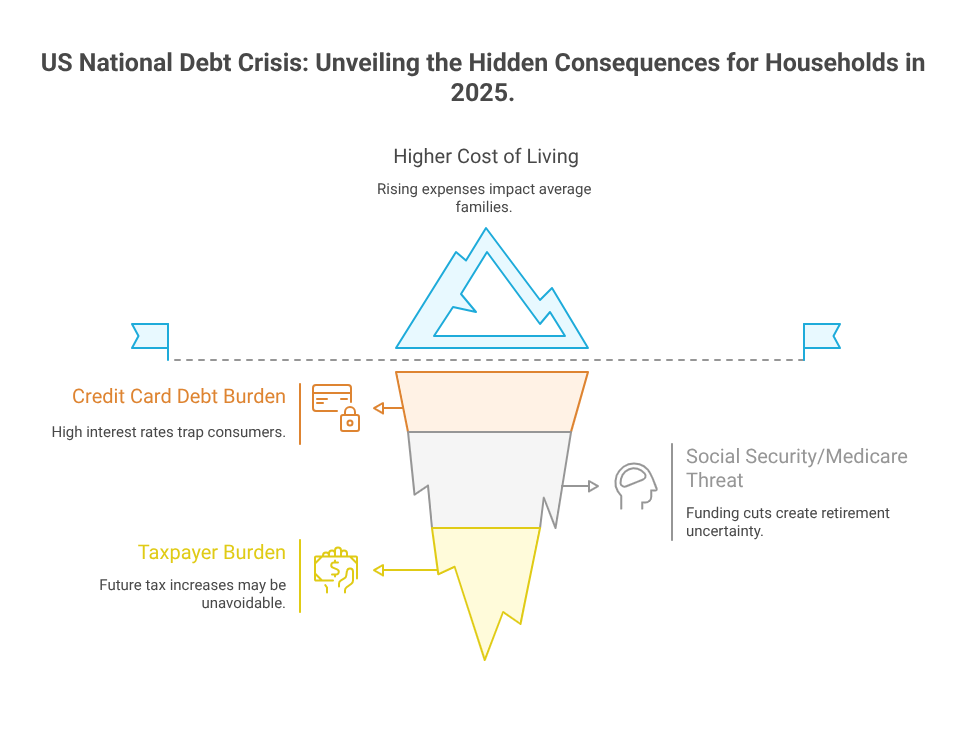

1. Higher Cost of Living

The average American family is already grappling with rising living expenses. The national debt contributes to inflationary pressure, meaning wages often fail to keep pace with price increases. Essentials like groceries, gas, and housing have all seen sustained cost hikes.

2. Credit Card and Loan Debt Burden

Credit card interest rates in 2025 hover near record highs, often above 20% APR, partly due to the Federal Reserve’s policy response to debt-driven inflation. Mortgage rates remain elevated, making homeownership less affordable. The debt trap for consumers mirrors the national debt spiral.

3. Threat to Social Security and Medicare

Programs like Social Security and Medicare rely on federal funding. As the US government spends more on interest payments to service its $35 trillion debt, funding for these programs could face cuts or restructuring. For retirees and those nearing retirement, this creates uncertainty.

4. Taxpayer Burden

Every American citizen’s “share” of the $35 trillion debt is over $100,000 per taxpayer. While you don’t get a personal bill, the reality is that future tax increases may be unavoidable.

Inflation in 2025: The Debt Connection

One of the clearest links between the US national debt and your wallet is inflation. As the government borrows more, the money supply increases, and the dollar weakens. Even with the Federal Reserve attempting to stabilize inflation, deficit-driven demand continues to push prices higher.

In 2025, inflation has stabilized compared to 2022–2023 but remains above the Federal Reserve’s 2% target. Persistent deficits make it difficult to fully tame inflation, leaving households stuck with higher prices on everyday goods.

Interest Rates: Why Debt Matters

The Federal Reserve’s approach to debt-driven inflation has been to raise interest rates, but this strategy comes with trade-offs. While higher rates slow borrowing and cool inflation, they also:

- Make mortgages more expensive, keeping first-time buyers locked out of the housing market.

- Push credit card balances higher due to compounding interest.

- Increase student loan repayment burdens.

In short, the $35 trillion debt level directly influences the cost of borrowing for families and businesses.

The Future of Taxes and Spending Cuts

When debt grows to this size, the government faces limited options:

- Raise Taxes – Income taxes, capital gains, and corporate taxes could rise to help balance budgets.

- Cut Spending – Social programs, healthcare, education, and defense may face reductions.

- Print More Money – Which risks fuelling further inflation?

None of these solutions is painless. For the average American, it likely means higher taxes, fewer benefits, or both in the coming years.

Household Debt vs. National Debt

The parallels between the national debt and household debt are striking. Just as the government borrows beyond its means, many American households are also weighed down by record credit card debt, auto loans, and mortgages.

- Household debt in 2025 has surpassed $17 trillion, with delinquencies rising.

- Credit card balances are at record highs, reflecting the struggle to keep up with inflation.

- Student loan repayments resuming after the pandemic pause adds further strain.

This double-debt pressure—national and personal—creates a vicious cycle where higher government debt worsens inflation, which in turn pushes households deeper into their own debt.

Why You Should Care About the Debt Clock

The US Debt Clock hitting $35 trillion isn’t just a statistic—it’s a warning sign. If you’re working, saving, or planning for retirement, the trajectory of national debt affects your financial future.

- Investors face volatile markets as debt-driven policies shift interest rates.

- Savers see their money eroded by inflation.

- Families face higher borrowing costs, reducing disposable income.

- Retirees worry about the security of Social Security and Medicare.

Ignoring the debt crisis is no longer an option.

What You Can Do as Debt Surges

While individuals can’t control government borrowing, you can take steps to protect yourself against the fallout from the US national debt crisis in 2025:

- Pay Down High-Interest Debt – With credit card APRs above 20%, prioritize paying off balances.

- Diversify Investments – Inflation erodes savings; consider inflation-protected securities or tangible assets.

- Build an Emergency Fund – Rising costs and economic uncertainty make savings crucial.

- Plan for Higher Taxes – Anticipate that your future tax burden may grow.

- Stay Informed – Following the US Debt Clock helps you understand how macroeconomic shifts affect personal finance.

Looking Ahead: Can the Debt Crisis Be Fixed?

Economists debate whether the US can sustain this level of debt. Some argue that as long as the US dollar remains the global reserve currency, demand for Treasuries will remain strong. Others warn that unchecked borrowing risks a fiscal crisis, where interest payments outpace revenue.

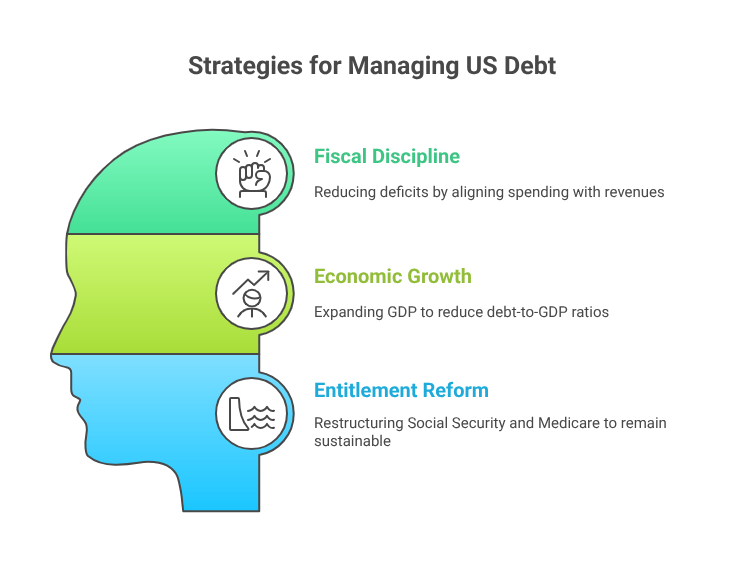

Potential solutions include:

- Fiscal discipline: Reducing deficits by aligning spending with revenues.

- Economic growth: Expanding GDP to reduce debt-to-GDP ratios.

- Entitlement reform: Restructuring Social Security and Medicare to remain sustainable.

But without political will, the debt is likely to keep climbing, leaving the next generation to face even larger burdens.

What This Means for Your Financial Future

The US Debt Clock hitting $35 trillion in 2025 is more than a headline—it’s a financial reality with far-reaching effects on every American. From inflation to interest rates, from taxes to retirement security, the rising national debt is shaping the economy in ways that directly impact households.

As policymakers grapple with how to manage this unprecedented debt, individuals must take proactive steps to safeguard their finances. Paying off high-interest debt, preparing for higher taxes, and protecting savings against inflation are no longer just good advice—they’re essential survival strategies in a $35 trillion debt economy.

The number on the US Debt Clock may seem distant, but in 2025, it’s closer to your wallet than ever before.