Debt Collectors Calling for Someone Else? Your Legal Rights Explained (US, Canada, UK)

If you’re receiving repeated calls from debt collectors about a debt that isn’t yours, you’re not alone. Searches for “debt collectors calling me for someone else” and “wrong number debt calls” have surged across the US, Canada, and the UK—driven by aggressive skip-tracing, recycled phone numbers, and outdated creditor databases.

What many people don’t realize is this: you have legal rights, even if you’re not the debtor. Debt collectors are not allowed to harass, intimidate, or repeatedly contact you once they know they have the wrong person. Yet thousands of consumers continue to receive daily calls, voicemails, and even threats for debts that have nothing to do with them.

This article explains why this happens, what the law says, and how to stop wrong-number debt collection calls in the United States, Canada, and the United Kingdom.

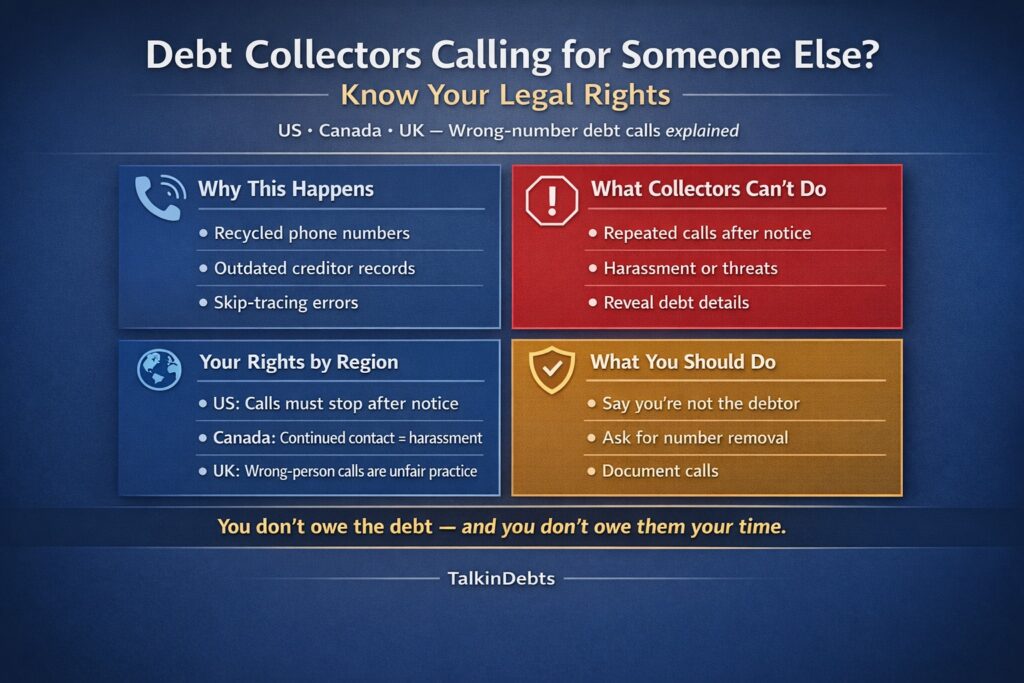

Why Debt Collectors Call the Wrong Person

Debt collectors rely heavily on data—often old, incomplete, or inaccurate. When someone changes their phone number, relocates, or shares a family name with a debtor, collection systems may link the wrong contact details to an account.

Common reasons include:

- Phone numbers reassigned by telecom providers

- Outdated creditor records

- Incorrect skip-tracing results

- Family members, roommates, or previous number owners

- Clerical or data-entry errors

While mistakes happen, repeated contact after you’ve stated you’re not the debtor is not acceptable in most jurisdictions.

Are Debt Collectors Allowed to Call You for Someone Else?

Short answer: Only in very limited circumstances—and not repeatedly.

Collectors may initially contact third parties solely to locate the debtor, but once they are informed they’ve reached the wrong person, continued calls can cross into harassment or unlawful conduct.

Let’s break this down country by country.

United States: Your Rights Against Wrong-Number Debt Calls

In the US, debt collection is regulated at both the federal and state levels. If debt collectors are calling you for someone else, the law provides clear protections.

What Collectors Are Allowed to Do

- Contact a third party once to confirm location details

- Ask if you know the debtor (without discussing the debt)

- Identify themselves without revealing sensitive information

What Collectors Are NOT Allowed to Do

- Continue calling after you state you are not the debtor

- Reveal details about the debt

- Harass, threaten, or intimidate you

- Use robocalls or repeated calls to pressure you

If wrong-number debt calls continue, the behavior may violate federal consumer protection laws, especially if the calls are frequent or abusive.

What You Should Do Immediately

- Clearly state that you are not the debtor

- Ask the caller to remove your number from their records

- Document dates, times, and call details

- Follow up in writing if calls continue

Persistent calls may entitle you to statutory damages, even if you don’t owe any money.

Canada: Protection From Debt Collectors Calling the Wrong Person

In Canada, debt collection practices are regulated provincially but follow similar consumer-protection principles nationwide.

Key Consumer Rights in Canada

- Collectors must stop contacting you once informed that they have the wrong person

- Calls cannot be excessive or misleading

- You cannot be pressured to provide personal information

- Debt details cannot be disclosed to third parties

If debt collectors continue calling you for someone else after notice, the behavior may be considered harassment under provincial regulations.

Best Steps to Stop Wrong Number Debt Calls in Canada

- State clearly that the debtor does not reside at your number

- Refuse to confirm personal data unrelated to you

- Request written confirmation that your number has been removed

- File a complaint with the relevant provincial authority if calls persist

Canadian regulators take repeated third-party contact seriously, especially when it causes distress or disruption.

United Kingdom: Wrong Person Debt Collection Calls Explained

In the UK, debt collection agencies are governed by strict conduct standards designed to prevent unfair treatment of consumers and third parties.

What UK Law Says

- Debt collectors must ensure data accuracy

- Contacting the wrong person repeatedly is considered an unfair practice

- Harassment includes frequent calls, pressure, or misleading claims

- You are not required to prove you are not the debtor

Once you inform a collector that they’ve contacted the wrong individual, they are expected to stop and correct their records.

If Calls Continue in the UK

You can:

- Request all communication stop immediately

- Ask for written confirmation of record correction

- Escalate the matter to the agency’s compliance department

- File a complaint with the financial regulator or ombudsman

Wrong number debt calls that continue may indicate poor data governance or regulatory non-compliance.

Can Debt Collectors Leave Voicemails for Someone Else?

This is a major concern for many consumers.

In most cases:

- Voicemails cannot disclose debt details

- Messages must be limited and non-specific

- Repeated voicemails after being told they have the wrong person may be unlawful

If collectors leave messages referencing a debt that isn’t yours, it could amount to a privacy violation—especially if others can hear or access those messages.

What If the Calls Are Automated or Robocalls?

Automated debt collection calls raise additional legal issues.

Across the US, Canada, and the UK:

- Robocalls to wrong numbers are heavily restricted

- Consent requirements are strict

- Repeated automated calls can trigger higher penalties

If you’re receiving frequent automated calls for someone else, document everything. These cases often carry stronger enforcement options.

How to Stop Debt Collectors Calling You for Someone Else

Here’s a practical, step-by-step approach that works across jurisdictions:

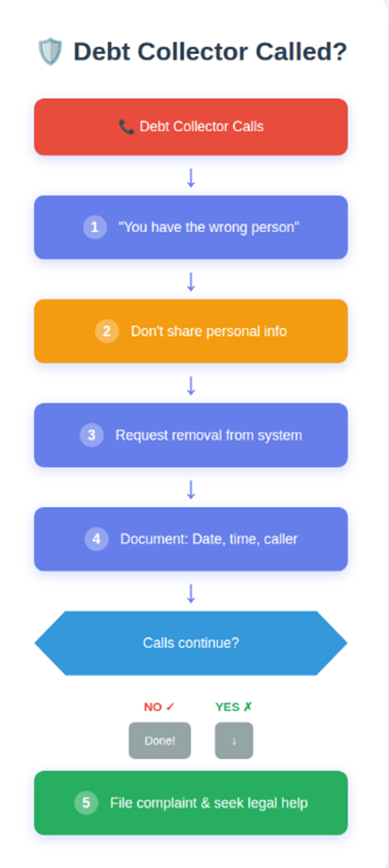

Step 1: Be Direct and Calm

State clearly:

“You have the wrong number. I am not the person you are trying to reach.”

Step 2: Do Not Provide Personal Details

You are not obligated to share your address, date of birth, or ID.

Step 3: Request Removal

Ask them to remove your number from their system immediately.

Step 4: Keep Records

Log call times, numbers, voicemails, and agent names.

Step 5: Escalate If Needed

If calls continue:

- File regulatory complaints

- Seek legal advice

- Consider consumer protection agencies

In many cases, just one formal complaint is enough to stop the calls permanently.

Why This Issue Is Increasing in 2025

Several trends are driving the spike in wrong-number debt calls:

- Increased use of AI-driven skip tracing

- Mass debt portfolio sales

- Telecom number recycling

- Cross-border outsourcing

- Data accuracy lagging behind speed

As lenders and collectors race to recover debts, third-party consumers often get caught in the middle.

You Are Not Responsible for Someone Else’s Debt

This cannot be said enough:

You are not legally responsible for a debt simply because a collector has your phone number.

Debt collectors calling you for someone else does not create any obligation on your part. The law in the US, Canada, and the UK is designed to protect non-debtors from harassment, privacy breaches, and unfair treatment.

If wrong-number debt calls are disrupting your life, you have every right to demand they stop—and to take action if they don’t.

To Stop Debt Collector Harassment, Check out our Free Debt Collection Cease and Desist Letter Generator Tool