How Debt Relief Works: Debt Relief vs Bankruptcy Explained

Debt can quickly become overwhelming. What starts as a few credit card balances can grow into a financial burden that affects your daily life, your relationships, and your peace of mind. Between rising interest rates, increasing living costs, and unexpected expenses, many consumers find themselves struggling to keep up with monthly payments.

When debt becomes unmanageable, two options often appear during online searches: debt relief and bankruptcy.

At first glance, both seem to offer a path out of debt. However, they work very differently and can have significantly different long-term effects on your finances.

If you’re researching debt relief vs bankruptcy, you’re likely looking for answers to important questions:

- Can I avoid bankruptcy?

- Will debt relief reduce what I owe?

- Which option will have less impact on my future?

- Is CuraDebt a legitimate alternative to bankruptcy?

This guide explains how debt relief works, how CuraDebt’s debt relief programs operate, and how debt relief compares to bankruptcy so you can make a more informed financial decision.

👉 See If You Qualify for Debt Relief Today

Why More Americans Are Looking for Bankruptcy Alternatives in 2026

Consumer debt continues to reach record levels. Credit card balances, medical expenses, personal loans, and collection accounts are placing increasing pressure on households across the country.

Many people don’t fall into debt because of poor financial decisions. Common causes include:

- Medical emergencies

- Job loss

- Reduced income

- Divorce

- Unexpected family expenses

- Rising interest rates

When debt payments become difficult to manage, consumers often begin looking for alternatives before considering bankruptcy.

Debt relief programs have become a popular option because they may provide a structured path toward resolving debt without entering a court-supervised bankruptcy process.

What Is Debt Relief?

Debt relief is a broad term used to describe programs that help consumers manage, reduce, or resolve unsecured debt.

Unlike bankruptcy, debt relief generally focuses on negotiating with creditors and creating a manageable strategy for addressing outstanding balances.

Debt relief may be used for:

- Credit card debt

- Medical debt

- Personal loans

- Collection accounts

- Certain business-related debts

The objective is simple: help consumers regain control of their finances and work toward becoming debt-free.

Many debt relief companies provide consultations to determine whether consumers qualify for their programs and whether debt settlement may be appropriate based on their circumstances.

How Does CuraDebt Debt Relief Work?

CuraDebt offers debt relief solutions for consumers facing significant unsecured debt.

The process typically begins with a free consultation designed to evaluate your financial situation.

Step 1: Financial Review

A specialist reviews:

- Total debt balances

- Monthly income

- Monthly expenses

- Types of debt

- Financial hardship factors

This helps determine whether debt relief is a suitable option.

Step 2: Personalized Strategy

Every financial situation is different.

Based on your debt profile, a customized debt resolution strategy is developed to address your unique circumstances.

Step 3: Debt Negotiation

One of the key components of debt relief involves negotiating with creditors.

The goal is to seek favorable settlement opportunities and create a path toward resolving eligible debts.

Step 4: Debt Resolution

Once agreements are reached, consumers follow the established plan until debts are resolved.

For many people, this process provides an alternative to filing bankruptcy while working toward long-term financial recovery.

What Types of Debt Can Debt Relief Help With?

Debt relief programs generally focus on unsecured debts.

Credit Card Debt

Credit cards often carry some of the highest interest rates, making balances difficult to repay.

Medical Debt

Unexpected healthcare expenses remain one of the most common causes of financial hardship.

Personal Loans

Certain unsecured personal loans may qualify for debt relief assistance.

Collection Accounts

Older collection accounts may also be reviewed as part of a debt relief strategy.

Understanding which debts qualify is an important part of determining whether debt relief is the right solution.

What Is Bankruptcy?

Bankruptcy is a legal process designed to help individuals and businesses who can no longer meet their debt obligations.

Unlike debt relief, bankruptcy operates through the federal court system.

The two most common forms of personal bankruptcy are Chapter 7 and Chapter 13.

Chapter 7 Bankruptcy

Chapter 7 is often referred to as liquidation bankruptcy.

Qualifying consumers may have certain unsecured debts discharged through a court-supervised process.

Eligibility requirements apply, and not all debts can be eliminated.

Chapter 13 Bankruptcy

Chapter 13 focuses on restructuring debt through a repayment plan.

Consumers typically make monthly payments over a period of three to five years under court supervision.

Bankruptcy can provide significant relief, but it also carries long-term financial consequences that should be carefully considered.

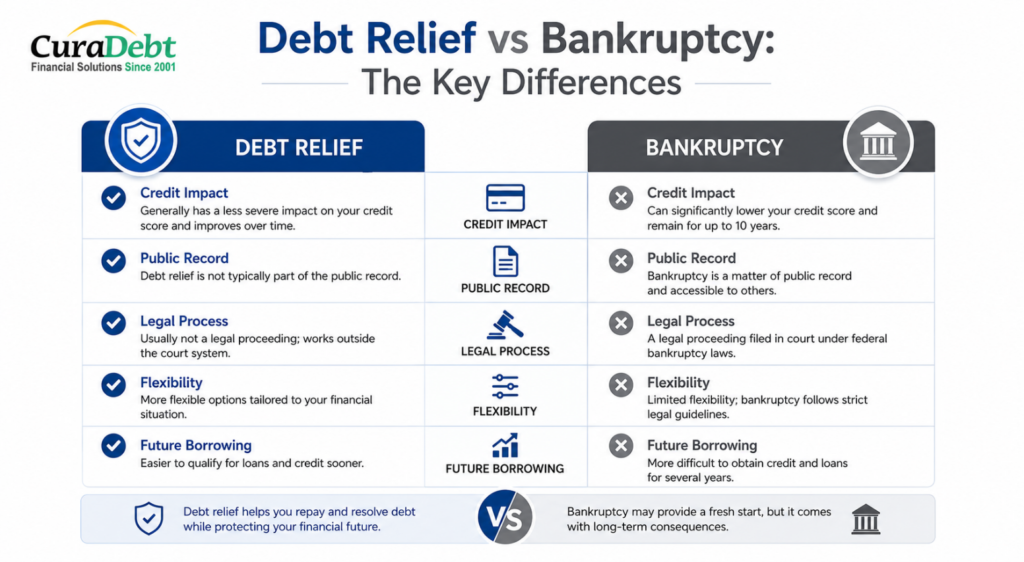

Debt Relief vs Bankruptcy: The Key Differences

Although both solutions are designed to address debt problems, there are important differences.

Credit Score Impact

Both debt relief and bankruptcy may affect your credit profile.

However, bankruptcy generally remains on credit reports longer and is often viewed as a more significant financial event.

Public Record

Bankruptcy filings become public records.

Debt relief programs generally do not involve public court filings.

Court Involvement

Debt relief operates outside the court system.

Bankruptcy requires legal proceedings and court oversight.

Cost

Bankruptcy may involve attorney fees, court filing fees, and administrative expenses.

Debt relief programs have their own costs but may avoid many legal expenses.

Future Financial Opportunities

Many consumers prefer exploring debt relief before bankruptcy because they hope to preserve greater financial flexibility in the future.

Why Many Consumers Explore Debt Relief Before Bankruptcy

For many people, bankruptcy represents a last resort.

Debt relief may provide an opportunity to:

- Address debt without court proceedings

- Seek negotiated settlements

- Explore alternatives before legal action

- Create a structured financial recovery plan

This is one reason debt settlement and debt relief services continue to attract significant attention from consumers facing financial hardship.

👉 Get Your Free CuraDebt Consultation

Pros and Cons of Debt Relief

Advantages

- Alternative to bankruptcy

- Professional negotiation assistance

- Structured debt resolution process

- Potential debt reduction opportunities

- Greater privacy

Disadvantages

- Not all debts qualify

- Results vary by individual circumstances

- Requires commitment and consistency

- May affect credit during the process

Pros and Cons of Bankruptcy

Advantages

- Legal protection from creditors

- Potential discharge of qualifying debts

- Court-supervised structure

Disadvantages

- Public record filing

- Long-term credit impact

- Potential asset implications

- Reduced future borrowing flexibility

Is Debt Relief Right for You?

Debt relief may be worth considering if:

- You have significant unsecured debt

- You still have a source of income

- You want to avoid bankruptcy if possible

- You are willing to follow a structured plan

Consumers in these situations often explore debt relief before considering more drastic legal options.

When Bankruptcy May Be Necessary

Bankruptcy may be appropriate when:

- Debt levels are overwhelming

- Income is insufficient to support repayment

- Creditors are pursuing aggressive actions

- Other debt solutions have failed

Every financial situation is unique, which is why professional guidance can be valuable.

Final Verdict: Debt Relief vs Bankruptcy

There is no universal solution for debt problems.

Debt relief and bankruptcy both exist because different financial situations require different approaches.

For many consumers, debt relief provides an opportunity to address debt, negotiate with creditors, and work toward financial recovery without entering a formal bankruptcy process.

For others facing severe financial hardship, bankruptcy may ultimately provide the protection and relief they need.

The most important step is understanding your options before making a decision.

If you’re struggling with credit card debt, personal loans, medical bills, or collection accounts, exploring debt relief may be worth considering before filing bankruptcy.

Start Your Free Debt Relief Consultation Today

Don’t wait until financial stress becomes overwhelming.